Straddles & Strangles: Trading Volatility Regardless of Direction

⚡ Key Takeaways

- A straddle buys an ATM call and ATM put at the same strike; a strangle buys an OTM call and OTM put at different strikes

- Both strategies profit from large moves in either direction, making them ideal for high-volatility events

- Straddles cost more but have a closer breakeven; strangles cost less but require a bigger move to profit

- Time decay is the primary enemy of both strategies, eroding value daily when the stock stays flat

- IV crush after earnings can devastate long straddles and strangles even if the stock moves in your favor

Straddles and Strangles Explained

Straddles and strangles are options strategies designed to profit from large price movements in either direction. Unlike directional strategies that require you to predict whether a stock will go up or down, these strategies only require that the stock moves — a lot.

Both strategies involve buying a call option and a put option simultaneously. The difference lies in strike selection:

- A straddle uses the same strike price for both the call and put (typically ATM)

- A strangle uses different strike prices — an OTM call and an OTM put

These are popular strategies for earnings plays, FDA announcements, and other binary events where a big move is expected but the direction is uncertain.

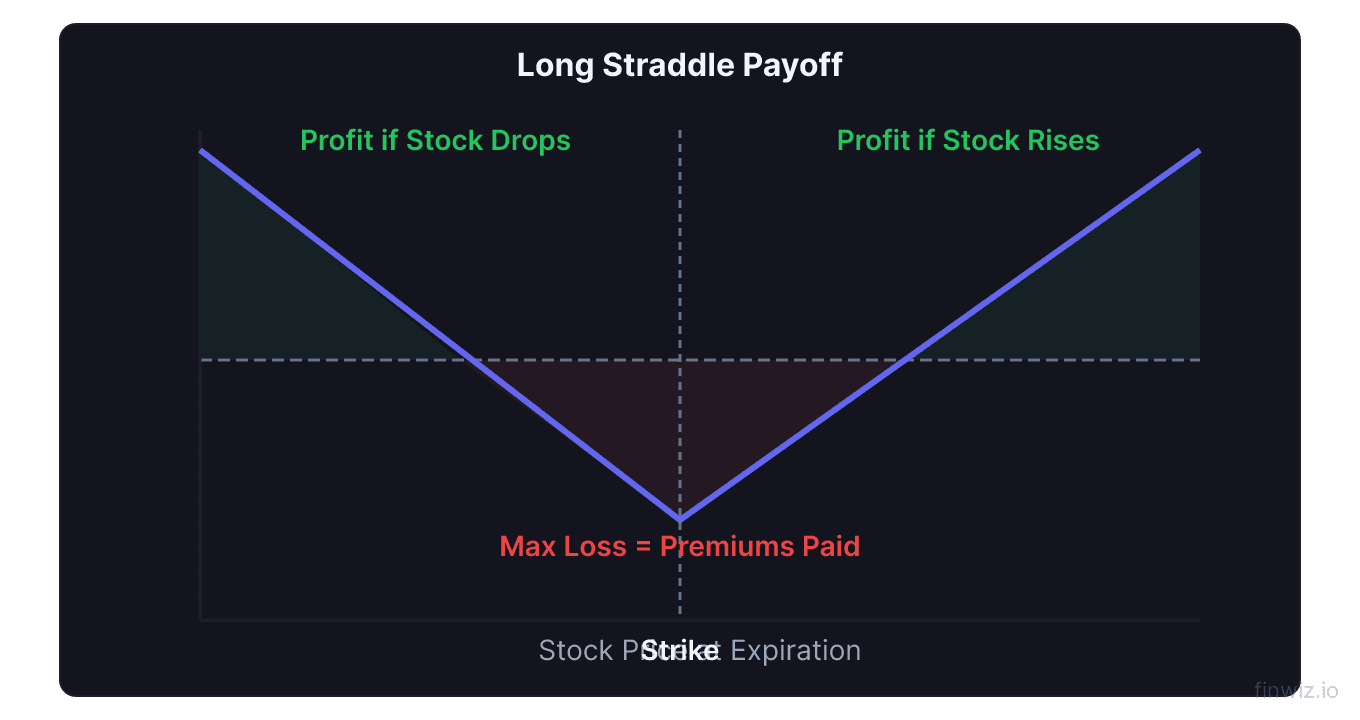

The Long Straddle

A long straddle involves buying one ATM call and one ATM put with the same strike price and expiration date.

