Slippage: Why Your Fill Price Differs from Your Expected Price

⚡ Key Takeaways

- Slippage is the difference between the price you expect to pay for a trade and the price you actually receive — it can work for or against you, but negative slippage is far more common

- Market orders are the primary cause of slippage because they execute at whatever price is available, not a price you specify

- Limit orders eliminate slippage entirely by setting a maximum buy price or minimum sell price, though the trade may not execute at all if the market moves away

- High-volatility events like earnings releases, FOMC announcements, and market opens produce the worst slippage because prices move faster than orders can fill

- Slippage compounds over hundreds of trades — a consistent $0.05/share slippage on 500 shares across 4 daily trades costs a day trader over $25,000 per year

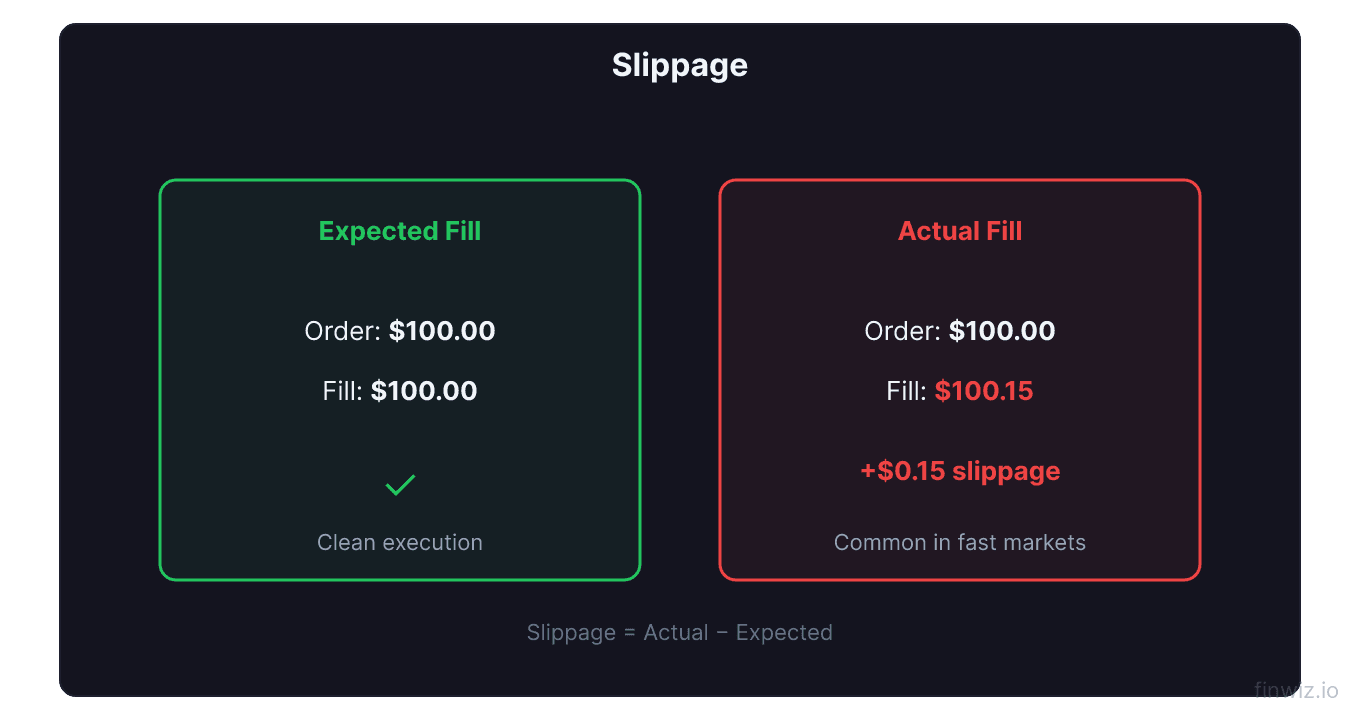

What Is Slippage?

Slippage occurs when your trade executes at a different price than the one displayed on your screen when you clicked the button. You see AAPL at $192.50, submit a buy order, and get filled at $192.54. That $0.04 difference is slippage. It sounds trivial on a single trade, but it is one of the most significant hidden costs in active trading.

Slippage happens because markets are not static. Between the moment you decide to trade and the moment your order reaches the exchange and gets matched with a counterparty, the price can move. The faster the market is moving and the less liquid the stock, the more slippage you experience.

There are two types of slippage. Negative slippage means you got a worse price than expected — you paid more when buying or received less when selling. Positive slippage means you got a better price. Positive slippage does happen, but the structure of modern markets makes negative slippage more common, particularly for retail traders using market orders.

