Protective Put: How to Insure Your Stock Position

⚡ Key Takeaways

- A protective put involves buying a put option on a stock you already own to limit downside risk

- The strategy acts like insurance, capping your maximum loss at the strike price minus what you paid for the put

- Protective puts cost money (the premium), which reduces your overall return if the stock rises or stays flat

- This strategy is superior to stop-loss orders during gaps, earnings announcements, and overnight risk events

- Protective puts let you stay long while sleeping well at night during uncertain markets

What Is a Protective Put?

A protective put is an options strategy where you buy a put option on a stock you already own. The put gives you the right to sell your shares at the strike price regardless of how far the stock drops, effectively placing a floor under your position.

Think of it as buying insurance on your home. You pay a premium, and in return, you are protected against catastrophic loss. If nothing bad happens, you lose the premium. If disaster strikes, the insurance pays off.

This is one of the simplest and most intuitive options strategies. If you own 100 shares of a stock and buy one put contract, you have a protective put. The combined position is sometimes called a married put when the stock and put are purchased at the same time.

How a Protective Put Works

You own 100 shares of stock ABC trading at $150. Earnings are in two weeks, and you are worried about a potential miss. You do not want to sell your shares because you are bullish long-term, but you want protection.

Trade setup:

- Own 100 shares of ABC at $150

- Buy 1 ABC $145 put, 21 DTE, for $3.00

Your total cost of protection is $300 (the put premium). Here is what happens at various prices at expiration:

| Stock Price | Stock P/L | Put Value | Put P/L | Total P/L |

|---|---|---|---|---|

| $170 | +$2,000 | $0 | -$300 | +$1,700 |

| $160 | +$1,000 | $0 | -$300 | +$700 |

| $150 | $0 | $0 | -$300 | -$300 |

| $145 | -$500 | $0 | -$300 | -$800 |

| $140 | -$1,000 | $500 | -$300 | -$800 |

| $130 | -$2,000 | $1,500 | -$300 | -$800 |

| $100 | -$5,000 | $4,500 | -$300 | -$800 |

No matter how far the stock falls, your maximum loss is capped at $800 (the $5 difference between your stock price and the put strike, plus the $3 premium).

