Long Call vs Short Call: Risk, Reward & When to Use Each

⚡ Key Takeaways

- A long call means you bought a call option — you paid a premium and have the right to buy 100 shares at the strike price before expiration

- A short call means you sold a call option — you collected a premium and have the obligation to sell 100 shares at the strike price if assigned

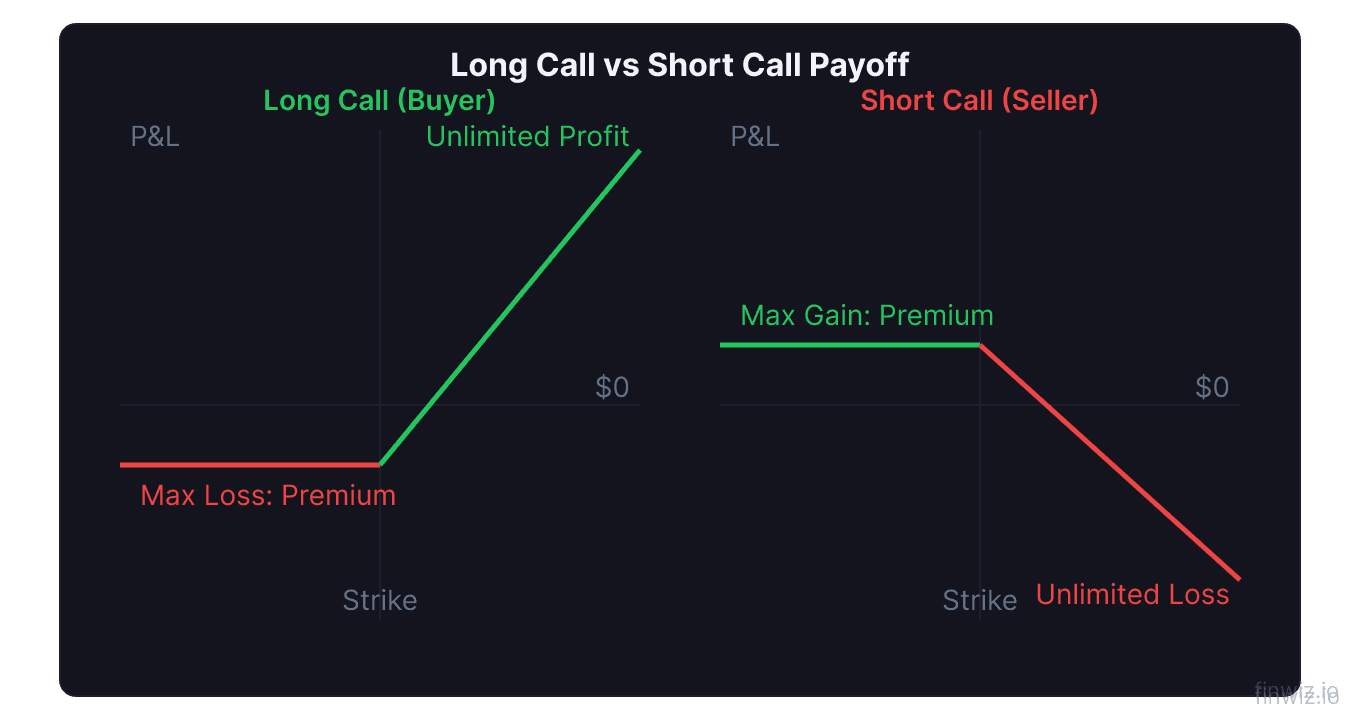

- The long call buyer's maximum loss is the premium paid; the short call seller's maximum loss is theoretically unlimited

- The long call buyer's maximum profit is theoretically unlimited; the short call seller's maximum profit is the premium collected

- Short calls require margin approval and maintenance margin, while long calls only require the premium payment upfront

Long Call vs Short Call: What Is the Difference?

A long call means you bought a call option. You paid a premium and now have the right to purchase 100 shares at the strike price before expiration. A short call means you sold a call option. You collected a premium and now have the obligation to sell 100 shares at the strike price if the buyer exercises. These two positions are exact opposites — the long call buyer's profit is the short call seller's loss, and vice versa.

The critical distinction is the risk-reward profile. Long calls risk a small, known amount (the premium) with the potential for large gains. Short calls earn a small, known amount (the premium) with the potential for large losses. This asymmetry defines when and why traders use each strategy.

Every call option contract has exactly one buyer and one seller. Understanding both sides of the trade is fundamental to every options strategy, from simple directional bets to complex spreads involving multiple options Greeks.

