Iron Butterfly: A Tighter Iron Condor for Range-Bound Markets

⚡ Key Takeaways

- An iron butterfly sells an ATM straddle and buys OTM wings, creating a defined-risk neutral strategy

- Maximum profit occurs when the stock closes exactly at the center strike at expiration

- The strategy collects a large net credit compared to iron condors because the short strikes are at the money

- Maximum loss equals the wing width minus the net credit received

- Iron butterflies work best in low-volatility environments where you expect the stock to stay flat

What Is an Iron Butterfly?

The iron butterfly is a four-leg options strategy that profits when the underlying stock stays near a specific price at expiration. It combines selling an at-the-money straddle (one ATM call and one ATM put at the same strike) with buying out-of-the-money wings (one lower put and one higher call) for protection.

Think of it as a tighter, more aggressive version of an iron condor. Where an iron condor uses two different short strikes to create a wide profit zone, the iron butterfly uses a single center strike. This concentrates maximum profit at one exact price point but collects significantly more premium.

The trade structure looks like this:

- Buy 1 OTM put (lower wing)

- Sell 1 ATM put (center strike)

- Sell 1 ATM call (center strike)

- Buy 1 OTM call (upper wing)

All four legs share the same expiration date. The distance between the center strike and each wing is equal, creating a symmetrical position.

Constructing the Trade

Let us build an iron butterfly on SPY trading at $500. You choose the $500 center strike with $10-wide wings:

| Leg | Strike | Action | Premium |

|---|---|---|---|

| Long put (lower wing) | $490 | Buy 1 | $2.50 |

| Short put (center) | $500 | Sell 1 | $6.00 |

| Short call (center) | $500 | Sell 1 | $6.00 |

| Long call (upper wing) | $510 | Buy 1 | $2.50 |

Net Credit = (Short Put + Short Call) − (Long Put + Long Call)Net Credit = ($6.00 + $6.00) − ($2.50 + $2.50) = $7.00 per share ($700 per contract)

This $700 credit is yours to keep if SPY closes exactly at $500 at expiration. The wings cost $500 total but are there purely for protection — without them, you would have an unlimited-risk short straddle.

Profit, Loss, and Breakeven

The risk-reward math on iron butterflies is straightforward once you know the structure.

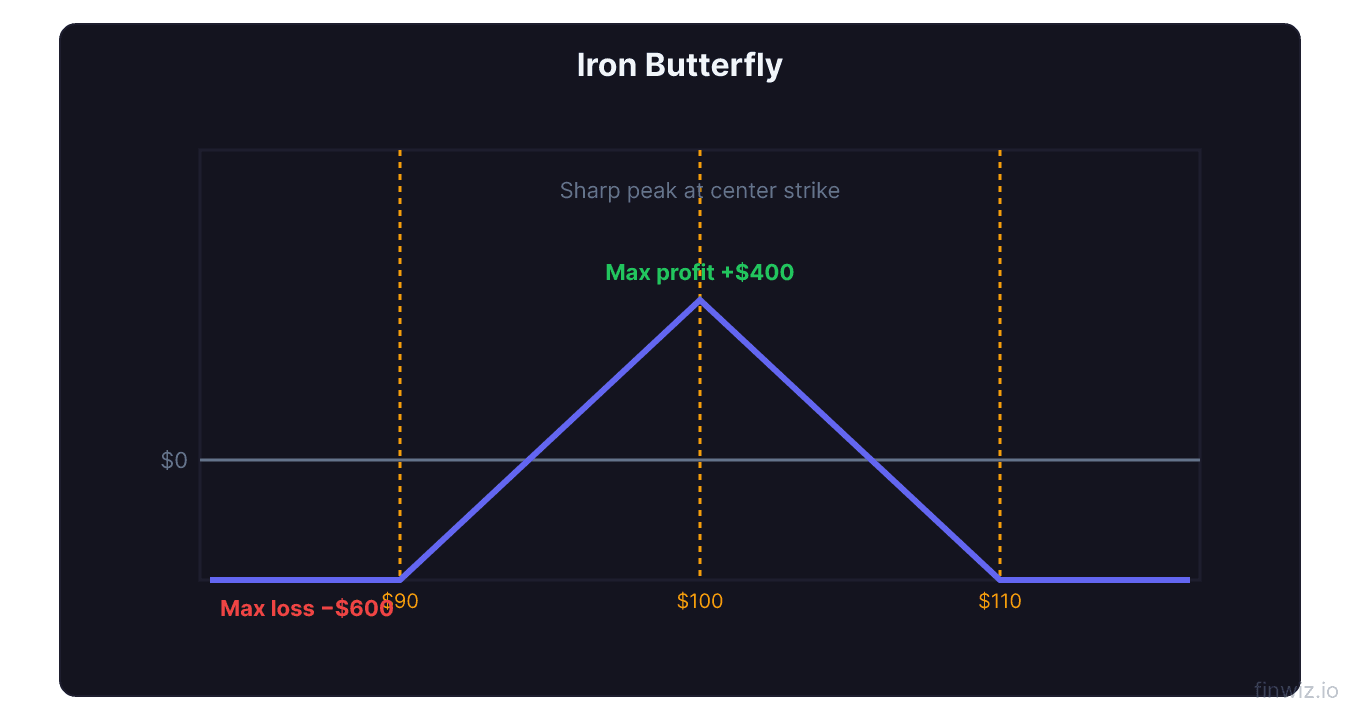

Maximum profit equals the net credit received. This occurs only if the stock closes exactly at the center strike. In practice, any close within a dollar or two of center still yields a substantial profit.

