Credit Spreads: Collecting Premium with Defined Risk

⚡ Key Takeaways

- Credit spreads collect premium upfront by selling a closer-to-the-money option and buying a further out-of-the-money option for protection

- Bull put spreads profit when the stock stays above the short put strike; bear call spreads profit when the stock stays below the short call strike

- Maximum loss is defined and equals the width of the strikes minus the credit received

- Credit spreads benefit from time decay (theta) working in your favor as a net seller

- Probability of profit is typically 60-75% depending on how far out-of-the-money you place the short strike

What Are Credit Spreads?

A credit spread is an options strategy where you simultaneously sell one option and buy another option of the same type (both calls or both puts) at different strike prices but the same expiration. The option you sell is closer to the current stock price and therefore more expensive, while the option you buy is further away and cheaper. The difference in premiums results in a net credit deposited into your account.

Credit spreads are one of the most popular strategies among options traders because they offer defined risk, consistent income potential, and the statistical advantage of theta decay working in your favor. Unlike selling naked options, the purchased option limits your maximum loss to a known amount.

There are two primary types of credit spreads: the bull put spread (bullish) and the bear call spread (bearish). Each has its own optimal market conditions, risk profile, and management techniques.

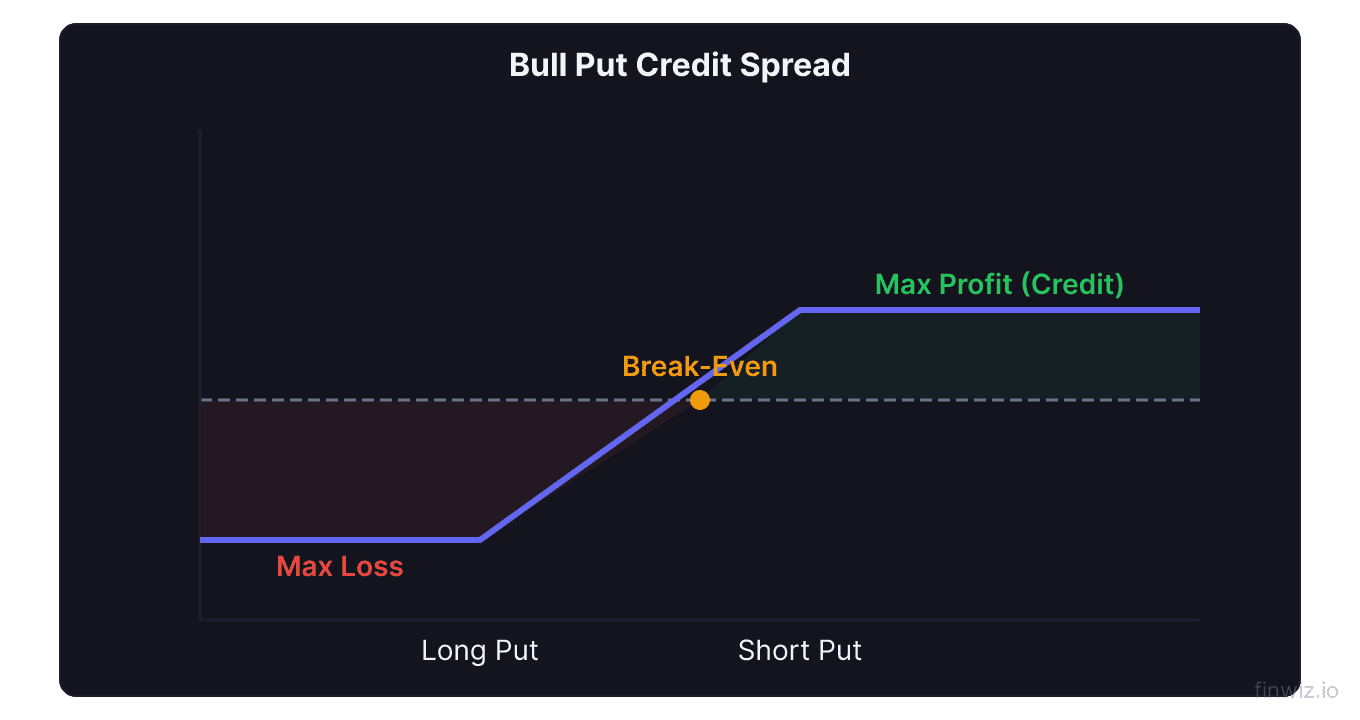

The Bull Put Spread Explained

A bull put spread is a bullish credit spread constructed using put options. You profit when the stock stays above a certain price through expiration.

