Rolling Options: How to Roll Forward, Up & Down

⚡ Key Takeaways

- Rolling an option means closing an existing position and simultaneously opening a new one with a different expiration or strike

- Rolling out extends the expiration date to buy more time for your trade thesis

- Rolling up or down changes the strike price to adjust your directional exposure

- The goal is to execute the roll for a net credit or minimal net debit

- Rolling is a management tool, not a rescue operation — know when to cut losses instead

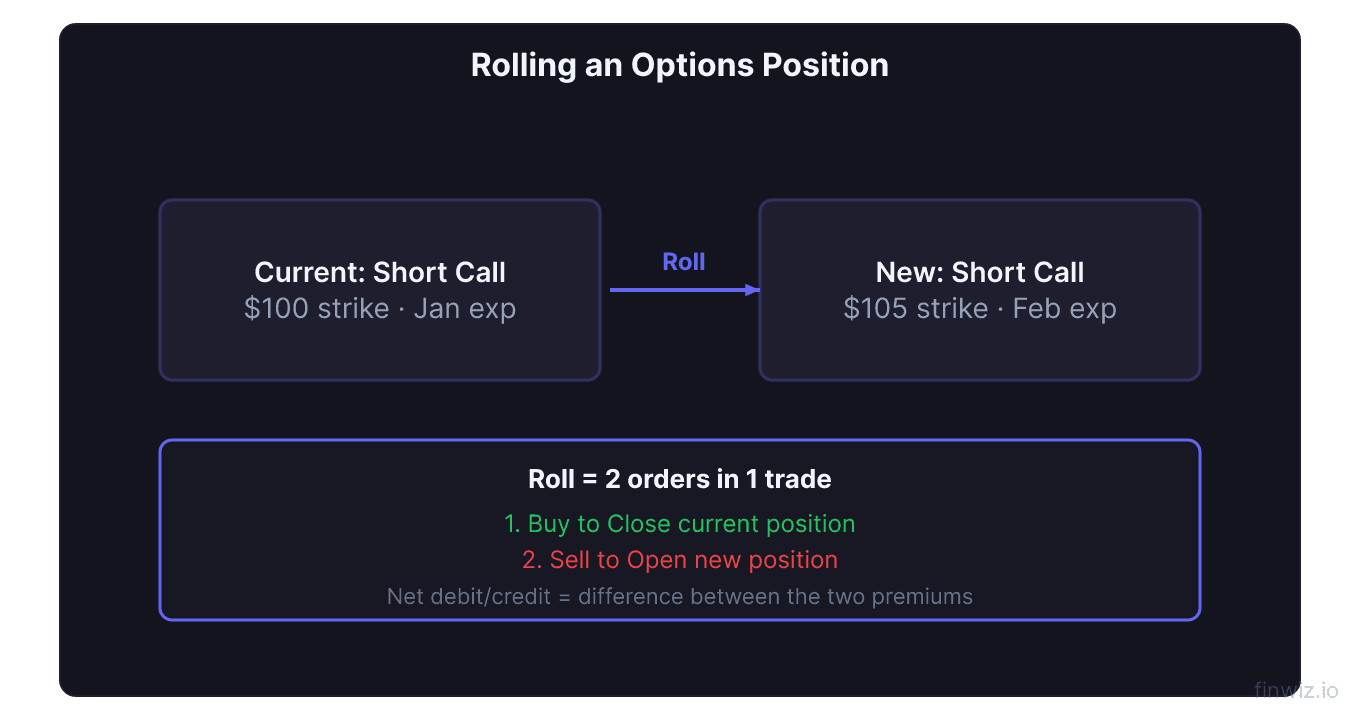

What Is Rolling an Option?

Rolling an option is the process of closing your current option position and simultaneously opening a new one with different terms. It is a single strategic move executed as two legs: a closing trade and an opening trade. Most brokers let you enter this as a single order, which helps you get better fills than executing each leg separately.

Rolling is used to manage existing positions that need adjustment. If your covered call is about to be assigned and you want to keep your shares, you roll. If your short put is threatened and you want to avoid assignment, you roll. If your long call is running out of time but your thesis remains intact, you roll.

The three types of rolls — out, up, and down — each serve a different purpose. Understanding when and how to use each type separates reactive traders from proactive ones.

Rolling Out: Extending the Expiration

Rolling out (also called rolling forward) means moving your option to a later expiration date while keeping the same strike price. This is the most common type of roll and is used primarily to buy more time.

For short options (covered calls, cash-secured puts), rolling out collects additional premium. You buy back the near-term option and sell a later-dated option at the same strike. Because the later-dated option has more extrinsic value, this trade typically generates a net credit.

Example: You sold an AAPL $190 covered call expiring this Friday for $3.00. AAPL trades at $192, and you want to keep your shares.

- Buy to close: AAPL $190 call, this Friday, at $2.50

- Sell to open: AAPL $190 call, next month, at $5.50

- Net credit: $3.00 ($5.50 received minus $2.50 paid)

You keep your shares, collect an additional $300, and extend the obligation by one month.

For long options, rolling out costs money. You sell the near-term option (capturing remaining value) and buy a later-dated option (paying more). The net debit is the price of extra time.