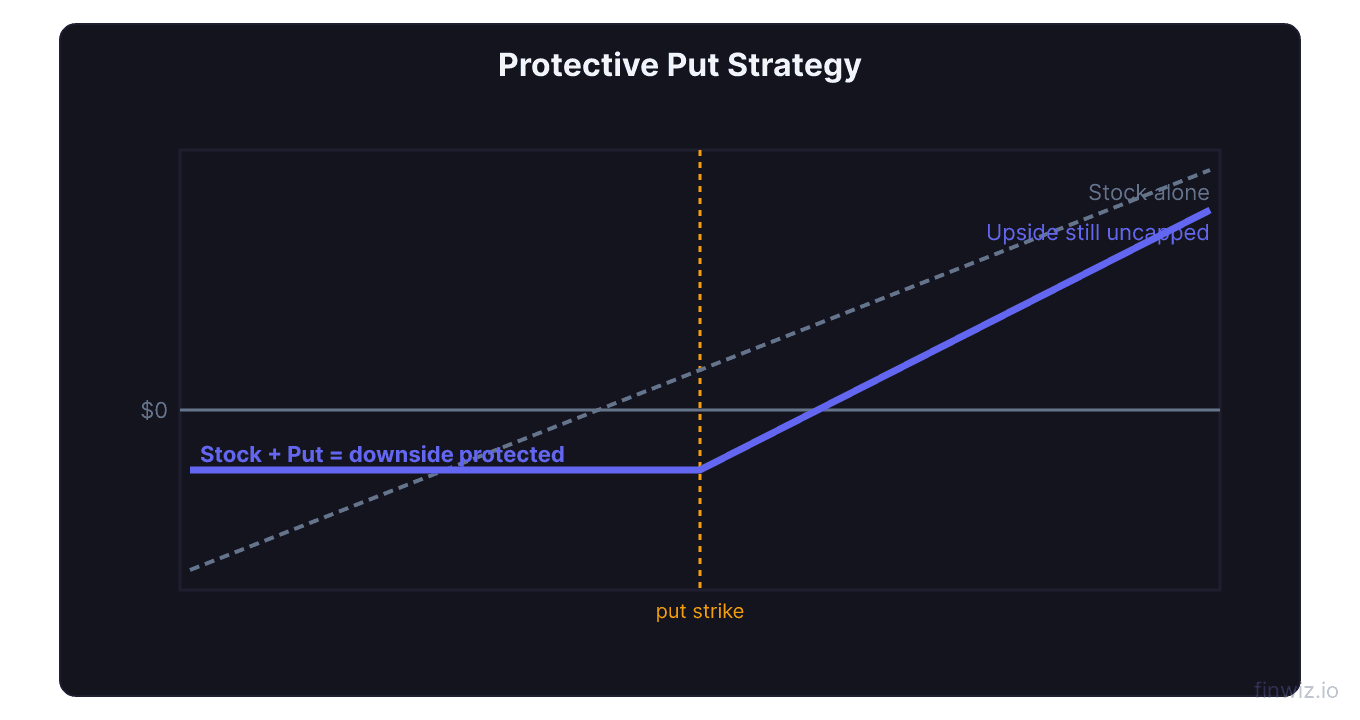

Payoff Diagram Description

The protective put payoff profile looks like a long call option. On the left side (below the strike), the line is flat because losses are capped. On the right side (above the strike plus premium), the line rises at a 45-degree angle because you participate fully in upside gains.

The breakeven point is the current stock price plus the put premium. In our example, the stock needs to reach $153 for you to break even. Below $153 but above $145, you have a partial loss. Below $145, losses are locked at $800.

This is the key tradeoff: you pay a premium for downside protection, which raises your breakeven and reduces returns in neutral or mildly bullish scenarios.

The Cost of Protection

Premium cost is the biggest drawback of protective puts. Here is how different put strikes affect your protection cost and loss limits:

| Put Strike | Premium | Max Loss | Breakeven | Protection Level |

|---|---|---|---|---|

| $150 ATM | $5.00 | $500 | $155 | Full from $150 |

| $145 (3% OTM) | $3.00 | $800 | $153 | From $145 down |

| $140 (7% OTM) | $1.50 | $1,150 | $151.50 | From $140 down |

| $135 (10% OTM) | $0.80 | $1,580 | $150.80 | From $135 down |

ATM puts offer the tightest protection but cost the most. Deep OTM puts are cheap but only protect against large drops. Most traders buy puts 3-7% out of the money as a balance between cost and protection.

Pro Tip

Protective Put vs. Stop-Loss Order

Many traders think a stop-loss order provides the same protection as a put. It does not. Here is why:

| Feature | Protective Put | Stop-Loss Order |

|---|---|---|

| Gap protection | Yes | No |

| Overnight protection | Yes | No |

| Guaranteed exit price | Yes (strike price) | No (market order) |

| Cost | Premium paid | Free |

| Slippage risk | None | Can be severe |

| Keeps position open | Yes | No (sells shares) |

| Whipsaw risk | None | High |

The gap problem is critical. If a stock closes at $150 and opens at $120 after bad earnings, your stop-loss at $145 fills at $120 or worse. Your protective put still lets you sell at $145.

Real-world example: In February 2018, XIV (a volatility ETF) dropped from $99 to $4.22 after hours in a single session. Stop-losses set at $90 would have filled near $4. A protective put at $90 would have saved holders $86 per share.

Stop-losses also get triggered by intraday wicks. A stock might dip 3%, trigger your stop, then immediately recover. You are sold out at the bottom. With a protective put, you ride through the volatility because you still hold both the stock and the put.

When to Use Protective Puts

Before earnings announcements. Earnings are binary events where stocks can gap 10-20% in either direction. If you are long-term bullish but worried about a single quarter, buying a short-term put before the announcement provides defined-risk protection.

During macro uncertainty. When the Federal Reserve is about to make a major decision, or geopolitical risks are elevated, protective puts let you stay invested without taking unhedged risk.

When you have large concentrated positions. If a single stock represents 20% or more of your portfolio, the risk of a catastrophic gap down justifies the cost of protection.

Before extended market closures. Long weekends and holidays introduce overnight risk without the ability to react. A protective put covers you during market closures.

Tax management situations. If selling would trigger a large short-term capital gains tax, you can buy a put instead of selling. This locks in a minimum exit price without creating a taxable event (subject to constructive sale rules for ATM or ITM puts).

