Naked Calls & Naked Puts: High-Risk Options Strategies Explained

⚡ Key Takeaways

- Naked (uncovered) options involve selling calls or puts without owning the underlying stock or sufficient collateral

- Naked calls carry theoretically unlimited risk because there is no cap on how high a stock can rise

- Naked puts risk is limited to the strike price minus the premium, but losses can still be enormous

- Margin requirements for naked options are substantial, often 20-30% of the underlying value plus the premium

- Only experienced traders with large accounts and strict risk management should trade naked options

What Are Naked Options?

Naked options (also called uncovered options) are options sold without a corresponding position in the underlying stock. A naked call means selling a call without owning 100 shares. A naked put means selling a put without holding enough cash to buy the shares if assigned.

Naked option selling is one of the highest-risk strategies in options trading. While the probability of profit is typically high (most options expire worthless), the potential losses on any single trade can be catastrophic. This is a strategy reserved for experienced traders with substantial accounts and ironclad discipline.

Most brokers require Level 4 or 5 options approval for naked writing, along with a margin account and minimum account balances, often $25,000 or more.

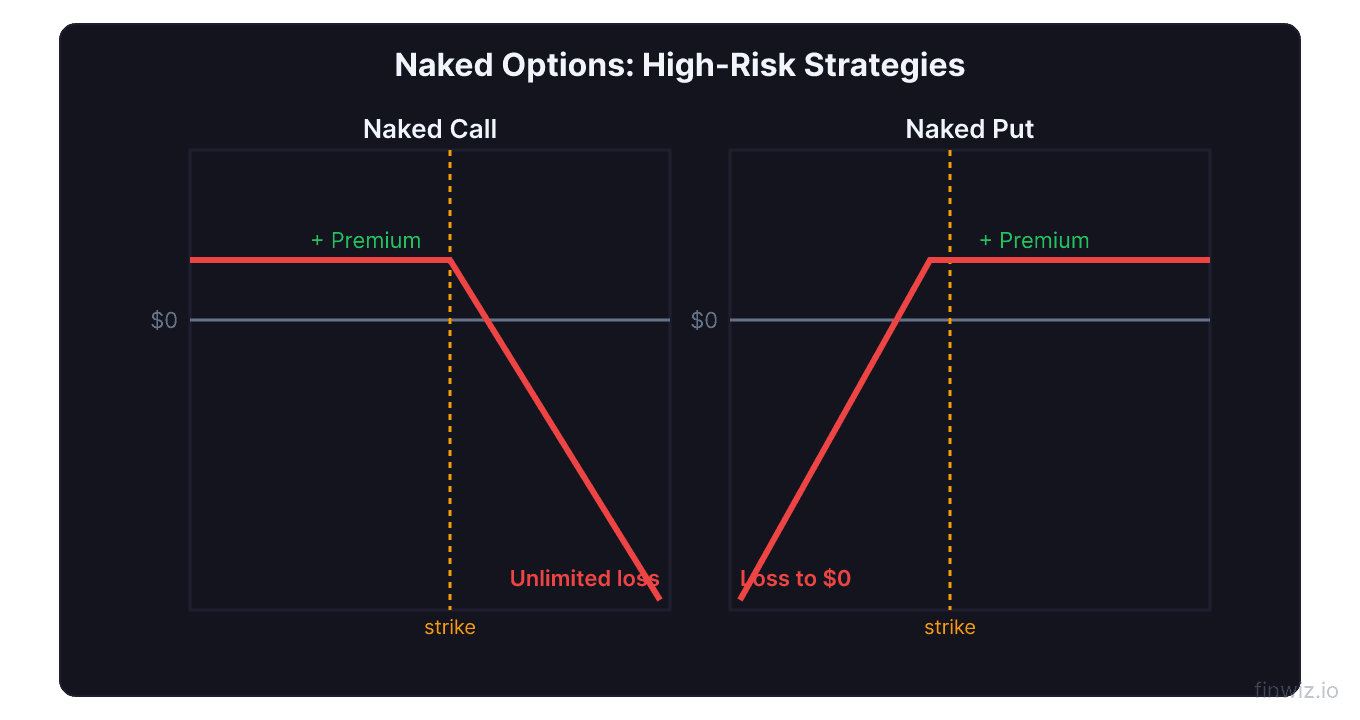

Naked Calls: Unlimited Risk

A naked call is the most dangerous options strategy available to retail traders. You sell a call option without owning the underlying stock, collecting the premium and hoping the stock stays below your strike price.

