Bear Put Spread: Profiting from Downside with Defined Risk

⚡ Key Takeaways

- A bear put spread involves buying a put at a higher strike and selling a put at a lower strike with the same expiration

- Maximum profit equals the difference between strikes minus the net debit paid

- Maximum loss is limited to the net debit, providing defined risk for bearish trades

- Bear put spreads cost less than buying puts outright, making them more capital-efficient

- The strategy works best with a moderately bearish outlook and when implied volatility is elevated

What Is a Bear Put Spread?

A bear put spread (also called a long put vertical or put debit spread) is a two-leg options strategy that profits when the underlying stock declines moderately. You buy a put at a higher strike price and simultaneously sell a put at a lower strike price, both with the same expiration date.

The sold put reduces your total cost by partially offsetting the premium of the bought put. In exchange, your profit potential is capped at the lower strike price. This creates a defined-risk, defined-reward bearish trade.

Bear put spreads are the bearish counterpart to bull call spreads. They are popular among traders who want to profit from declines without paying the full cost of buying put options outright.

How to Construct a Bear Put Spread

A bear put spread has two legs with the same expiration:

- Buy 1 put at the higher strike (typically ATM or slightly ITM)

- Sell 1 put at the lower strike (further OTM)

Example: Stock XYZ trades at $100. You expect it to fall to around $90 over the next 30 days.

| Leg | Action | Strike | Premium |

|---|---|---|---|

| 1 | Buy put | $100 | -$4.20 |

| 2 | Sell put | $90 | +$1.30 |

| Net | -$2.90 (debit) |

Your total cost is $2.90 per share, or $290 per contract. This is both your investment and your maximum risk.

