Debit Spreads: Directional Bets with Limited Risk

⚡ Key Takeaways

- Debit spreads are directional options strategies where you pay a net premium to enter the trade

- Bull call spreads profit from upward moves; bear put spreads profit from downward moves

- Maximum profit is capped at the difference between strikes minus the debit paid

- Debit spreads cost less than buying options outright, reducing your breakeven price

- These spreads define both maximum profit and maximum loss from the moment you enter

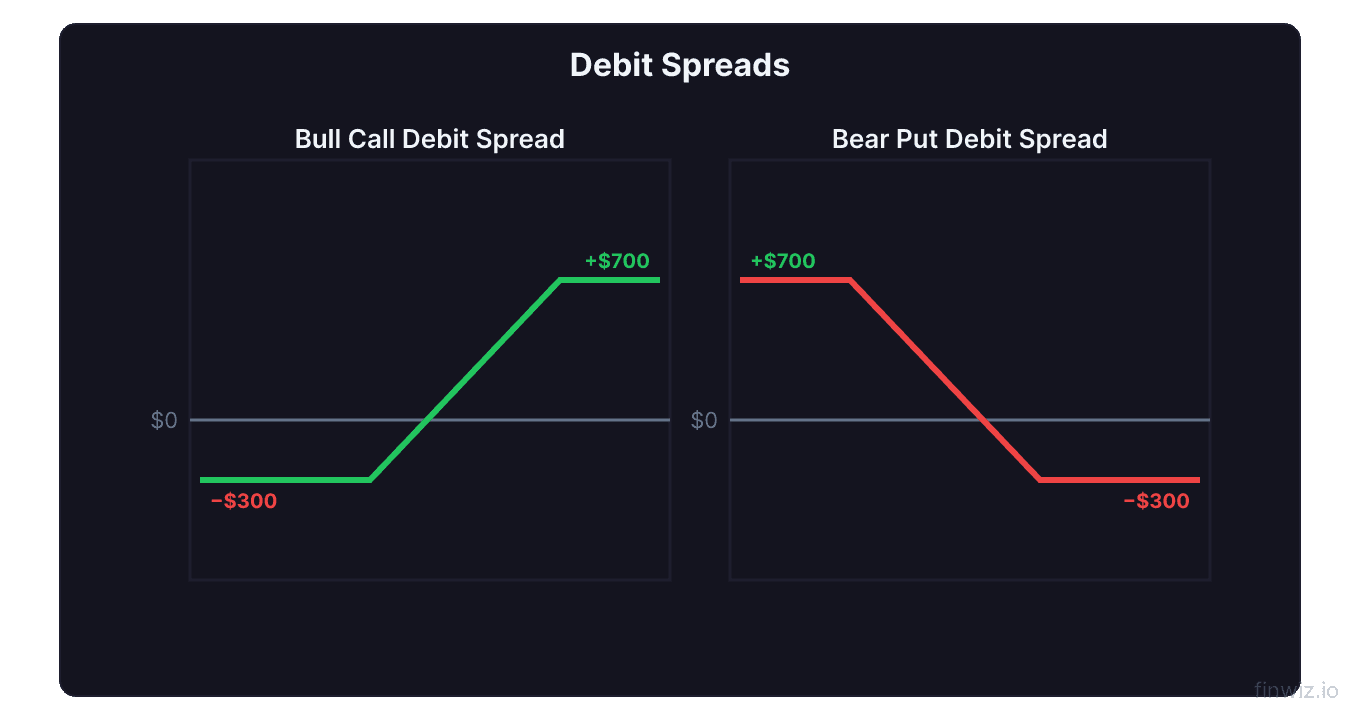

What Are Debit Spreads?

A debit spread is an options strategy where you buy one option and sell another option of the same type at a different strike price, both with the same expiration. The option you buy costs more than the one you sell, so you pay a net debit to enter the position.

Debit spreads are directional strategies. You use a bull call spread when you expect the stock to go up and a bear put spread when you expect it to go down. Unlike credit spreads where you collect premium and hope the options expire worthless, debit spreads require the stock to move in your anticipated direction.

The key advantage of a debit spread over buying a single option is reduced cost. By selling a further out-of-the-money option, you offset part of the premium of the option you purchase. This lowers your breakeven point and increases your probability of profit compared to an outright long option.