Example: Stock ABC trades at $100. You sell a $110 naked call for $2.00 per share, collecting $200.

Best case: The stock stays below $110 at expiration. The call expires worthless and you keep the $200.

Worst case: The stock surges to $200. You must buy 100 shares at $200 and deliver them at $110. Your loss: ($200 − $110 − $2) × 100 = $8,800. And if the stock went to $500? Your loss would be $38,800 on a $200 premium.

Naked Call Loss = (Stock Price − Strike Price − Premium Collected) × 100The risk is theoretically unlimited because there is no cap on how high a stock price can go. Short squeezes, buyouts, and unexpected news can send stocks dramatically higher in hours.

| Stock at Expiration | Profit/Loss |

|---|---|

| $100 | +$200 (max profit) |

| $110 | +$200 |

| $112 | $0 (breakeven) |

| $120 | -$800 |

| $150 | -$3,800 |

| $200 | -$8,800 |

| $500 | -$38,800 |

Pro Tip

Naked Puts: Large but Limited Risk

Naked puts are somewhat less dangerous than naked calls because a stock can only fall to zero. When you sell a naked put, you collect the premium and accept the obligation to buy 100 shares at the strike price if assigned.

The distinction between a naked put and a cash-secured put is capital. A cash-secured put has the full purchase price set aside in your account. A naked put uses margin, meaning you can sell puts with far less capital than needed to cover assignment. This leverage amplifies both returns and losses.

Example: Stock DEF trades at $80. You sell a $75 naked put for $1.80 per share, collecting $180.

Naked Put Loss = (Strike Price − Stock Price − Premium Collected) × 100| Stock at Expiration | Profit/Loss |

|---|---|

| $80 | +$180 (max profit) |

| $75 | +$180 |

| $73.20 | $0 (breakeven) |

| $70 | -$320 |

| $60 | -$1,320 |

| $40 | -$3,320 |

| $0 | -$7,320 (max loss) |

The maximum loss is $7,320 on a $180 credit, a risk-reward ratio of more than 40:1 against you. While a stock going to zero is rare, declines of 30-50% are not uncommon during market crashes.

Margin Requirements for Naked Options

Selling naked options requires significant margin. The standard formula (though brokers vary) is:

Naked Call Margin = Max of:For a $100 stock with a $110 naked call sold for $2.00:

- Calculation 1: (20% x $100 x 100) + $200 − $1,000 = $1,200

- Calculation 2: (10% x $100 x 100) + $200 = $1,200

- Margin requirement: $1,200

If the stock rises to $150, the margin requirement jumps dramatically, potentially triggering a margin call. Margin calls force you to either deposit more capital or close positions at a loss, often at the worst possible time.

When Professional Traders Use Naked Options

Despite the risks, professional traders and market makers use naked options regularly. Here is how they manage it:

Portfolio margin accounts. Professionals often use portfolio margin instead of Reg-T margin. Portfolio margin calculates risk across the entire portfolio, often resulting in much lower margin requirements. This is available to accounts with $125,000+ at most brokers.

Small position sizing. Professionals risk a tiny percentage of their portfolio on any single naked position, typically 0.5-2% of total account value as maximum loss.

Strict stop losses. Professional naked sellers close positions when the loss reaches 2-3x the premium collected. They never let a trade spiral into a catastrophic loss.

Diversification across underlyings. Rather than concentrating naked positions in one stock, professionals spread risk across dozens of different stocks and ETFs.

