TWAP: Time-Weighted Average Price for Institutional Execution

⚡ Key Takeaways

- TWAP (Time-Weighted Average Price) calculates the average price of a security over a specific time period, weighting each price equally regardless of volume.

- Institutional traders use TWAP algorithms to execute large orders by slicing them into equal-sized pieces distributed evenly across a time window, minimizing market impact.

- TWAP differs from VWAP in that it ignores volume entirely — making it preferable for illiquid stocks or when the goal is consistent execution pacing.

- Retail traders can use TWAP as a benchmark to evaluate whether their fills were favorable relative to the session's average price.

What Is TWAP?

TWAP (Time-Weighted Average Price) is the arithmetic mean of a security's price sampled at regular intervals over a defined period. If you snapshot a stock's price every minute for an hour and average those 60 readings, you have the TWAP for that hour.

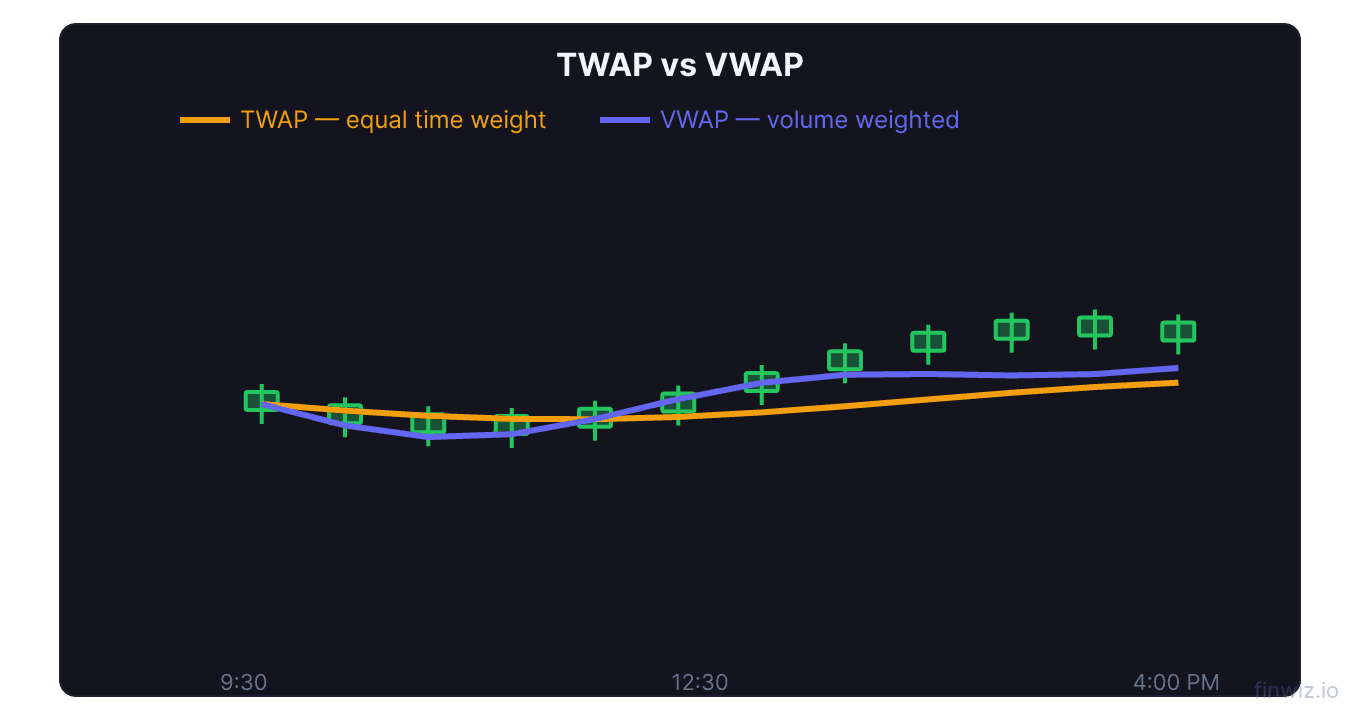

Unlike VWAP, which weights each price by the volume traded at that price, TWAP treats every time interval equally. A price printed at 10:15 AM when 500 shares traded carries the same weight as a price at 2:30 PM when 50,000 shares traded. This simplicity is both TWAP's strength and its limitation.

TWAP originated on institutional trading desks as a straightforward execution benchmark. Before algorithmic trading, a desk trader might manually break a 100,000-share order into equal chunks and execute one chunk every 10 minutes. That manual process was the original TWAP strategy. Today, algorithms handle this automatically with far greater precision.

TWAP = (P₁ + P₂ + P₃ + ... + Pₙ) / nHow TWAP Algorithms Work

A TWAP algorithm divides a parent order into equal child orders and distributes them evenly across a specified execution window. If a fund needs to buy 60,000 shares of JPM over 6 hours, the algorithm executes roughly 10,000 shares per hour — or about 167 shares per minute — regardless of what volume or price is doing.