Net Credit/Debit = Premium Received (New Option) − Premium Paid (Closing Old Option)Rolling Up: Raising the Strike Price

Rolling up means moving to a higher strike price. This is used with call positions when the stock has risen and you want to adjust your exposure.

For covered call sellers, rolling up creates more room for the stock to appreciate before assignment. If you sold a $150 call and the stock surged to $160, rolling up to a $165 call lets you capture more upside.

Example: You sold a GOOGL $170 covered call. GOOGL rallies to $178.

- Buy to close: GOOGL $170 call at $9.00

- Sell to open: GOOGL $180 call (same expiration) at $3.50

- Net debit: $5.50

You raised your cap by $10 but paid $5.50 for the privilege. This makes sense if you believe GOOGL will continue higher. If you combine rolling up with rolling out, you can often turn this net debit into a credit.

Rolling Down: Lowering the Strike Price

Rolling down means moving to a lower strike price. This is most commonly used with put positions when the stock has declined.

For put sellers, rolling down means accepting a lower purchase price if assigned, which can be appropriate if the stock's value has deteriorated. For call sellers, rolling down captures more premium but brings the short strike closer to the current stock price.

Example: You sold an AMD $150 put for $4.00. AMD drops to $140.

- Buy to close: AMD $150 put at $11.50

- Sell to open: AMD $140 put (later expiration) at $8.00

- Net debit: $3.50

You lowered your assignment price from $150 to $140, better reflecting AMD's new trading range. The $3.50 debit reduces your total premium collected, but your new effective purchase price if assigned is $140 minus net premium collected — a more accurate reflection of fair value.

Combining Rolls: Up and Out, Down and Out

The most powerful rolls combine strike and time adjustments simultaneously.

Rolling up and out on covered calls is the classic move when you are bullish but want to avoid assignment. You raise the strike and extend the expiration, often achieving a net credit.

Rolling down and out on short puts is the defensive move when a stock pulls back. You lower the strike to reduce your assignment price and extend the expiration to collect more premium.

| Roll Type | When to Use | Typical Cost | Goal |

|---|---|---|---|

| Out only | Need more time, same strike works | Credit (short options) | Buy time |

| Up only | Stock rallied, need higher cap | Debit | More upside room |

| Down only | Stock dropped, need lower assignment | Debit | Lower entry price |

| Up and out | Bullish, avoid call assignment | Usually credit | Keep shares + collect premium |

| Down and out | Bearish pressure on short put | Credit or small debit | Avoid assignment + lower strike |

Pro Tip

Cost Analysis: When Rolling Makes Sense

Not every roll is a good roll. Here is how to evaluate whether rolling is the right decision.

Calculate the total premium picture. Add up all premiums collected and paid across the original trade and the roll. If you are still net positive, the roll is working. If you have turned a winning trade into a net debit position after rolling, reconsider.

Compare to closing and restarting. Sometimes it is cheaper to close the position entirely and sell a new option from scratch rather than rolling. This is especially true when the roll involves a large debit.

Consider the Greeks of the new position. After rolling, you have a new option with different delta, theta, and vega characteristics. Make sure these align with your current outlook. Rolling a covered call out six months gives you premium but reduces theta decay benefits because longer-dated options decay more slowly.

Set a maximum number of rolls. A common discipline is to limit yourself to two or three rolls on any single position. If you have rolled three times and the trade still is not working, it is time to close and reassess. Endless rolling traps capital in losing positions.

Total Position P&L = Sum of All Premiums Collected − Sum of All Premiums Paid ± Stock P&L (if assigned)Common Rolling Mistakes

Rolling to avoid a loss. Rolling should be a proactive management tool, not an emotional escape from taking a loss. If the fundamental thesis has broken, close the trade. Rolling an INTC put after the company cuts guidance and slashes dividends just delays the inevitable loss.

Rolling for a large debit. Any roll that costs more than the original premium collected is a warning sign. You are spending money to stay in a deteriorating position.

Ignoring options assignment risk on the new position. After rolling, reassess whether you are comfortable with assignment at the new strike. Do not roll to a strike that represents a price you would not pay for the stock.

Rolling too early. Let theta work for you. If your short option still has 20 days to expiration and plenty of extrinsic value, there is no urgency to roll. Wait until the option approaches expiration or your short strike before acting.

Frequently Asked Questions

Can I roll any type of option?

Yes. You can roll calls, puts, covered calls, cash-secured puts, and even individual legs of spreads. The mechanics are the same: close the existing leg and open a new one. However, rolling spread legs independently can create temporary unbalanced positions, so execute carefully.

Does rolling reset my cost basis for taxes?

Rolling is treated as two separate transactions for tax purposes. Closing the first option generates a realized gain or loss. Opening the second option starts a new position with its own cost basis. Consult a tax professional for specifics, as wash sale rules may apply if you roll at a loss and re-establish a substantially identical position.

How do I know when to roll versus when to close?

Roll when your thesis on the underlying stock remains intact and the roll can be executed for a credit or a small debit. Close when the thesis has changed, the roll requires a large debit, or you have already rolled the position multiple times without improvement. The decision is ultimately about whether you still want exposure to the stock at the new terms.

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.