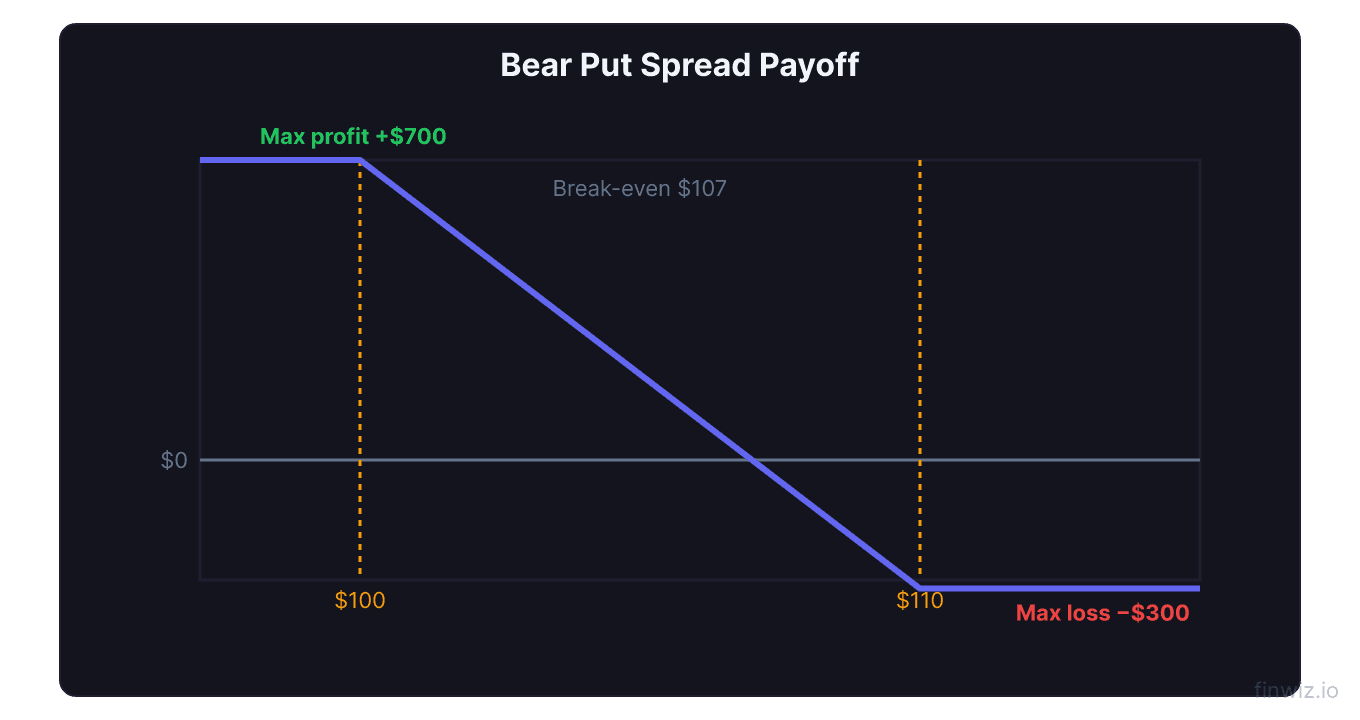

Maximum Profit, Maximum Loss, and Breakeven

Maximum Profit = (Higher Strike − Lower Strike − Net Debit) × 100Using our example:

| Metric | Calculation | Result |

|---|---|---|

| Max Profit | ($100 − $90 − $2.90) × 100 | $710 |

| Max Loss | $2.90 × 100 | $290 |

| Breakeven | $100 − $2.90 | $97.10 |

| Risk-Reward Ratio | $710 ÷ $290 | 2.45:1 |

The stock needs to drop just 2.9% to break even. Maximum profit is achieved when the stock falls to $90 or below at expiration.

Payoff at Expiration

| Stock Price | Long $100 Put Value | Short $90 Put Value | Net P/L |

|---|---|---|---|

| $105 | $0 | $0 | -$290 |

| $100 | $0 | $0 | -$290 |

| $97.10 | $2.90 | $0 | $0 (breakeven) |

| $95 | $5.00 | $0 | +$210 |

| $92 | $8.00 | $0 | +$510 |

| $90 | $10.00 | $0 | +$710 (max profit) |

| $85 | $15.00 | -$5.00 | +$710 (max profit) |

| $80 | $20.00 | -$10.00 | +$710 (max profit) |

Once the stock falls below $90, additional gains on the long put are offset by losses on the short put. Your profit is capped at $710 regardless of how far the stock falls.

Pro Tip

When to Use a Bear Put Spread

Moderately bearish outlook. You expect a decline but not a catastrophic crash. The stock needs to reach your lower strike for maximum profit.

Elevated implied volatility. When IV is high, puts are expensive. The bear put spread reduces your net cost because the sold put offsets some of the inflated premium. You also gain partial protection from IV crush.

Defined risk needed. Unlike short selling, your maximum loss is known before you enter the trade. This simplifies risk management and position sizing.

Better than buying puts when: IV is above average, you want a lower breakeven, or you are targeting a specific downside price level rather than an open-ended decline.

Bear Put Spread vs. Buying Puts

| Factor | Bear Put Spread | Long Put |

|---|---|---|

| Cost | Lower (net debit) | Higher (full premium) |

| Max profit | Capped | Large (stock to $0) |

| Max loss | Net debit | Full premium |

| Breakeven | Closer to current price | Further from current price |

| Theta impact | Partially offset | Full negative theta |

| Vega exposure | Reduced | Full positive vega |

| Best for | Moderate declines | Large declines |

Example comparison on a $100 stock:

- Bear put spread ($100/$90): Cost $2.90, max profit $710, breakeven $97.10

- Long $100 put: Cost $4.20, max profit $9,580 (to $0), breakeven $95.80

For a moderate decline to $90:

- Spread profit: $710 (245% return on $290 cost)

- Long put profit: $580 (138% return on $420 cost)

The spread generates a higher percentage return for the same moderate move because it costs less to enter.

Choosing Strike Prices

Upper strike (long put): Buy the ATM or slightly ITM put for maximum delta and the best chance of the spread gaining value quickly. Buying an OTM put reduces cost but increases the distance to breakeven.

Lower strike (short put): This is your profit target. Place it at the level where you expect the stock to settle or at a strong support level.

| Spread Width | Net Debit | Max Profit | Risk-Reward |

|---|---|---|---|

| $5 ($100/$95) | $1.80 | $320 | 1.78:1 |

| $10 ($100/$90) | $2.90 | $710 | 2.45:1 |

| $15 ($100/$85) | $3.50 | $1,150 | 3.29:1 |

| $20 ($100/$80) | $3.80 | $1,620 | 4.26:1 |

Wider spreads offer better risk-reward ratios but require a larger stock move to reach maximum profit. Match the width to your price target and conviction level.

