Ratio Spreads & Backspreads: Asymmetric Options Strategies

⚡ Key Takeaways

- A ratio spread buys fewer options at one strike and sells more at another, creating an unbalanced position

- Call ratio spreads profit from moderate upside moves while generating risk beyond the short strikes

- Backspreads reverse the ratio — buying more options than you sell — to profit from large volatility moves

- Ratio spreads can be entered for zero cost or a net credit, but carry undefined risk on one side

- These are advanced strategies that require active management and clear exit rules

What Is a Ratio Spread?

A ratio spread is an options strategy where you buy and sell different quantities of options at different strike prices with the same expiration. The most common configuration is a 1:2 ratio — buy one option at one strike, sell two options at another strike.

Unlike a standard bull call spread or bear put spread where you buy and sell equal quantities, the unequal ratio creates a unique risk profile. You get the benefits of a spread at one price range, but you also have a naked short option that creates risk beyond a certain point.

Ratio spreads are not beginner strategies. They require understanding of the Greeks, comfort with undefined risk on one side, and the discipline to manage or close positions before they move against you. However, for intermediate and advanced traders, they offer flexibility that balanced spreads cannot match.

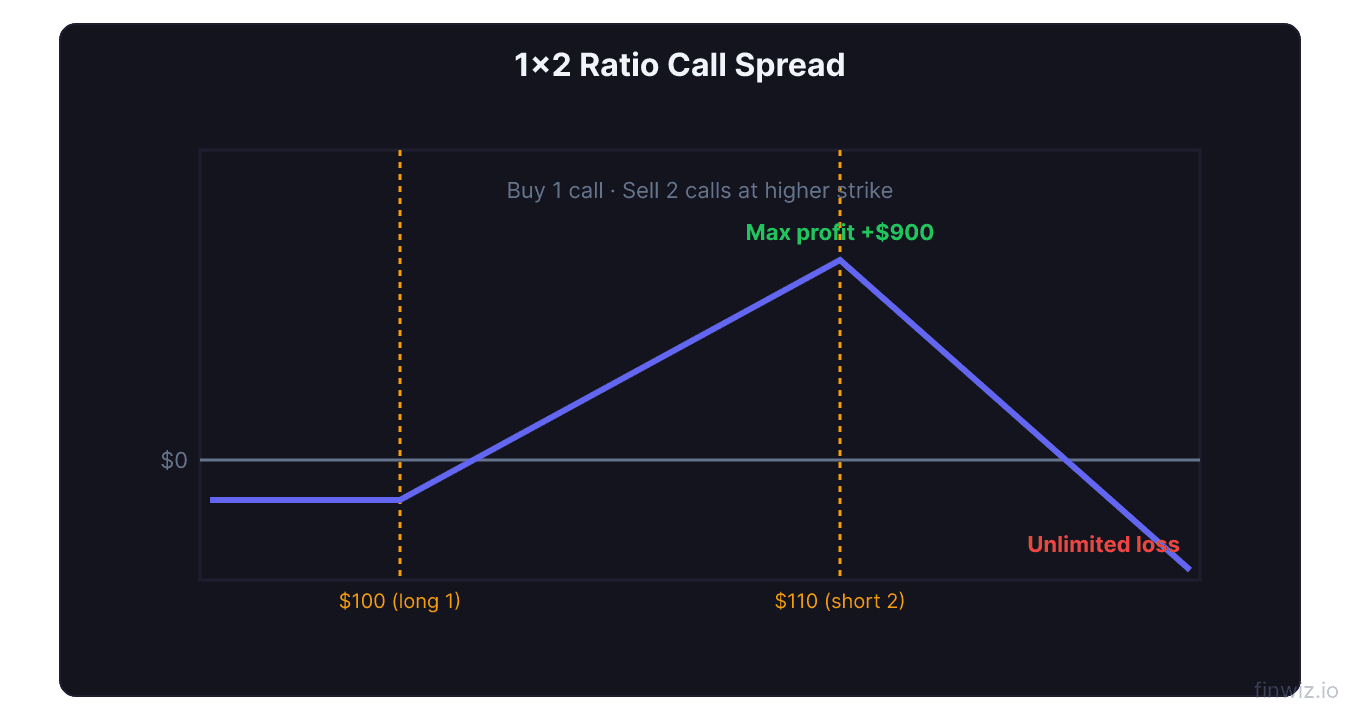

Call Ratio Spread: Structure and Example

A call ratio spread (also called a ratio call write or ratio vertical) involves buying calls at a lower strike and selling more calls at a higher strike. The standard 1:2 ratio means buying 1 lower-strike call and selling 2 higher-strike calls.

Example on AMZN trading at $185:

| Leg | Strike | Action | Premium |

|---|---|---|---|

| Long call | $185 | Buy 1 | $7.00 |

| Short calls | $195 | Sell 2 | $3.00 each ($6.00 total) |

| Net cost | $1.00 ($100 per position) |

This position profits if AMZN stays near $185 (you only lose the $1.00 net debit) or rises moderately to $195 (the long call gains value while the short calls expire worthless or near worthless).

Maximum profit occurs at the short strike at expiration:

Max Profit = (Short Strike − Long Strike − Net Debit) × 100Max Profit = ($195 − $185 − $1.00) × 100 = $900

Breakeven points:

Lower Breakeven = Long Strike + Net Debit = $185 + $1.00 = $186Upper Breakeven = Short Strike + Max Profit = $195 + $9.00 = $204Between $186 and $204, the trade is profitable. Below $186, you lose the $100 net debit. Above $204, losses increase dollar-for-dollar because you have one naked short call.