Protective Put vs. Collar Strategy

A collar adds a short call on top of the protective put. You own stock, buy a put, and sell a call. The call premium offsets the put cost, sometimes creating a zero-cost collar.

| Strategy | Cost | Upside | Downside Protection |

|---|---|---|---|

| Protective put | Put premium | Unlimited | Yes, from strike |

| Collar | Reduced or zero | Capped at call strike | Yes, from put strike |

If you are willing to cap your upside, the collar eliminates the cost disadvantage of the protective put. If you want unlimited upside participation, stick with the put alone. See our full guide on the collar strategy.

Choosing the Right Expiration

Short-term puts (1-2 weeks) work for specific events like earnings. They are cheaper but expire quickly. If the event passes without incident, the put expires worthless and you move on.

Monthly puts (30-45 DTE) balance cost and duration. They give you several weeks of protection and still have reasonable premiums.

Quarterly puts (60-90 DTE) cost more in absolute terms but less per day of protection. If you want coverage for an extended uncertain period, longer-dated puts are more cost-efficient on a daily basis.

Daily Cost of Protection = Put Premium / Days to ExpirationExample: A 30-day put costs $3.00 on a $150 stock. Daily cost = $0.10. Annualized cost = ($3 / $150) x (365 / 30) x 100 = 24.3%. A 90-day put costs $5.50. Daily cost = $0.061. Annualized cost = 13.4%. The longer-dated put is cheaper per day.

Rolling Protective Puts

When your put is about to expire and you still want protection, you roll it by closing the current put and opening a new one with a later expiration.

When to roll: Roll with 5-7 days remaining before expiration. At this point, the put has lost most of its time value if OTM, and the new put will be relatively cheaper.

How to roll efficiently: Use a single order (sell current put, buy new put) as a spread to minimize commissions and slippage. Most brokers offer roll orders as a built-in feature.

Adjusting the strike: If the stock has risen since you bought the original put, consider rolling to a higher strike to move your floor up. If the stock has fallen, keep the same strike or adjust based on your new risk assessment.

Calculating Your True Cost Basis

When you add protective puts, your effective cost basis changes:

Effective Cost Basis = Stock Purchase Price + Put Premium PaidExample: You bought stock at $150 and a $140 put for $2.00.

- Effective cost basis: $152

- Maximum loss per share: $150 - $140 + $2 = $12

- Maximum loss percentage: $12 / $152 = 7.9%

This means even in a worst-case scenario, you lose no more than 7.9% of your invested capital (including the put cost).

Common Mistakes with Protective Puts

Buying too much protection. ATM puts are expensive. Most traders are better served by puts 5-7% OTM, which protect against catastrophic moves while keeping costs reasonable.

Holding puts too long. Theta decay accelerates in the final two weeks. If the risk event has passed and the stock is fine, sell the put to recoup remaining time value rather than letting it expire worthless.

Ignoring implied volatility. Buying puts when IV is already elevated (such as right before earnings when everyone is hedging) means you overpay. The put loses value from IV crush even if the stock drops modestly.

Using protective puts on every position. The cost is prohibitive for permanent, portfolio-wide protection. Use them selectively on your largest or most volatile positions around specific risk events.

Frequently Asked Questions

How much does a protective put cost?

Typically 1-5% of the stock price for a monthly put, depending on how far out of the money you go and the stock's implied volatility. A $150 stock might have protective puts ranging from $0.80 (10% OTM) to $5.00 (ATM) for a 30-day expiration.

Can I write calls against my protective put position?

Yes. If you own stock and buy a put, adding a short call creates a collar. The call premium offsets the put cost. This is a common adjustment when you want to reduce or eliminate the cost of protection.

Is a protective put the same as a married put?

A married put specifically refers to buying a put at the same time you buy the stock. A protective put is broader and includes buying a put on stock you already own. The payoff profile is identical. The distinction matters mainly for tax purposes and cost basis tracking.

Should I use a protective put or just sell the stock?

If you are long-term bullish and want to maintain your position through a short-term risk, the protective put is better. If you are no longer bullish, just sell. The protective put costs money, so only use it when you want to stay in the position but need temporary downside protection.

What happens if my put expires in the money?

If the stock is below the put strike at expiration, the put will typically be auto-exercised, selling your 100 shares at the strike price. If you want to keep your shares, sell the put before expiration to capture its intrinsic value instead of allowing exercise.

Disclaimer

This is educational content, not financial advice. Trading involves risk, and you should consult a qualified financial advisor before making any investment decisions. Past performance does not guarantee future results.

Related Articles

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.