Expiration Selection

Short-term (7-14 DTE): Use for immediate catalysts like earnings. Fast gamma means the spread gains or loses value quickly.

Medium-term (30-45 DTE): The most popular choice. Enough time for the bearish thesis to develop without excessive time decay eating your long put.

Long-term (60-90+ DTE): Best when the catalyst has an uncertain timeline, such as a deteriorating fundamental picture that will take time to play out in the stock price.

Time decay affects both legs, but the long put (higher strike) decays faster because it has more extrinsic value. As expiration approaches, theta becomes a headwind if the stock has not moved enough.

Managing the Position

Take profits at 50-75% of max profit. If your spread has captured most of the available profit, close it rather than holding to expiration and risking a reversal.

Cut losses at 50%. If the spread has lost half its value, the trade is not working. Close and preserve the remaining capital.

Roll down and out. If the stock has dropped but not enough, close the current spread and open a new one with lower strikes and a later expiration. This gives the trade more time but resets your cost.

Watch for reversals. If the stock drops to your lower strike and you reach max profit early, close immediately. Holding risks a bounce that erodes profits.

Close before expiration. If both puts are ITM, close the spread to avoid assignment risk on the short put and exercise issues on the long put.

Real-World Example

Stock DEF trades at $75 and you are bearish due to a weakening sector and rising competition.

Trade: Buy $75/$65 bear put spread, 35 DTE

- Buy $75 put: $3.80

- Sell $65 put: $0.90

- Net debit: $2.90 ($290 per contract)

- Max profit: ($75 − $65 − $2.90) × 100 = $710

- Breakeven: $72.10

Outcome 1: Stock drops to $62 on bad earnings. Spread value: $10.00. Profit: ($10 − $2.90) × 100 = $710 (245% return).

Outcome 2: Stock rises to $80. Both puts expire worthless. Loss: $290 (100% of investment).

Outcome 3: Stock drops to $70. Spread value: $5.00. Profit: ($5 − $2.90) × 100 = $210 (72% return).

Even in Outcome 3, where the stock dropped moderately, the spread returned 72%. Compare this to a long put at the $75 strike costing $3.80: at $70, the put is worth $5.00, for a profit of $120 (32% return). The spread wins on percentage return.

Comparison to Bear Call Spread

Both strategies profit from declines but use different mechanics:

| Feature | Bear Put Spread | Bear Call Spread |

|---|---|---|

| Type | Debit spread | Credit spread |

| Entry | Pay net debit | Collect net credit |

| Profit mechanism | Spread widens | Short call expires worthless |

| Risk | Net debit paid | Width − credit |

| Reward | Width − debit | Credit collected |

| Theta impact | Against you | In your favor |

A bear call spread is better when IV is high (you collect more credit) and you prefer theta working in your favor. A bear put spread is better when you want a cleaner risk-reward and are willing to pay upfront.

Frequently Asked Questions

What is the maximum I can lose on a bear put spread?

Your maximum loss is the net debit paid. If the spread costs $2.90 ($290 per contract), that is your worst-case scenario. This occurs when the stock stays at or above the higher strike at expiration, causing both puts to expire worthless.

Can I make money if the stock only drops a little?

Yes. You start profiting once the stock drops below your breakeven (higher strike minus net debit). A small decline that crosses the breakeven generates a partial profit. You do not need the stock to reach the lower strike to make money — you just need it to pass the breakeven.

Should I use a bear put spread or short the stock?

A bear put spread is almost always better for retail traders. It has defined risk (you know your max loss), requires less capital (just the debit), has no borrowing costs, and cannot be short squeezed. Short selling has unlimited risk, margin requirements, and borrowing fees. The only advantage of shorting is no expiration date.

What happens at expiration if the stock is between my strikes?

The long put (higher strike) is ITM and may be auto-exercised, while the short put (lower strike) expires worthless. This means you would sell 100 shares short at the higher strike price. To avoid this situation, close the spread before expiration.

Can I turn a long put into a bear put spread?

Yes. If you already own a put and implied volatility spikes, you can sell a lower-strike put against it to create a bear put spread. This locks in some of the IV gain, reduces your cost basis, and converts the trade from undefined to defined reward. This is a common adjustment technique.

Disclaimer

This is educational content, not financial advice. Trading involves risk, and you should consult a qualified financial advisor before making any investment decisions. Past performance does not guarantee future results.

Related Articles

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.