Long Call: How the Buyer's Position Works

When you buy a call (Buy to Open), you are making a bullish bet. You believe the stock will rise above the strike price by enough to cover the premium you paid.

Example: AAPL $200 Call at $8.00 Premium

Suppose AAPL trades at $198. You buy a $200 call expiring in 45 days for $8.00 per share ($800 total for one contract controlling 100 shares).

- Cost: $800 (the premium)

- Breakeven at expiration: $208 ($200 strike + $8 premium)

- Maximum loss: $800 (if AAPL stays at or below $200 at expiration)

- Maximum profit: Theoretically unlimited (AAPL can rise indefinitely)

| AAPL Price at Expiration | Call Intrinsic Value | Buyer P/L |

|---|---|---|

| $185 | $0 | -$800 |

| $195 | $0 | -$800 |

| $200 | $0 | -$800 |

| $208 | $8.00 | $0 (breakeven) |

| $215 | $15.00 | +$700 |

| $230 | $30.00 | +$2,200 |

| $250 | $50.00 | +$4,200 |

The payoff curve is flat at -$800 for all prices at or below $200, then angles upward above the breakeven. Your loss is capped at the premium. Your upside has no ceiling.

Pro Tip

Short Call: How the Seller's Position Works

When you sell a call (Sell to Open), you are making a neutral-to-bearish bet. You believe the stock will stay at or below the strike price, allowing you to keep the premium as profit.

Example: AAPL $200 Call at $8.00 Premium (Seller's Perspective)

Using the same contract, you sell the $200 call and collect $8.00 per share ($800 total).

- Income: $800 (the premium collected)

- Breakeven at expiration: $208 ($200 strike + $8 premium)

- Maximum profit: $800 (if AAPL stays at or below $200 at expiration)

- Maximum loss: Theoretically unlimited (AAPL can rise indefinitely)

| AAPL Price at Expiration | Call Intrinsic Value | Seller P/L |

|---|---|---|

| $185 | $0 | +$800 |

| $195 | $0 | +$800 |

| $200 | $0 | +$800 |

| $208 | $8.00 | $0 (breakeven) |

| $215 | $15.00 | -$700 |

| $230 | $30.00 | -$2,200 |

| $250 | $50.00 | -$4,200 |

The seller's payoff is the mirror image of the buyer's. Every dollar the long call gains above breakeven, the short call loses. The seller wins in three scenarios (stock goes down, stays flat, or rises slightly below breakeven), but loses in one scenario that has no cap.

Side-by-Side Comparison

| Factor | Long Call (Buyer) | Short Call (Seller) |

|---|---|---|

| Market outlook | Bullish | Neutral to bearish |

| Premium | Paid (debit) | Received (credit) |

| Maximum profit | Unlimited | Premium collected |

| Maximum loss | Premium paid | Unlimited (naked) |

| Breakeven | Strike + premium | Strike + premium |

| Margin required | No (pay premium in full) | Yes (naked calls require significant margin) |

| Theta (time decay) | Works against you | Works for you |

| Vega (volatility) | Positive — benefits from IV increase | Negative — benefits from IV decrease |

| Delta | Positive (+0.01 to +1.0) | Negative (-0.01 to -1.0) |

| Probability of profit | Typically 30-45% | Typically 55-70% |

| Assignment risk | None (you exercise by choice) | Yes (can be assigned at any time) |

Margin Requirements and Capital

Long Call Capital Requirement

Buying a call requires no margin. You pay the full premium at the time of purchase and that is your total financial commitment. To buy the AAPL $200 call at $8.00, you need $800 in your account. No additional capital can be demanded.

Short Call Margin Requirement

Selling a naked call requires margin approval (typically Level 4 or 5 at most brokerages) and substantial collateral. The standard margin formula for a naked short call is:

Naked Call Margin = (20% x Underlying Price x 100) + Premium Received - Out-of-the-Money AmountFor the AAPL $200 call sold at $8.00 with AAPL at $198:

- 20% x $198 x 100 = $3,960

- Plus premium: $3,960 + $800 = $4,760

- Minus OTM amount: $4,760 - $200 = $4,560

Your broker holds approximately $4,560 in margin for this single contract. If AAPL rises, the margin requirement increases, and the broker may issue a margin call demanding additional capital.

Selling covered calls eliminates the margin issue because the 100 shares you already own serve as collateral. This makes covered calls the most common short call strategy and a core component of income-oriented portfolios.

The Greeks From Both Sides

Understanding options Greeks from both the buyer's and seller's perspectives clarifies how each position behaves in real time.