Maximum loss equals the wing width minus the net credit. Using our example: $10.00 − $7.00 = $3.00 per share ($300 per contract). This loss occurs if SPY moves beyond either wing at expiration.

Max Loss = Wing Width − Net Credit ReceivedBreakeven points are the center strike plus and minus the net credit:

Upper Breakeven = Center Strike + Net Credit = $500 + $7.00 = $507Lower Breakeven = Center Strike − Net Credit = $500 − $7.00 = $493The profit zone spans $493 to $507 — a $14 range. SPY needs to stay within 1.4% of the center strike for the trade to be profitable. The risk-to-reward ratio is attractive: risking $300 to make up to $700 is a 2.3:1 reward-to-risk.

Iron Butterfly vs. Iron Condor

Both strategies profit from range-bound stocks, but they differ in important ways:

| Feature | Iron Butterfly | Iron Condor |

|---|---|---|

| Short strikes | Same (ATM) | Different (OTM) |

| Credit collected | Larger | Smaller |

| Profit zone width | Narrower | Wider |

| Max profit probability | Lower | Higher |

| Max profit amount | Higher | Lower |

| Best for | Precise price targets | Wider range expectations |

Choose the iron butterfly when you have high conviction the stock will stay near a specific price — such as after earnings when the stock has already reacted and implied volatility has collapsed. Choose the iron condor when you want a wider margin of error.

The butterfly spread using only calls or only puts achieves a similar payoff but is entered as a debit trade rather than a credit trade. The iron butterfly's credit structure means time decay works in your favor from the moment you enter.

Pro Tip

When to Use an Iron Butterfly

Iron butterflies thrive in specific market conditions:

Post-earnings. After a company reports earnings and the stock settles into a new range, implied volatility drops sharply. The stock often trades sideways for days or weeks. An iron butterfly centered at the post-earnings price capitalizes on this consolidation.

Low-volatility environments. When VIX is low and stocks are grinding sideways, iron butterflies collect premium from the remaining extrinsic value that time decay will erode.

Before weekends or holidays. Theta decay continues on non-trading days. Entering an iron butterfly on Thursday afternoon captures weekend decay without market movement risk (though gap risk remains at Monday's open).

Avoid iron butterflies before known catalysts (earnings, FDA decisions, Fed announcements) because large moves will push the stock beyond your profit zone. Also avoid them in trending markets where directional momentum makes a center-pin unlikely.

Managing the Position

Active management separates profitable iron butterfly traders from those who let theta decay do all the work and give it back on a single move.

Close at 50% of max profit. If you collected $7.00 in credit, close the position when you can buy it back for $3.50. This captures $350 in profit while removing the risk of a late move against you. Studies on SPY options show that closing at 50% significantly improves risk-adjusted returns.

Adjust if the stock moves. If the stock trends away from center, you can roll the untested wing closer to collect additional credit and reduce your breakeven range. For example, if SPY moves to $505, roll the $490 put up to $495 for a small credit.

Watch the Greeks. Monitor delta to gauge directional risk and gamma to understand how quickly your position changes. As expiration approaches, gamma increases sharply for ATM options, meaning small stock moves create large P&L swings. For a deeper dive, see options Greeks.

Have a max loss exit. If the stock moves beyond one of your wings before expiration, consider closing to avoid max loss. The loss will be less than max if there is time value remaining in the position.

Frequently Asked Questions

How is an iron butterfly different from a regular butterfly?

A regular butterfly spread uses either all calls or all puts and is entered for a net debit. An iron butterfly uses both calls and puts and is entered for a net credit. The payoff profile at expiration is nearly identical — both achieve max profit at the center strike with defined risk. The iron butterfly is often preferred because the credit structure means you receive cash upfront.

What is the ideal time to expiration for an iron butterfly?

The sweet spot is 21 to 45 days to expiration. This gives enough time to collect meaningful premium while being close enough for theta to accelerate. Shorter durations (under 14 DTE) have higher gamma risk and less room for error. Longer durations tie up capital without proportional premium benefit.

Can I lose more than the width of the wings minus the credit?

No. The maximum loss is strictly defined as the wing width minus the net credit, multiplied by 100. Using our example, the maximum loss per contract is $300. This is true regardless of how far the stock moves beyond the wings. The long wing options cap your loss on both sides. This is why the iron butterfly is classified as a defined-risk strategy, distinguishing it from a naked straddle or strangle.

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.