The algorithm uses time slicing rather than volume slicing. Each slice targets a fixed time interval. Within each interval, the algorithm may use limit orders to avoid crossing the spread or market orders if the slice must complete before the interval ends.

Sophisticated TWAP algorithms add randomization to prevent detection. A pure TWAP that executes exactly 167 shares every 60 seconds becomes predictable — other algorithms and traders in dark pools can detect the pattern and front-run the remaining orders. Modern TWAP engines randomize both the timing and size of child orders around the target average while maintaining the overall time-weighted distribution.

Institutional Use Cases

Illiquid stocks. When executing in names with thin order books, TWAP is preferred over VWAP because volume-weighted algorithms may cluster executions during brief volume spikes, creating adverse slippage. TWAP spreads the order evenly regardless of volume patterns, reducing the chance of exhausting available liquidity at any single moment.

Overnight or multi-day execution. For very large positions that must be built over days, TWAP provides a predictable pacing framework. A pension fund accumulating a position in MSFT might run a TWAP algorithm across five trading days, executing equal portions each day.

Currency and commodity markets. In 24-hour markets like forex and futures, TWAP is common because volume data can be fragmented across exchanges. The time-based approach sidesteps the need for consolidated volume feeds.

Benchmark for order fills. Portfolio managers evaluate their execution desk by comparing actual fill prices against the TWAP of their execution window. If the desk bought shares at an average of $152.30 and the TWAP was $152.50, the desk achieved positive execution quality — $0.20 per share of price improvement.

TWAP vs. VWAP

The core difference is weighting. VWAP weights prices by volume, so prices during high-volume periods dominate the average. TWAP weights all time intervals equally, ignoring volume entirely.

| Feature | TWAP | VWAP |

|---|---|---|

| Weighting | Equal time intervals | Volume at each price |

| Best for | Illiquid stocks, consistent pacing | Liquid stocks, minimizing market impact |

| Volume sensitivity | None | High |

| Predictability | Higher (can be front-run) | Lower (adapts to volume) |

| Calculation complexity | Simple | Moderate |

In liquid large-cap stocks like AAPL or AMZN, VWAP is almost always preferred because volume clustering reflects genuine institutional participation patterns. In thinly traded small-caps, TWAP avoids the problem of VWAP forcing excessive execution during sporadic volume bursts.

Pro Tip

Using TWAP as a Retail Trader

While TWAP algorithms are institutional tools, retail traders can apply the TWAP concept in two practical ways.

Manual TWAP entries. If you want to build a position in a volatile stock without timing risk, divide your total intended position into equal parts and buy at fixed time intervals. Buying 100 shares of GOOGL? Purchase 25 shares at 10:00 AM, 25 at 11:00 AM, 25 at 1:00 PM, and 25 at 3:00 PM. This simple approach prevents the common mistake of committing your entire position at a single potentially unfavorable price.

TWAP as a trend filter. Plot the session TWAP on an intraday chart. When price is above TWAP, buyers have controlled the session on average. When below, sellers have dominated. This works similarly to VWAP as a dynamic support/resistance level, though it is less widely watched and therefore less likely to produce self-fulfilling reactions.

Limitations of TWAP

TWAP's equal time weighting is a double-edged sword. During low-volume lunch hours, prices may drift on thin activity, and TWAP gives those drifts the same weight as prices established during high-conviction opening or closing action. This can make TWAP misleading as a fair value reference during sessions with uneven activity.

TWAP algorithms are also easier to detect than VWAP algorithms because their execution pattern is more mechanical. Predatory algorithms specifically scan for TWAP signatures — steady, evenly spaced order flow — and attempt to trade ahead of the remaining slices.

Finally, TWAP does not adapt to market conditions. If a stock gaps sharply against your TWAP execution midway through the window, the algorithm continues executing at the same pace rather than pausing or accelerating. More sophisticated algorithms like implementation shortfall strategies adjust dynamically, but pure TWAP does not.

Frequently Asked Questions

When should I use TWAP instead of VWAP?

Use TWAP when trading illiquid securities where volume is sparse or unpredictable, or when your goal is simply to spread execution evenly across time. TWAP is also preferred when reliable real-time volume data is unavailable. For most liquid U.S. equities, VWAP is the better benchmark and execution algorithm.

Can retail brokers execute TWAP orders?

Most standard retail brokers do not offer native TWAP algorithms. Some advanced platforms like Interactive Brokers provide TWAP as an order type. Retail traders can approximate TWAP manually by setting price alerts at fixed time intervals and executing equal-sized orders at each alert. Algorithmic trading platforms aimed at active traders increasingly offer TWAP functionality.

Does TWAP work for cryptocurrency trading?

Yes, and it is widely used. Crypto markets trade 24/7 with highly variable volume patterns across time zones. TWAP algorithms help large crypto buyers and sellers execute without causing dramatic price dislocations in thinner overnight sessions. Major crypto exchanges and OTC desks offer TWAP execution natively.

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.