Example: Stock XYZ trades at $100. You buy the following 30-day straddle:

| Leg | Action | Strike | Premium |

|---|---|---|---|

| 1 | Buy call | $100 | $3.50 |

| 2 | Buy put | $100 | $3.20 |

| Total cost | $6.70 |

Total investment: $6.70 per share, or $670 per contract.

Straddle Breakeven (upside) = Strike + Total Premium = $100 + $6.70 = $106.70The stock must move at least 6.7% in either direction just to break even. This is a significant hurdle that illustrates the high cost of straddles.

| Stock at Expiration | Call Value | Put Value | Total Value | Net P/L |

|---|---|---|---|---|

| $80 | $0 | $20.00 | $20.00 | +$1,330 |

| $90 | $0 | $10.00 | $10.00 | +$330 |

| $93.30 | $0 | $6.70 | $6.70 | $0 (breakeven) |

| $97 | $0 | $3.00 | $3.00 | -$370 |

| $100 | $0 | $0 | $0 | -$670 (max loss) |

| $103 | $3.00 | $0 | $3.00 | -$370 |

| $106.70 | $6.70 | $0 | $6.70 | $0 (breakeven) |

| $110 | $10.00 | $0 | $10.00 | +$330 |

| $120 | $20.00 | $0 | $20.00 | +$1,330 |

The worst outcome is the stock finishing exactly at $100 — both options expire worthless and you lose the entire $670.

The Long Strangle

A long strangle involves buying one OTM call and one OTM put with different strike prices and the same expiration date.

Example: Stock XYZ at $100. You buy the following 30-day strangle:

| Leg | Action | Strike | Premium |

|---|---|---|---|

| 1 | Buy call | $105 | $1.80 |

| 2 | Buy put | $95 | $1.50 |

| Total cost | $3.30 |

Total investment: $3.30 per share, or $330 per contract — roughly half the straddle's cost.

Strangle Breakeven (upside) = Call Strike + Total Premium = $105 + $3.30 = $108.30The stock must move 8.3% up or 8.3% down to break even. This is a larger move than the straddle requires, but the trade costs less.

| Stock at Expiration | Call Value | Put Value | Total Value | Net P/L |

|---|---|---|---|---|

| $80 | $0 | $15.00 | $15.00 | +$1,170 |

| $91.70 | $0 | $3.30 | $3.30 | $0 (breakeven) |

| $95-$105 | $0 | $0 | $0 | -$330 (max loss) |

| $108.30 | $3.30 | $0 | $3.30 | $0 (breakeven) |

| $120 | $15.00 | $0 | $15.00 | +$1,170 |

The strangle has a wider max-loss zone ($95 to $105 versus just $100 for the straddle) but a lower total cost, making it more capital-efficient for large expected moves.

Straddle vs. Strangle: Which to Choose?

| Feature | Long Straddle | Long Strangle |

|---|---|---|

| Cost | Higher | Lower |

| Breakeven distance | Closer | Further |

| Max loss zone | Single point (strike) | Range (between strikes) |

| Max loss amount | Higher (more premium) | Lower (less premium) |

| Best for | Moderate expected moves | Large expected moves |

| Capital required | More | Less |

| Probability of profit | Higher | Lower |

Choose a straddle when:

- You expect a moderate-to-large move

- You want the closest breakeven points

- You can afford the higher premium

Choose a strangle when:

- You expect a very large move

- You want to spend less capital

- You are comfortable with a wider no-profit zone

Pro Tip

Earnings Plays with Straddles and Strangles

The most common use of straddles and strangles is earnings trades. The logic is straightforward: earnings create uncertainty, uncertainty drives big moves, and straddles/strangles profit from big moves.

However, there is a critical problem: IV crush.

Before earnings, implied volatility spikes because the market prices in the expected move. After earnings, IV collapses back to normal levels. This IV crush can destroy the value of your straddle or strangle even if the stock moves in your favor.

Example of IV crush destroying a straddle:

- Pre-earnings straddle cost: $8.00 (IV at 55%)

- Stock moves 5% from $100 to $105

- Post-earnings IV drops to 25%

- Straddle value: $5.80

- Loss: $2.20 per share despite a 5% move

The stock moved 5%, but the straddle lost money because the IV crush was worth more than the directional move.

How to avoid IV crush losses:

- Compare the straddle price to the expected move. If the ATM straddle costs $8.00, the market expects an $8 move. You only profit if the stock moves MORE than $8.