Slippage = Execution Price - Expected PriceMarket Orders vs. Limit Orders: The Core Trade-Off

The single biggest factor in slippage is your order type. A market order tells your broker "buy or sell this stock right now at whatever price is available." You get speed and certainty of execution, but zero control over price. A limit order says "buy or sell only at this price or better." You get price control but risk the order never filling.

When you submit a market order to buy 1,000 shares of a stock with only 300 shares offered at the best ask price, your order eats through multiple price levels. The first 300 shares fill at $50.00, the next 400 at $50.02, and the last 300 at $50.05. Your average fill is $50.02 — two cents of slippage caused entirely by the order type.

This is directly related to the bid-ask spread. Stocks with wide spreads (low-liquidity names, penny stocks, pre-market sessions) produce more slippage because there is more distance between where buyers and sellers are willing to transact. A stock with a $0.01 spread like SPY produces far less slippage than a low-float small-cap with a $0.10 spread.

Pro Tip

When Slippage Gets Extreme: High-Volatility Scenarios

Certain market conditions amplify slippage dramatically. Understanding these scenarios helps you avoid the worst fills of your trading career.

Earnings releases are among the worst. When a company reports after hours, the stock can gap 5-15% overnight. If you had a market order queued for the open, you get filled at the new price — potentially dollars away from the previous close. NVDA reporting a blowout quarter and gapping from $700 to $760 means any market buy order at the open fills near $760, not the $700 you saw at yesterday's close.

FOMC announcements and economic data releases cause price to spike in both directions within seconds. The bid-ask spread on even liquid stocks like SPY can widen from $0.01 to $0.05 or more in the moments surrounding the announcement. Algorithmic traders pull their orders from the book, leaving fewer resting orders to absorb your trade.

Market open (9:30 AM ET) is consistently the highest-slippage period of the trading day. Overnight order flow and pre-market gaps create a flood of orders hitting the exchange simultaneously. The first 5-10 minutes produce the widest spreads and fastest price changes. Many experienced scalping traders wait until 9:45 or 10:00 AM to let the opening chaos settle before placing trades.

Flash crashes and circuit breakers represent the extreme end. During the May 2010 flash crash, some stocks briefly traded at $0.01 while others hit absurd prices. Market orders during these events fill at catastrophic levels.

How to Reduce Slippage

You cannot eliminate slippage entirely, but you can minimize it with disciplined habits.

Use limit orders for entries. Set your limit at or slightly above the ask for buys (or slightly below the bid for sells). You might miss a few trades, but over hundreds of trades, the saved slippage adds up to thousands of dollars.

Trade liquid stocks. Stick to names with average daily volume above 1 million shares and tight bid-ask spreads. The top components of SPY, QQQ, and other major ETFs — AAPL, MSFT, AMZN, GOOGL, META, NVDA — consistently offer the tightest spreads and deepest order books.

Avoid trading during news events. If you are already in a position when news hits, use pre-set limit orders or stop-limits rather than panic-clicking market orders. If you are looking to enter, wait 2-5 minutes for the spread to tighten and the initial volatility to subside.

Size your orders relative to volume. If a stock trades 50,000 shares per 5-minute candle and you are trying to buy 10,000 shares with a market order, you are trying to absorb 20% of recent volume in an instant. Break large orders into smaller pieces or use time-weighted algorithms.

Rule of Thumb for Order Sizing:Choose brokers with smart order routing. Not all brokers route orders the same way. Some prioritize speed, others prioritize price improvement. Brokers that route to exchanges and ECNs offering price improvement (rather than selling order flow to market makers) tend to produce less slippage on average.

Pro Tip

Frequently Asked Questions

Does slippage affect limit orders?

No. A limit order guarantees your price or better. The trade-off is that your order may not fill at all if the market moves away from your limit price. This is called opportunity cost — the cost of missing a profitable trade because your limit was too tight. Many traders accept small slippage on market orders rather than risk missing a fast-moving setup entirely.

Is slippage worse for buying or selling?

Slippage affects both sides, but selling during a rapid decline typically produces worse slippage than buying during a rally. This is because sell-offs tend to be faster and more violent than rallies (fear moves markets faster than greed), and liquidity dries up more quickly on the downside as market makers widen their quotes.

How does slippage differ in crypto and forex compared to stocks?

Slippage in crypto is generally worse than in stocks because crypto markets are more fragmented, less regulated, and have thinner order books outside of the top few coins. Forex slippage on major pairs (EUR/USD, GBP/USD) is typically very low due to the massive daily volume (over $6 trillion), but can spike during news events and low-liquidity sessions like the Asian close.

Related Articles

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.