Bull Put Spread: Bullish Credit Spread for Income Traders

⚡ Key Takeaways

- A bull put spread involves selling a higher-strike put and buying a lower-strike put with the same expiration for a net credit

- Maximum profit is the net credit received, earned when the stock stays above the short put strike at expiration

- Maximum loss is the width of the spread minus the credit, which occurs when the stock drops below the long put strike

- The strategy is bullish to neutral, profiting from time decay, falling implied volatility, or upward stock movement

- Bull put spreads are one of the most popular defined-risk income strategies for intermediate options traders

What Is a Bull Put Spread?

A bull put spread (also called a short put vertical or put credit spread) is a two-leg options strategy where you sell a put at a higher strike price and simultaneously buy a put at a lower strike price, both with the same expiration date. You collect a net credit upfront, and that credit is your maximum profit.

The strategy profits when the underlying stock stays above the short put strike at expiration. It is called "bull" because it benefits from bullish or neutral price action, and "put spread" because it uses two put options at different strikes.

Bull put spreads are the bullish counterpart to bear put spreads. They are popular among income-oriented traders who want to profit from time decay with defined risk on both sides of the trade.

How to Construct a Bull Put Spread

A bull put spread has two legs with the same expiration:

- Sell 1 put at the higher strike (closer to or at the money)

- Buy 1 put at the lower strike (further out of the money)

Example: Stock XYZ trades at $100. You are moderately bullish and expect it to stay above $90.

| Leg | Action | Strike | Premium |

|---|---|---|---|

| 1 | Sell put | $95 | +$3.20 |

| 2 | Buy put | $90 | -$1.30 |

| Net | +$1.90 (credit) |

You collect $190 per contract upfront. This is both your income and your maximum profit.

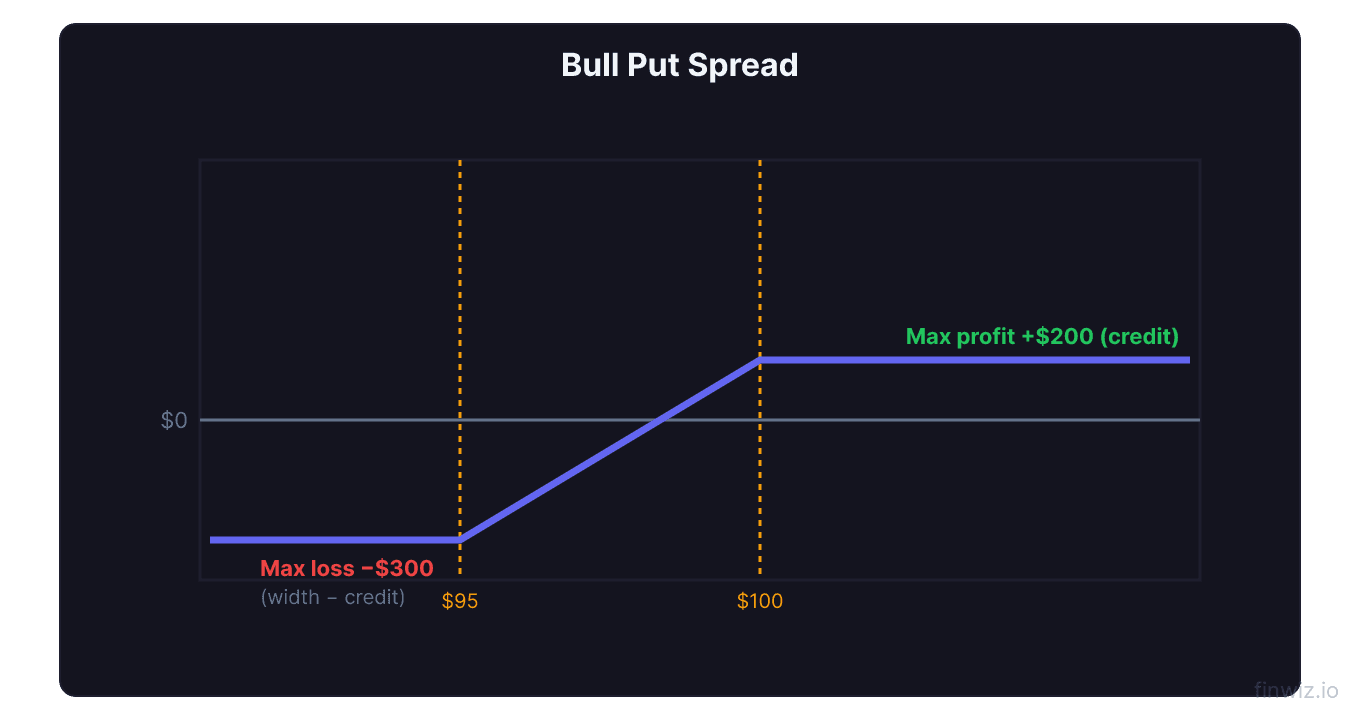

Maximum Profit, Maximum Loss, and Breakeven

Maximum Profit = Net Credit Received × 100Using our example:

| Metric | Calculation | Result |

|---|---|---|

| Max Profit | $1.90 × 100 | $190 |

| Max Loss | ($95 − $90 − $1.90) × 100 | $310 |

| Breakeven | $95 − $1.90 | $93.10 |

| Risk-Reward Ratio | $190 ÷ $310 | 0.61:1 |

The stock needs to stay above $93.10 for you to profit. Maximum profit occurs when the stock is at or above $95 at expiration, and maximum loss occurs at $90 or below.

Payoff at Expiration

| Stock Price | Short $95 Put Value | Long $90 Put Value | Net P/L |

|---|---|---|---|

| $100 | $0 | $0 | +$190 |

| $97 | $0 | $0 | +$190 |

| $95 | $0 | $0 | +$190 (max profit) |

| $93.10 | -$1.90 | $0 | $0 (breakeven) |

| $92 | -$3.00 | $0 | -$110 |

| $90 | -$5.00 | $0 | -$310 (max loss) |

| $85 | -$10.00 | +$5.00 | -$310 (max loss) |

| $80 | -$15.00 | +$10.00 | -$310 (max loss) |

Below $90, additional losses on the short put are offset by gains on the long put. Your loss is capped at $310 regardless of how far the stock falls.

Pro Tip

Ideal Market Conditions

Bullish or neutral outlook. The stock needs to stay above your short strike. You do not need the stock to rally — just to not crash. This gives you three winning scenarios: stock goes up, stock stays flat, or stock declines slightly.

Elevated implied volatility. When IV is high, put premiums are inflated. Selling puts in this environment captures richer credits. If IV subsequently contracts, both puts lose value, but the short put (which you want to decrease) loses more in absolute terms.

Strong support nearby. Place your short strike at or below a significant support level. If the stock bounces off support, your spread profits. Technical support adds an extra layer of conviction to the trade.

Trending or range-bound markets. Bull put spreads work well in uptrends (the stock keeps rising away from your strikes) and in range-bound markets (the stock oscillates but stays above your short strike). They struggle in downtrends.

Choosing Strike Prices and Width

Short put strike selection: This is your key decision. A higher strike (closer to the money) generates more premium but has a higher probability of being tested. A lower strike generates less premium but has a wider margin of safety.

| Strike Selection | Delta | Probability OTM | Typical Credit (5-wide) |

|---|---|---|---|

| ATM ($100) | ~0.50 | ~50% | $2.80 |

| Slightly OTM ($95) | ~0.25 | ~75% | $1.90 |

| Far OTM ($90) | ~0.15 | ~85% | $1.00 |

Spread width: Wider spreads offer larger credits but also larger maximum losses. Common widths are $2.50, $5, and $10.

| Width | Credit | Max Loss | Breakeven Distance |

|---|---|---|---|

| $2.50 | $0.90 | $160 | $4.10 below stock |

| $5.00 | $1.90 | $310 | $6.90 below stock |

| $10.00 | $3.50 | $650 | $6.50 below stock |

Most traders use $5 wide spreads as the default. They offer a good balance of credit size, risk, and capital efficiency.

Expiration Selection

30-45 DTE is the standard recommendation. At this timeframe, theta decay is accelerating but you have enough time for the trade to work. Shorter expirations generate less total premium. Longer expirations tie up capital and expose you to more price risk.

Weekly expirations work for traders who want rapid turnover. You sell a new spread each week. The premium per trade is smaller, but you can compound more frequently.

Pre-earnings expirations can be attractive because IV inflates before the announcement, boosting put premiums. However, the gap risk on earnings is significant. Only sell bull put spreads through earnings on stocks where you have high conviction the stock will not breach your short strike.

Managing the Position

Take profits at 50-75% of max credit. If you collected $1.90 and the spread is now worth $0.50, you have captured $1.40 of the $1.90 potential. Close the trade by buying back the spread for $0.50. This locks in profit and frees capital for the next trade.

Cut losses at 2x the credit received. If you collected $1.90 and the spread is now worth $3.80, you have lost twice your potential profit. This is a sign the trade is not working. Close and move on.