Construction:

- Sell 1 put at a higher strike (closer to current price)

- Buy 1 put at a lower strike (further from current price)

- Both puts share the same expiration date

For example, with stock XYZ trading at $105:

| Leg | Strike | Action | Premium |

|---|---|---|---|

| Short put | $100 | Sell | $2.50 |

| Long put | $95 | Buy | $1.00 |

| Net credit | $1.50 |

Net Credit = Short Put Premium - Long Put Premium = $2.50 - $1.00 = $1.50You receive $1.50 per share ($150 per contract) immediately. Your maximum profit is this $150 if both puts expire worthless, which happens when the stock is above $100 at expiration.

Max Loss = Strike Width - Net Credit = ($100 - $95) - $1.50 = $3.50 per share ($350 per contract)Breakeven = Short Strike - Net Credit = $100 - $1.50 = $98.50The stock can drop from $105 to $98.50 before you start losing money. That is a $6.50 cushion or roughly 6.2% below the current price. This margin of safety is a key advantage of credit spreads.

The Bear Call Spread Explained

A bear call spread is a bearish credit spread constructed using call options. You profit when the stock stays below a certain price through expiration.

Construction:

- Sell 1 call at a lower strike (closer to current price)

- Buy 1 call at a higher strike (further from current price)

- Both calls share the same expiration date

For example, with stock XYZ trading at $95:

| Leg | Strike | Action | Premium |

|---|---|---|---|

| Short call | $100 | Sell | $2.00 |

| Long call | $105 | Buy | $0.75 |

| Net credit | $1.25 |

You collect $1.25 per share ($125 per contract). The stock must stay below $100 for maximum profit. Your maximum loss is $3.75 per share ($375 per contract), which occurs if the stock closes above $105 at expiration.

Breakeven = Short Strike + Net Credit = $100 + $1.25 = $101.25Bear call spreads are commonly used when you expect a stock to stay flat or decline. They are also popular for selling into elevated implied volatility after a stock has had a sharp run-up.

How Theta Decay Benefits Credit Spreads

One of the most compelling reasons to trade credit spreads is that time is on your side. As a net option seller, you benefit from the daily erosion of time value, known as theta decay.

Every day that passes, your short option loses value faster than your long option. This is because the short option is closer to the money and has more extrinsic value (time value) to decay. As the spread loses value, you can buy it back for less than you sold it for, capturing a profit.

Spread Value at Expiration (stock above short put for bull put spread) = $0.00. Your profit = Full credit received.Theta decay accelerates in the final 30-45 days before expiration, which is why most credit spread traders enter positions with 30-45 days to expiration (DTE). This sweet spot balances premium collection with the acceleration of time decay.

Pro Tip

Choosing Strike Prices and Width

The strike prices you choose for a credit spread determine your probability of profit, premium collected, and maximum risk. These factors involve trade-offs that you must balance.

Short strike selection is the most important decision. The further out-of-the-money your short strike, the higher your probability of profit but the lower your premium collected. Many traders use delta as a guide:

| Short Strike Delta | Approx. Probability of Profit | Premium Level |

|---|---|---|

| 0.30 delta | ~70% | Moderate |

| 0.20 delta | ~80% | Lower |

| 0.15 delta | ~85% | Low |

| 0.10 delta | ~90% | Very low |

Spread width (the distance between strikes) determines your maximum loss and affects the risk-to-reward ratio. Wider spreads collect more credit but have higher maximum loss. Narrower spreads have less risk but collect less premium.

| Spread Width | Credit Example | Max Loss | Risk:Reward |

|---|---|---|---|

| $1 wide | $0.30 | $0.70 | 2.3:1 |

| $2 wide | $0.55 | $1.45 | 2.6:1 |

| $5 wide | $1.25 | $3.75 | 3:1 |

| $10 wide | $2.20 | $7.80 | 3.5:1 |

Notice that wider spreads have a worse risk-to-reward ratio. However, they collect more absolute premium, and many traders prefer them for capital efficiency since the margin requirement is based on spread width.

Managing Credit Spreads

Active management of credit spreads separates consistent traders from those who rely purely on probability. Here are the key management rules.

Close at 50% of max profit. When the spread has lost half its value, buy it back. If you sold a spread for $1.50 and it is now worth $0.75, close it. This captures 50% of the profit while eliminating the risk of a reversal. Your capital is then free for a new trade.

Close at 21 DTE. If the trade is still open with 21 days left and has not reached 50% profit, evaluate whether to close or continue holding. Gamma risk increases as expiration approaches, making the position more volatile.