The trade-off is that your profit is capped at the width of the strikes minus the debit paid. You sacrifice unlimited upside for a lower cost of entry and a better risk-to-reward profile.

How to Build a Bull Call Spread

The bull call spread is the most common debit spread. It profits when the underlying stock rises above your breakeven point before expiration.

Construction:

- Buy 1 call at a lower strike (usually at-the-money or slightly ITM)

- Sell 1 call at a higher strike (out-of-the-money)

- Same expiration date for both

For example, with stock XYZ trading at $100:

| Leg | Strike | Action | Premium |

|---|---|---|---|

| Long call | $100 | Buy | $4.00 |

| Short call | $105 | Sell | $1.50 |

| Net debit | $2.50 |

Net Debit = Long Call Premium - Short Call Premium = $4.00 - $1.50 = $2.50 per share ($250 per contract)Your maximum risk is the $250 net debit. This is lost if the stock is at or below $100 at expiration.

Max Profit = Strike Width - Net Debit = ($105 - $100) - $2.50 = $2.50 per share ($250 per contract)Breakeven = Long Strike + Net Debit = $100 + $2.50 = $102.50The stock needs to reach $102.50 for you to break even, and you make maximum profit at $105 or above. This is a 1:1 risk-to-reward ratio in this example.

Try It: Debit Spread Calculator

How to Build a Bear Put Spread

The bear put spread is the bearish counterpart. It profits when the stock declines below your breakeven point.

Construction:

- Buy 1 put at a higher strike (at-the-money or slightly ITM)

- Sell 1 put at a lower strike (out-of-the-money)

- Same expiration date

For example, with stock XYZ trading at $100:

| Leg | Strike | Action | Premium |

|---|---|---|---|

| Long put | $100 | Buy | $3.50 |

| Short put | $95 | Sell | $1.25 |

| Net debit | $2.25 |

Max Profit = Strike Width - Net Debit = ($100 - $95) - $2.25 = $2.75 per share ($275 per contract)Breakeven = Long Strike - Net Debit = $100 - $2.25 = $97.75The stock needs to drop to $97.75 for you to break even, with maximum profit at $95 or below. This trade risks $225 to make $275, a 1.2:1 reward-to-risk ratio.

Debit Spreads vs Buying Options Outright

One of the most common questions from options beginners is why you would cap your profit by using a spread instead of simply buying a call or put. The comparison reveals important trade-offs.

| Factor | Long Call | Bull Call Spread |

|---|---|---|

| Cost | $4.00 ($400) | $2.50 ($250) |

| Breakeven | $104.00 | $102.50 |

| Max loss | $400 | $250 |

| Max profit | Unlimited | $250 |

| Prob. of profit | Lower | Higher |

| Theta impact | Negative | Partially offset |

The spread is cheaper, has a lower breakeven, and has a higher probability of profit. The only advantage of the long call is its unlimited upside. But statistically, stocks rarely make massive moves in a short time frame. For a move to $105 in this example, the spread and the outright call produce similar dollar returns, but the spread cost 37% less.

Pro Tip

Selecting Strikes and Expiration

Getting the right strike prices and expiration is critical for debit spread success.

Long strike selection. For bull call spreads, the long call is typically at-the-money or slightly in-the-money. ATM strikes have the highest gamma and benefit most from quick moves. Slightly ITM strikes have higher delta and a higher probability of profit but cost more.

Short strike selection. Place the short strike at or near your price target. There is no benefit in setting it beyond where you think the stock will go, as it just widens the spread and increases your debit without improving expected returns.

Spread width guidelines:

| Spread Width | Typical Debit | Risk Profile |

|---|---|---|

| $1 wide | 40-60% of width | Low risk, low reward |

| $2.50 wide | 40-55% of width | Moderate |

| $5 wide | 35-50% of width | Moderate-high |

| $10 wide | 30-45% of width | Higher dollar risk/reward |

Expiration selection. Choose an expiration that gives the stock enough time to reach your target. As a rule of thumb, select an expiration that is 1.5 to 2 times the period you think the move will take. If you expect the move in 2 weeks, use a 3-4 week expiration. This provides a buffer for timing errors.

Avoid very short expirations (less than 7 days) unless you are making a specific event-driven trade. Theta decay accelerates in the final week and can erode your long option's value rapidly.