The risk above $204 is theoretically unlimited — this is the key danger of ratio spreads. If AMZN surges to $220, your loss is ($220 − $204) × 100 = $1,600 and growing.

Put Ratio Spread

A put ratio spread is the bearish equivalent. You buy puts at a higher strike and sell more puts at a lower strike, profiting from a moderate decline.

Example on NFLX trading at $700:

- Buy 1 NFLX $700 put at $15.00

- Sell 2 NFLX $680 puts at $8.00 each ($16.00 total)

- Net credit: $1.00 ($100)

Maximum profit occurs if NFLX drops to exactly $680 at expiration. The risk is to the downside — if NFLX crashes well below $660 (the lower breakeven), losses accelerate because of the naked short put.

Put Ratio Max Profit = (Long Strike − Short Strike + Net Credit) × 100Max Profit = ($700 − $680 + $1.00) × 100 = $2,100

The net credit entry means you do not lose money if NFLX stays flat or rises — the position simply expires worthless with the $100 credit in your pocket. This is an advantage over a standard bear put spread, which requires a move lower just to break even.

Pro Tip

Backspreads: Reversing the Ratio

A backspread flips the ratio — you sell fewer options at one strike and buy more at another. The standard configuration sells 1 and buys 2, creating a position that profits from large moves.

Call backspread (1:2):

- Sell 1 lower-strike call

- Buy 2 higher-strike calls

This trade profits from a large upward move. The two long calls outpace the single short call as the stock surges. It also has limited risk to the downside (you keep the net credit if entered for a credit, or lose the net debit).

Example on TSLA trading at $250:

| Leg | Strike | Action | Premium |

|---|---|---|---|

| Short call | $250 | Sell 1 | $12.00 |

| Long calls | $265 | Buy 2 | $6.00 each ($12.00 total) |

| Net cost | $0.00 (even) |

If TSLA stays at $250, both the short and long calls expire worthless — no gain, no loss. If TSLA drops, same result. If TSLA rallies to $300, the short call loses $50.00 but the two long calls gain $35.00 each ($70.00 total). Net profit: $20.00 per share, or $2,000.

The danger zone for backspreads is a moderate move toward the long strikes. If TSLA rises to exactly $265, the short call is worth $15.00 (loss), each long call is worth $0.00. Net loss: $15.00 per share ($1,500). This maximum loss occurs at the long strike price at expiration.

Backspread Max Loss = (Long Strike − Short Strike − Net Credit) × (Contracts Sold × 100)Put Backspreads for Crash Protection

Put backspreads sell one higher-strike put and buy two lower-strike puts. They profit from large downside moves and are used as portfolio crash protection.

This strategy shines during black swan events when stocks gap down sharply. The two long puts accelerate in value while the single short put limits your cost. If entered for a credit, you have zero risk if the stock stays flat or rises.

Put backspreads are a more capital-efficient alternative to buying outright protective puts. The sold put subsidizes the cost of two long puts, letting you own more downside protection per dollar spent.

Greek Profile and Management

Understanding the Greeks of ratio spreads and backspreads is essential for management. Reviewing options Greeks before trading these strategies is strongly recommended.

Ratio spreads:

- Near zero delta at entry (market neutral)

- Positive theta (time decay helps, similar to credit spreads)

- Negative gamma (large moves hurt)

- Short vega (benefits from falling implied volatility)

Backspreads:

- Near zero delta at entry

- Negative theta (time decay hurts)

- Positive gamma (large moves help)

- Long vega (benefits from rising implied volatility)

This means ratio spreads behave like income trades in calm markets but become dangerous in volatile ones. Backspreads lose money in calm markets but explode in value during sharp moves.

Management rules:

- Close ratio spreads if the stock approaches the upper breakeven (call ratios) or lower breakeven (put ratios)

- Close backspreads at 21 DTE if the large move has not occurred — theta acceleration will erode value

- Monitor delta daily; if delta exceeds ±50 per contract, the position is becoming directional and needs adjustment

For a comprehensive framework on managing these positions, see options risk management.

When to Use Each Strategy

| Strategy | Market Outlook | Volatility View | Best Scenario |

|---|---|---|---|

| Call ratio spread | Moderately bullish | Expect IV to fall | Stock rises to short strike |

| Put ratio spread | Moderately bearish | Expect IV to fall | Stock drops to short strike |

| Call backspread | Strongly bullish or neutral | Expect IV to rise | Stock surges or stays flat |

| Put backspread | Strongly bearish or neutral | Expect IV to rise | Stock crashes or stays flat |

Ratio spreads work best in the 30-45 DTE window where theta decay is meaningful. Backspreads work best with 45-60 DTE to give the stock time for a large move before theta erodes the position.

Frequently Asked Questions

Are ratio spreads suitable for beginners?

No. Ratio spreads involve undefined risk on one side and require understanding of multi-leg option pricing, Greeks management, and active position monitoring. Start with defined-risk strategies like vertical spreads and iron condors. Once you are consistently profitable with those and understand how the Greeks interact, ratio spreads and backspreads become viable additions to your toolkit.

Can I adjust a ratio spread to remove the naked risk?

Yes. You can convert a ratio spread into a butterfly by buying an additional out-of-the-money option to cap the open-ended risk. For example, adding a $210 long call to the 1:2 call ratio spread ($185/$195) creates a broken-wing butterfly with defined risk on both sides. This costs additional premium but eliminates the theoretically unlimited loss.

How do backspreads perform during earnings?

Backspreads can perform well around earnings because they profit from large moves in either direction (depending on call vs. put backspread). However, the IV crush after earnings can hurt backspreads even when the stock makes a large move. The best approach is to enter backspreads before IV expansion (weeks before earnings) rather than the day before when IV is already elevated.

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.