- Buy straddles early. Purchase 2-3 weeks before earnings when IV has not yet spiked to its peak. Sell the straddle right before the announcement to capture the IV expansion without holding through the crush.

- Use shorter-dated options. Weekly options have less extrinsic value to crush, though they also have less time for the trade to work.

Time Decay: The Enemy of Both Strategies

Both straddles and strangles have significant negative theta. You own two options, and both decay every day. This means:

- A flat stock costs you money daily

- You need the stock to move enough each day just to overcome time decay

- The closer to expiration, the faster both options lose value

| Days to Expiration | Daily Theta (approximate) | Weekly Cost |

|---|---|---|

| 60 | -$0.06 | $42 |

| 30 | -$0.09 | $63 |

| 14 | -$0.14 | $98 |

| 7 | -$0.22 | $154 |

At 7 DTE, your straddle is losing $22 per day ($154/week). If the stock moves less than $0.22 per day, you are losing money.

This is why straddles and strangles require quick, large moves. Slow, grinding trends do not work because time decay outpaces the directional gain.

Short Straddles and Strangles

Selling straddles and strangles is the opposite trade — you collect premium and profit when the stock stays flat or moves only slightly.

Short straddle: Sell ATM call and ATM put. Profit zone is narrow but premium collected is high. Risk is unlimited on both sides.

Short strangle: Sell OTM call and OTM put. Wider profit zone, less premium. Risk is unlimited on both sides.

| Feature | Short Straddle | Short Strangle |

|---|---|---|

| Premium collected | High | Moderate |

| Profit zone | Narrow | Wide |

| Max risk | Unlimited | Unlimited |

| Theta benefit | Strong | Strong |

| IV crush benefit | Strong | Strong |

Short strangles are extremely popular among professional options sellers, especially when the defined-risk version (iron condor) is used to cap the unlimited risk.

Pro Tip

Managing Straddles and Strangles

For long positions:

- Close winners at 25-50% profit. Straddles rarely reach maximum theoretical profit. Take what the market gives you.

- Close losers at 25-50% loss. If the stock is not moving and theta is eating your position, cut your losses early.

- Leg out when directional. If the stock starts trending strongly in one direction, consider closing the losing leg to reduce cost. This converts your straddle into a directional bet.

- Do not hold through expiration. Time decay accelerates dramatically in the final week. If the trade has not worked by 7-10 DTE, close it.

For short positions:

- Close winners at 50% of max profit. Collecting half the premium with time remaining reduces risk.

- Close losers at 2x the premium. If the stock breaks out and your loss reaches twice the credit collected, close to prevent catastrophic damage.

- Roll the tested side. If the stock threatens one strike, roll that leg further OTM to give yourself more room.

Frequently Asked Questions

What is the difference between a straddle and a strangle?

A straddle uses the same strike for both the call and put (typically ATM), while a strangle uses different strikes (OTM call and OTM put). Straddles cost more but have a tighter breakeven. Strangles cost less but require a larger move to profit.

Are straddles good for earnings trades?

Straddles can work for earnings, but IV crush is a major risk. The pre-earnings IV inflation means you are paying a premium for the expected move. You only profit if the actual move exceeds the expected move (approximated by the straddle price). Many traders prefer buying straddles weeks before earnings to capture IV expansion, then selling before the announcement.

How much does the stock need to move for a straddle to profit?

The stock needs to move more than the total premium paid in either direction. If the straddle costs $6.00, the stock must move more than $6 (6% for a $100 stock) from the strike price by expiration. Before expiration, the breakeven distance is smaller because the options still have time value.

Can I sell a straddle or strangle in a small account?

Selling naked straddles and strangles requires significant margin and is not recommended for small accounts. The undefined risk means a single bad trade can wipe out the account. Small account traders should use iron condors or iron butterflies instead, which provide similar exposure with defined risk and lower margin requirements.

Which is better for high volatility events — straddle or strangle?

For extremely high volatility events (potential 15%+ moves), the strangle is usually better because it is cheaper and the expected move is large enough to overcome its wider breakeven. For moderate volatility events (5-10% expected moves), the straddle is better because its tighter breakeven is more likely to be reached.

Disclaimer

This is educational content, not financial advice. Trading involves risk, and you should consult a qualified financial advisor before making any investment decisions. Past performance does not guarantee future results.

Related Articles

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.