Hedging with further OTM options or VIX products. Some professionals buy cheap, far OTM options as tail-risk hedges against the very moves that destroy naked sellers.

| Professional Practice | Why It Matters |

|---|---|

| Portfolio margin | Lower capital requirements |

| 0.5-2% max risk per trade | Survives inevitable losses |

| Stop at 2-3x premium | Limits catastrophic damage |

| 30+ different underlyings | No single stock can blow up account |

| Tail-risk hedges | Protection against black swan events |

Naked Options vs. Defined-Risk Alternatives

For every naked option strategy, there is a defined-risk alternative that caps your maximum loss:

| Naked Strategy | Defined-Risk Alternative | Trade-Off |

|---|---|---|

| Naked call | Bear call spread | Less premium, capped risk |

| Naked put | Cash-secured put or bull put spread | Less premium, capped risk |

| Naked strangle | Iron condor | Less premium, capped risk |

The defined-risk alternatives collect less premium because you are buying a protective option. But the peace of mind and margin efficiency often make up for the reduced income.

Example comparison:

- Naked put on $100 stock, $95 strike: Premium $2.50, max loss $9,250, margin ~$1,800

- Bull put spread, $95/$90 strikes: Premium $1.50, max loss $350, margin $350

The naked put earns $100 more but risks $8,900 more. On a return-on-risk basis, the spread is often superior.

Pro Tip

Famous Naked Option Blowups

History is littered with stories of traders destroyed by naked options:

The short volatility blowup of February 2018. Traders who had sold naked VIX calls or related products lost everything when the VIX spiked from 13 to 50 in a single day. The XIV ETN lost 96% of its value overnight and was liquidated.

Individual stock short squeezes. GameStop in January 2021 saw shares rise from $20 to $483 in days. Any naked call seller with a $30 or $40 strike faced losses of $44,300 to $45,300 per contract — from a position that collected perhaps $200-$400 in premium.

Earnings surprises. Stocks regularly move 20-30% on earnings. A naked call seller on a stock that gaps up 40% overnight cannot exit before the damage is done.

These events are rare but not impossible. The question is not whether they will happen, but whether your account can survive when they do.

Risk Management Rules for Naked Sellers

If you choose to sell naked options despite the risks, follow these rules:

-

Never risk more than 2% of your account on a single position. If your account is $100,000, your maximum loss on any naked trade should not exceed $2,000.

-

Always use stop losses. Close a naked call at 2-3x the premium collected. Close a naked put at 2-3x the premium collected.

-

Avoid earnings and binary events. Close naked positions before earnings, FDA decisions, or any event that can cause a gap.

-

Monitor positions daily. Naked options require active management. If you cannot watch your positions every day, do not sell naked options.

-

Diversify across sectors and underlyings. Never have more than 20-30% of your margin in a single stock's naked options.

-

Keep cash reserves. Maintain at least 50% of your margin buying power as unused cash. This provides a buffer against margin calls.

-

Avoid meme stocks and low-float names. These are most susceptible to short squeezes and extreme moves. Stick to large-cap, liquid stocks.

Frequently Asked Questions

Why would anyone sell naked options if the risk is so high?

The primary reason is high probability of profit. Most options expire worthless, so naked sellers win the majority of their trades. Additionally, naked options require less capital than owning stock or using defined-risk strategies, allowing for higher return on capital when trades work. The strategy is profitable in aggregate for disciplined traders who manage risk properly, though one catastrophic loss can erase many months of profits.

How much money do I need to sell naked options?

Most brokers require a minimum of $25,000 for naked option approval, though many recommend $50,000-$100,000 or more. Portfolio margin accounts typically require $125,000. Beyond the minimum requirements, you need enough capital to absorb losses without being forced out of positions at the worst time.

Can I sell naked options in a retirement account?

No. IRA and 401(k) accounts do not allow naked option selling because these accounts cannot have a negative balance. You can sell cash-secured puts or covered calls in retirement accounts, but not naked calls or uncovered puts.

What is the difference between a naked put and a cash-secured put?

The strategy is the same — you sell a put and hope the stock stays above the strike. The difference is capital allocation. A cash-secured put has the full cash (strike x 100) set aside to buy shares if assigned. A naked put uses margin, requiring only a fraction of that amount. Naked puts are more capital-efficient but introduce margin call risk.

How do I close a naked option position?

To close a naked call, you buy to close the same call option. To close a naked put, you buy to close the same put option. You can do this at any time during market hours. If the option has lost value (moved in your favor), you buy it back for less than you sold it, pocketing the difference as profit.

Disclaimer

This is educational content, not financial advice. Trading involves risk, and you should consult a qualified financial advisor before making any investment decisions. Past performance does not guarantee future results.

Related Articles

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.