Options Premium: What Determines the Price of an Option

⚡ Key Takeaways

- An option's premium is made up of intrinsic value plus time value (also called extrinsic value)

- Intrinsic value is the amount an option is in-the-money and represents real, tangible worth

- Time value reflects the probability that the option could gain additional value before expiration

- Implied volatility is the single largest driver of time value and can inflate or crush premiums independently of price movement

- Understanding premium composition helps you avoid overpaying for options and identify mispriced contracts

What Is an Options Premium?

The options premium is the price you pay to buy an option contract or the price you receive when you sell one. It is quoted on a per-share basis, so a premium of $5.00 means the contract costs $500 total (100 shares per contract).

The premium is not an arbitrary number. It is determined by a combination of measurable factors that you can analyze before entering a trade. Breaking the premium into its components lets you understand exactly what you are paying for — and whether the price is reasonable.

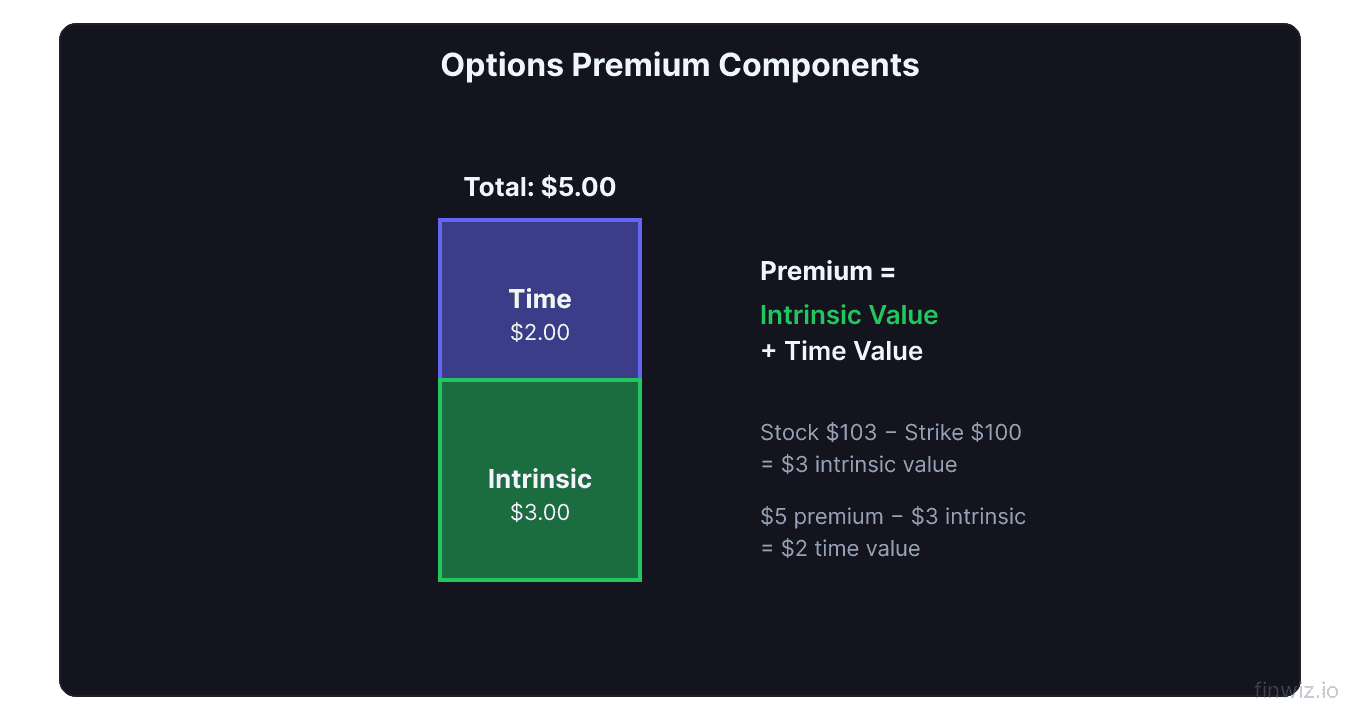

Every option premium consists of two parts:

Option Premium = Intrinsic Value + Time ValueUnderstanding each component separately is the key to making informed options trades. Traders who ignore premium composition often buy options that are too expensive relative to the expected move, or sell options that are too cheap relative to the risk they are taking.

Intrinsic Value: The Built-In Worth

Intrinsic value is the portion of the premium that reflects the option's moneyness. It is the amount by which the option is in-the-money. If an option is at-the-money or out-of-the-money, its intrinsic value is zero.

Suppose NVDA trades at $900. A $870 call option is $30 in-the-money, so it has $30 of intrinsic value. If that call is trading at $42.00, the remaining $12.00 is time value.