Cut losses at 2x credit received. If you sold a spread for $1.50 and it has expanded to $3.00 (your loss equals the credit received), close the position. This prevents a small loss from becoming a maximum loss.

Roll the position if you still believe in the thesis but the trade has moved against you. Rolling means closing the current spread and opening a new one at a later expiration, possibly at different strikes. Rolling out in time collects additional credit and gives the trade more time to work.

Net Credit After Roll = Original Credit + New Credit Received from Roll - Cost to Close Original SpreadCredit Spreads vs Other Income Strategies

Credit spreads are one of several options selling strategies. Here is how they compare:

| Strategy | Risk | Capital Required | Complexity | Theta Benefit |

|---|---|---|---|---|

| Credit spread | Defined | Low-moderate | Low | Moderate |

| Naked put | Substantial | High (margin) | Low | High |

| Iron condor | Defined | Low-moderate | Moderate | High |

| Covered call | Stock risk | High (own shares) | Low | Moderate |

| Calendar spread | Defined | Moderate | Moderate | Moderate |

Credit spreads offer the best balance of simplicity, defined risk, and capital efficiency among income strategies. They require less capital than naked puts or covered calls, and they are simpler than iron condors or calendars.

Position Sizing for Credit Spreads

Proper position sizing is critical when trading credit spreads because even high-probability trades will lose sometimes. A string of losses should not damage your account.

The general rule is to risk no more than 2-5% of your total account on any single credit spread trade. Since the maximum loss equals the spread width minus the credit received, size your position accordingly.

Number of Contracts = (Account Size x Max Risk %) / Max Loss Per ContractFor example, with a $50,000 account risking 3% per trade on a spread with $350 max loss:

Contracts = ($50,000 x 0.03) / $350 = 4.3, round down to 4 contractsDiversify across underlyings to avoid concentration risk. Even if you trade credit spreads exclusively, spread your positions across different stocks, sectors, and market conditions. A single event (like an earnings miss) can cause maximum loss on a position, so having 5-10 different spreads reduces the impact of any single loss.

Pro Tip

Common Credit Spread Mistakes

Avoid these frequent errors that undermine credit spread profitability.

Selling spreads before earnings. The implied volatility is high for a reason. A post-earnings gap can easily blow through your short strike. Either trade credit spreads after earnings or leave a wide buffer.

Ignoring implied volatility rank. Credit spreads work best when IV rank is elevated (above 30-50%). Selling options when IV is low means you collect less premium and have less of a cushion if things go wrong. Check IV percentile before entering.

Choosing illiquid options. Poor liquidity means wide bid-ask spreads, which reduce your edge. Stick to underlyings with high options volume and open interest. Major stocks and ETFs are ideal.

Not having an exit plan. Decide your profit target and loss limit before entering the trade. Without predefined rules, emotions take over and lead to holding losers too long or closing winners too early.

Over-concentrating in one direction. If all your bull put spreads are on tech stocks, a sector downturn hits everything at once. Diversify across sectors and balance bullish and bearish positions when possible.

Frequently Asked Questions

What is a good return on a credit spread?

Most credit spread traders target a return of 10-25% of the capital at risk per trade, collected over 30-45 days. On an annualized basis, consistently profitable credit spread traders often achieve 20-40% annual returns, though this varies significantly based on market conditions and risk management.

Can I get assigned on a credit spread?

Yes, early assignment is possible on the short leg of your spread, particularly on short puts when the stock drops below the strike or short calls near ex-dividend dates. If assigned, you can exercise your long option to close the position. The net result should not exceed your maximum defined loss, but assignment can temporarily require additional capital.

Should I trade bull put spreads or bear call spreads?

Statistically, bull put spreads tend to perform better over time because the stock market has a long-term upward bias. However, bear call spreads are valuable during overbought conditions, elevated IV, or when you have a bearish thesis on a specific stock. Many traders use both depending on market conditions.

How many credit spreads should I have open at once?

This depends on your account size and risk tolerance. Most experienced traders carry 5-15 open credit spread positions at a time, diversified across different stocks and sectors. The key is ensuring your total risk from all positions does not exceed 20-30% of your account.

What happens if a credit spread expires in between the two strikes?

If the stock closes between your strikes at expiration, the short option is in-the-money and the long option is out-of-the-money. Your short option will likely be assigned, and you will not be able to exercise your long option for full offset. This results in a loss between zero and the maximum loss. To avoid this scenario, close the spread before expiration day.

Disclaimer

This is educational content, not financial advice. Trading involves risk, and you should consult a qualified financial advisor before making any investment decisions. Past performance does not guarantee future results.

Related Articles

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.