How Greeks Affect Debit Spreads

Understanding how the options Greeks impact your debit spread helps you manage the position effectively.

Delta tells you how much the spread's value changes per $1 move in the stock. A bull call spread's net delta is positive, meaning it gains value as the stock rises. The net delta is the difference between the long and short option deltas.

Theta is partially offset in a debit spread. Your long option loses value each day, but your short option also loses value, and since you are short that option, its decay works in your favor. The net theta is still negative (you lose money each day from time decay), but the loss is smaller than holding the long option alone.

Vega is the spread's sensitivity to changes in implied volatility. A debit spread has positive net vega when opened, meaning it benefits from rising IV and is hurt by falling IV. However, the vega exposure is smaller than a single long option because the short leg partially offsets it.

Gamma increases as the stock approaches the long strike and decreases as it approaches the short strike. High gamma near expiration means the spread's delta can change rapidly, making the position more volatile.

Managing Debit Spreads

Effective management of debit spreads involves knowing when to take profits, cut losses, and adjust positions.

Take profits at 50-75% of max profit. If your $250 max profit spread is worth $375-$437 (you paid $250), consider closing. Waiting for full max profit requires the stock to be at or above the short strike at expiration, which adds unnecessary risk.

Cut losses early. If the stock moves against you and the spread loses 50% of its value (from $250 to $125), evaluate whether your thesis still holds. If not, close the trade and preserve capital.

Roll the position if you still believe in the direction but need more time. Close the current spread and open a new one at a later expiration. You can also adjust strikes if the price has moved.

Close before the last week. Unless the spread is fully in-the-money, the final week brings high gamma risk that can turn a winning trade into a loser quickly. Taking profits early avoids this.

| Scenario | Action | Reasoning |

|---|---|---|

| 50-75% of max profit reached | Close | Lock in gains, redeploy capital |

| Stock at short strike with weeks left | Hold or close | Already near max profit |

| Spread lost 50% of value | Evaluate and likely close | Preserve capital |

| 5 DTE with partial profit | Close | Avoid gamma risk |

| Stock gapped through both strikes | Close for near-max profit | No additional upside |

When to Use Debit Spreads vs Credit Spreads

Both debit spreads and credit spreads are vertical spreads, but they suit different situations.

Use debit spreads when:

- You have a specific directional thesis with a price target

- Implied volatility is low to moderate (options are cheap to buy)

- You want the stock to move significantly in one direction

- You prefer to pay upfront and wait for a move

Use credit spreads when:

- You want the stock to stay in a range or move slightly in one direction

- Implied volatility is elevated (options are expensive, good to sell)

- You prefer theta decay working in your favor

- You want income-style consistent smaller wins

The best traders use both strategies, selecting whichever fits the current market environment and their thesis for the specific underlying.

Pro Tip

Frequently Asked Questions

What is the ideal risk-to-reward ratio for a debit spread?

Aim for a net debit that is 30-50% of the spread width. This gives you a reward-to-risk ratio of 1:1 to 2.3:1. For example, on a $5-wide spread, paying $1.50-$2.50 is reasonable. Paying more than 60% of the width means you need the stock to move almost all the way to the short strike just to break even.

Should I exercise my debit spread at expiration?

Almost never. Sell the spread before expiration rather than exercising. Exercising forfeits any remaining time value in the long option and requires capital to buy the shares. Selling the spread captures the full value including time premium and avoids assignment complications.

Can I lose more than my initial debit?

No. The maximum loss on a debit spread is the net debit paid. If you paid $250 to enter the trade, $250 is the most you can lose. There is no margin risk and no possibility of a loss exceeding your initial investment.

How do debit spreads handle earnings announcements?

Debit spreads can work for earnings plays because the short leg reduces the impact of IV crush. When IV drops after earnings, both legs lose extrinsic value, partially offsetting each other. However, you still need the stock to move in your direction to profit, so the earnings announcement must produce the expected move.

Can I turn a long call into a debit spread after entry?

Yes. If you bought a long call and it has appreciated, you can sell a higher-strike call against it to create a bull call spread. This is called legging into a spread. It locks in some profit and reduces risk, though it also caps your upside from that point forward.

Disclaimer

This is educational content, not financial advice. Trading involves risk, and you should consult a qualified financial advisor before making any investment decisions. Past performance does not guarantee future results.

Related Articles

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.