Intrinsic Value (Call) = Stock Price − Strike PriceIntrinsic Value (Put) = Strike Price − Stock PriceIntrinsic value cannot be negative. If the formula yields a negative number, the intrinsic value is simply zero and the entire premium consists of time value.

Intrinsic value is the "floor" of an option's worth. The option can never trade below its intrinsic value in a rational market because arbitrageurs would instantly buy the option and exercise it for a risk-free profit. This means deep in-the-money options trade very close to their intrinsic value, with minimal time value added.

Time Value: Paying for Possibility

Time value (also called extrinsic value) is everything in the premium beyond intrinsic value. It represents the market's assessment of the probability that the option will gain additional value before expiration.

Time Value = Option Premium − Intrinsic ValueThree factors drive time value:

Time to expiration — More time means more opportunity for the stock to move favorably. An AAPL $180 call expiring in 90 days will have significantly more time value than the same strike expiring in 7 days. This decay is measured by the Greek known as theta, which you can study further in our options Greeks guide.

Implied volatility — Higher implied volatility means the market expects larger price swings, which increases the probability of the option finishing in-the-money. This directly inflates time value. Before earnings reports, implied volatility often spikes, making options on that stock significantly more expensive even if the stock has not moved.

Interest rates and dividends — These have a smaller impact but still affect the premium. Higher interest rates slightly increase call premiums and decrease put premiums. Upcoming dividends decrease call premiums and increase put premiums because the stock price drops by the dividend amount on the ex-date.

How Implied Volatility Inflates and Crushes Premiums

Implied volatility (IV) deserves special attention because it is the most misunderstood component of the premium. IV does not predict direction — it predicts magnitude. When IV is high, the market expects a large move, and options premiums reflect that expectation.

Consider TSLA trading at $250 with two different IV environments:

| Component | Low IV (30%) | High IV (70%) |

|---|---|---|

| TSLA $250 Call (30 DTE) | $8.50 | $19.80 |

| Intrinsic Value | $0.00 | $0.00 |

| Time Value | $8.50 | $19.80 |

Both options are at-the-money with zero intrinsic value. The entire premium is time value. Yet the high-IV option costs more than double. If you buy the high-IV option and volatility contracts back to normal levels — even if the stock moves in your direction — you can lose money. This is called IV crush and it is the most common way inexperienced options traders lose on trades where they get the direction right.

Pro Tip

Premium Decay Over Time

Time value does not decay in a straight line. It accelerates as expiration approaches. An option with 60 days to expiration might lose $0.03 per day to theta, but that same option with 10 days left might lose $0.15 per day.

This has practical implications for both buyers and sellers:

Option buyers fight theta every day. The longer you hold an option without a favorable move, the more value bleeds away. This is why directional option buyers should have a defined time horizon and exit plan.

Option sellers benefit from theta. Selling options with 30 to 45 days to expiration captures the steepest portion of the decay curve while still leaving enough time value to collect meaningful premium.

The at-the-money strike always has the most time value in dollar terms. As you move further in-the-money or out-of-the-money, time value decreases. This is why ATM options are most affected by theta decay on a dollar basis.

Putting It All Together: Reading a Premium

When you see an option quoted at a certain price, you should immediately decompose it. Take SPY at $510 with a $500 call trading at $14.50 and 21 days to expiration:

- Intrinsic value: $510 − $500 = $10.00

- Time value: $14.50 − $10.00 = $4.50

- Time value percentage: $4.50 / $14.50 = 31%

You are paying $10.00 for built-in value and $4.50 for time and volatility. If you hold this option to expiration and SPY stays at $510, you will lose that $4.50 in time value — a 31% loss from decay alone despite the stock not moving against you.

This analysis should be automatic before every trade. Knowing exactly what you are paying for prevents the common mistake of buying options that need an unrealistically large move just to overcome the time value embedded in the premium.

Pro Tip

FAQ

Why do options with the same strike and expiration have different premiums for calls and puts?

Call and put premiums differ because of put-call parity, which accounts for the cost of carrying the underlying stock (interest rates) and any dividends expected before expiration. In practice, for most stocks, the differences are small, but they become noticeable on high-dividend stocks or when interest rates are elevated.

Can an option's premium increase even if the stock does not move?

Yes. If implied volatility rises, the time value component of the premium increases, pushing the total premium higher. This commonly happens before earnings announcements, FDA decisions, or major economic reports when the market anticipates a large price swing regardless of direction.

How do I know if an option is overpriced?

Compare the current implied volatility to the stock's historical volatility and its IV rank over the past year. If IV is elevated relative to history, the option is more expensive than usual. You can also compare the option's expected move (derived from the premium) to the stock's actual average move over similar time periods to gauge whether the market is overpricing the expected range.

Related Articles

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.