Roll when tested. If the stock is approaching your short strike with time remaining, you can roll the spread:

Rolling Down

Close the current spread and open a new one at lower strikes. This gives you more room but may result in a debit (net cost) for the adjustment. The total risk increases.

Rolling Out in Time

Close the current spread and open the same strikes at a later expiration. This buys more time for the stock to recover and often generates an additional credit because the later expiration has more premium.

Rolling Down and Out

Combine both: lower strikes and later expiration. This is the most aggressive adjustment, giving you more room and more time. Use this when you still believe the stock will recover but need breathing room.

Bull Put Spread vs. Cash-Secured Put

| Factor | Bull Put Spread | Cash-Secured Put |

|---|---|---|

| Capital required | Spread width minus credit | Full strike price × 100 |

| Max loss | Spread width minus credit | Strike minus premium to $0 |

| Max profit | Net credit | Net credit |

| Risk type | Defined | Undefined (to $0) |

| Assignment | Possible on short leg | Yes, if ITM |

| Capital efficiency | High | Low |

A $5 bull put spread requires roughly $310 in capital. A cash-secured put at the $95 strike requires $9,500. The bull put spread is 30x more capital efficient while earning similar premium.

The tradeoff is that cash-secured puts result in stock ownership (which you may want), while bull put spreads are purely income trades.

Real-World Example

AAPL trades at $185. It has strong support at $175 and you are moderately bullish after a recent pullback.

Trade: Sell $175/$170 bull put spread, 35 DTE

- Sell $175 put: $3.40

- Buy $170 put: $2.10

- Net credit: $1.30 ($130 per contract)

- Max loss: ($175 - $170 - $1.30) × 100 = $370

- Breakeven: $175 - $1.30 = $173.70

Outcome 1: AAPL stays at $185. Both puts expire worthless. You keep the full $130 credit. Return: $130 / $370 = 35.1% in 35 days.

Outcome 2: AAPL drops to $176. Both puts still expire worthless (above $175 strike). Full $130 profit.

Outcome 3: AAPL drops to $172. Short put is worth $3.00, long put is worthless. Spread costs $3.00 to close. Loss: $3.00 - $1.30 = $170.

Outcome 4: AAPL crashes to $160. Both puts are ITM. Spread is worth $5.00 (max width). Loss: $5.00 - $1.30 = $370 (max loss).

Common Mistakes

Selling too close to the money. Chasing high premiums by selling ATM puts increases your probability of loss. The sweet spot is 1-2 standard deviations OTM (roughly 0.15-0.30 delta on the short put).

Ignoring the risk-reward ratio. A spread that collects $0.50 on a $5 width risks $4.50 to make $0.50. That is a 9:1 risk-reward against you. Even with high probability, one loss wipes out nine wins.

Not having a management plan. Decide before entering the trade: at what profit level will you close? At what loss level will you exit? Will you roll if tested? Write these rules down.

Overleveraging with spreads. Because spreads require less capital, it is tempting to sell many contracts. Ten contracts on a $5 wide spread risks $3,700. That is real money. Size positions so that a max loss on any single trade is no more than 2-3% of your account.

Frequently Asked Questions

What happens if the stock is between my two strikes at expiration?

The short put (higher strike) is ITM and may be assigned, while the long put (lower strike) expires worthless. You would be assigned 100 shares at the higher strike price. To avoid this, close the spread before expiration whenever the stock is near your strikes.

Can I turn a cash-secured put into a bull put spread?

Yes. If you have a short put and the stock starts declining, you can buy a lower-strike put to create a bull put spread. This caps your maximum loss at the spread width minus your total credit. This is a common defensive adjustment.

Is a bull put spread the same as a short put vertical?

Yes. Bull put spread, short put vertical, and put credit spread all describe the same strategy: selling a higher-strike put and buying a lower-strike put for a net credit.

How does assignment work on a bull put spread?

If the short put is assigned, you buy 100 shares at the short put strike. You can then exercise your long put to sell those shares at the long put strike, limiting your loss to the spread width minus the credit. Most brokers handle this automatically, but it may briefly require margin. Close spreads before expiration to avoid assignment mechanics entirely.

What is the ideal win rate for bull put spreads?

With a typical credit of 30-33% of the spread width, you need to win roughly 70% of your trades to be profitable long-term. If you take profits at 50% of max credit and cut losses at 2x credit, the required win rate drops to around 60%.

Disclaimer

This is educational content, not financial advice. Trading involves risk, and you should consult a qualified financial advisor before making any investment decisions. Past performance does not guarantee future results.

Related Articles

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.