Delta measures directional exposure. The long call buyer has positive delta, profiting as AAPL rises. The short call seller has negative delta, profiting as AAPL falls or stays flat. An at-the-money call has roughly 0.50 delta, meaning the buyer gains about $50 per $1 increase in AAPL, and the seller loses $50.

Theta measures time decay. The long call buyer loses value every day as expiration approaches. The short call seller gains that same value. Theta accelerates in the final 30 days before expiration, which is why many call sellers target 30-45 DTE contracts — the decay works in their favor most aggressively during this window.

Vega measures sensitivity to implied volatility. The long call buyer benefits when IV rises because higher volatility increases the option's price. The short call seller benefits when IV falls. This is why selling calls after an IV spike (post-earnings, post-Fed announcement) can be profitable as volatility reverts to its mean.

Managing Risk on Each Side

Long Call Risk Management

- Set a stop-loss on the premium. Many traders exit if the option loses 50% of its value, preserving capital for future trades.

- Roll forward. If the stock has not reached your target but the thesis is intact, roll the call to a later expiration before theta decay accelerates.

- Take partial profits. Sell half the position when the option doubles, letting the remaining contracts ride with zero risk on the original capital.

Short Call Risk Management

- Cover your calls. Owning the underlying stock turns a naked call into a covered call, eliminating the risk of unlimited loss.

- Use a spread. Buying a higher-strike call creates a bear call spread with defined maximum loss. This is how most traders sell calls without taking on naked exposure.

- Set a buy-to-close target. Many sellers close the position when 50-75% of the premium has decayed, rather than holding to expiration and risking a late adverse move.

- Monitor position size. A solid risk management framework limits the total capital exposed to short call positions to a small percentage of the overall portfolio.

Pro Tip

Real-World Walkthrough: AAPL $200 Call

Two traders take opposite sides of the same AAPL $200 call with 45 DTE, priced at $8.00.

Trader A (Long Call): Pays $800. Believes AAPL will rally on strong iPhone demand.

Trader B (Short Call): Collects $800. Believes AAPL will remain range-bound.

Scenario 1: AAPL rises to $225 at expiration.

- Trader A: Call is worth $25.00. Profit: $1,700 (212% return on $800).

- Trader B: Loses $1,700. If naked, margin was approximately $4,500, so the loss exceeds 37% of the margin held.

Scenario 2: AAPL drops to $190 at expiration.

- Trader A: Call expires worthless. Loss: $800 (100% of premium).

- Trader B: Keeps the full $800 premium. Return on margin: approximately 17.5%.

Scenario 3: AAPL closes at $205 at expiration.

- Trader A: Call is worth $5.00. Loss: $300 (AAPL rose but not enough to cover the premium).

- Trader B: Loses $500 in intrinsic value but still nets $300 profit ($800 premium - $500 obligation).

Scenario 3 illustrates why breakeven matters. AAPL rose 3.5% but the call buyer still lost money because the stock did not clear the $208 breakeven. The seller profited despite being wrong about direction because the premium provided a $8 cushion.

Frequently Asked Questions

Which is better for beginners, long calls or short calls?

Long calls are more appropriate for beginners because the maximum loss is defined and known upfront (the premium paid). There is no margin requirement, no risk of assignment, and no possibility of owing more than the initial investment. Short calls, especially naked short calls, carry theoretically unlimited risk and require margin approval that most beginners do not qualify for.

Can I lose more than I invested with a long call?

No. Your maximum loss is the premium paid. If you bought an AAPL $200 call for $800, $800 is the absolute most you can lose. The option can expire completely worthless, but your broker will never demand additional funds on a long call position.

What happens if I get assigned on a short call?

If assigned, you must sell 100 shares at the strike price. If you own the shares (covered call), the shares are sold from your account. If you do not own the shares (naked call), your broker sells 100 shares short on your behalf, creating a short stock position that you must eventually cover. This is why naked call assignment can result in large losses if the stock has risen significantly above the strike.

How do dividends affect long and short calls?

If a stock pays a dividend, in-the-money call holders may exercise early to capture the dividend. This means short call sellers face early assignment risk around ex-dividend dates. Long call holders can choose to exercise early to receive the dividend, but it is only worthwhile if the dividend exceeds the remaining time value of the option.

Should I sell calls naked or covered?

Covered calls are strongly preferred for most traders. They generate income while limiting upside rather than exposing you to unlimited risk. Naked call selling is a strategy used primarily by professional traders and institutions with sophisticated risk management systems and substantial capital reserves. The risk-reward profile of naked calls is asymmetric in a dangerous direction — many small wins can be wiped out by a single large loss.

Related Articles

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.