Calendar Spreads: Profiting from Time Decay Differences

⚡ Key Takeaways

- A calendar spread uses the same strike price but different expiration dates to exploit the difference in time decay rates

- The near-term short option decays faster than the longer-term long option, creating a theta advantage

- Calendar spreads profit most when the stock stays near the strike price through the near-term expiration

- These spreads benefit from rising implied volatility and are hurt by falling IV

- Maximum loss is limited to the net debit paid to enter the trade

What Is a Calendar Spread?

A calendar spread (also called a time spread or horizontal spread) is an options strategy that involves buying and selling options at the same strike price but with different expiration dates. You sell a near-term option and buy a longer-term option, paying a net debit to enter the position.

The strategy profits from the difference in time decay rates between the two options. The near-term option you sold decays faster than the longer-term option you own. As the short option loses value, the spread widens and your position gains value.

Calendar spreads are neutral strategies at their core. They profit most when the stock stays near the chosen strike price. However, they can be positioned with a directional bias by choosing strikes above (bullish) or below (bearish) the current stock price.

This strategy is more nuanced than simple credit spreads or debit spreads because it involves two different expiration cycles, introducing additional variables like term structure and vega sensitivity that traders must consider.

How to Construct a Calendar Spread

The standard calendar spread construction is straightforward:

Long call calendar:

- Sell 1 call at strike X with near-term expiration

- Buy 1 call at strike X with longer-term expiration

Long put calendar:

- Sell 1 put at strike X with near-term expiration

- Buy 1 put at strike X with longer-term expiration

Both call and put calendars behave similarly when placed at-the-money. The choice between calls and puts often comes down to liquidity.

For example, stock XYZ is trading at $100:

| Leg | Strike | Expiration | Action | Premium |

|---|---|---|---|---|

| Front month call | $100 | 30 days | Sell | $3.00 |

| Back month call | $100 | 60 days | Buy | $4.50 |

| Net debit | $1.50 |

Net Debit = Back Month Premium - Front Month Premium = $4.50 - $3.00 = $1.50 per share ($150 per contract)Your maximum loss is the $150 debit paid. This occurs if the stock makes a very large move in either direction, causing both options to have similar values.

The Theta Advantage Explained

The core mechanism of the calendar spread is the differential theta decay between the front-month and back-month options.

Options do not lose time value at a constant rate. Theta decay follows a curve that accelerates as expiration approaches. An option with 30 days left loses value much faster per day than an option with 60 days left.

Approximate Theta Relationship: Theta is proportional to 1/√(days to expiration). A 30-day option has roughly √2 = 1.41x the daily decay of a 60-day option at the same strike.This means your short front-month option is decaying approximately 41% faster than your long back-month option. Each day, the short option loses more value than the long option, and since you are short that decaying option, the difference flows into your pocket as profit.

At the front-month expiration, the ideal scenario is:

- The short option expires at-the-money (worthless or near-zero)

- The long option retains significant time value plus any remaining extrinsic value

- The spread is worth more than the $1.50 you paid

| Days to Front Expiration | Short Option Theta | Long Option Theta | Net Theta (Your Benefit) |

|---|---|---|---|

| 30 days | -$0.05 | -$0.035 | +$0.015/day |

| 15 days | -$0.07 | -$0.04 | +$0.03/day |

| 7 days | -$0.10 | -$0.045 | +$0.055/day |

| 3 days | -$0.15 | -$0.05 | +$0.10/day |

The theta advantage accelerates as the front month approaches expiration, which is why the final two weeks are the most profitable period for a calendar spread.

Pro Tip

The Volatility Component

Calendar spreads have a unique relationship with implied volatility (IV) that makes them a powerful tool for volatility traders.

The back-month option has higher vega than the front-month option because longer-dated options are more sensitive to changes in IV. Since you own the back-month option, your net vega is positive. This means:

- Rising IV benefits calendar spreads (the back month gains more than the front month)

- Falling IV hurts calendar spreads (the back month loses more than the front month)

This makes calendars excellent pre-event plays when you expect implied volatility to rise leading into an event but the stock to stay range-bound. For example, placing a calendar spread several weeks before an earnings announcement can profit from the IV run-up, as long as the stock does not move significantly.

However, be cautious about holding calendars through the event. After earnings or other catalysts, IV typically crashes (IV crush), which damages your back-month option's value.

| IV Scenario | Impact on Calendar Spread |

|---|---|

| IV rises 5 points | Positive: spread widens ~$0.30-$0.50 |

| IV stays flat | Neutral: theta decay drives profits |

| IV drops 5 points | Negative: spread narrows ~$0.30-$0.50 |

| IV term structure steepens | Very positive |

| IV term structure flattens | Negative |

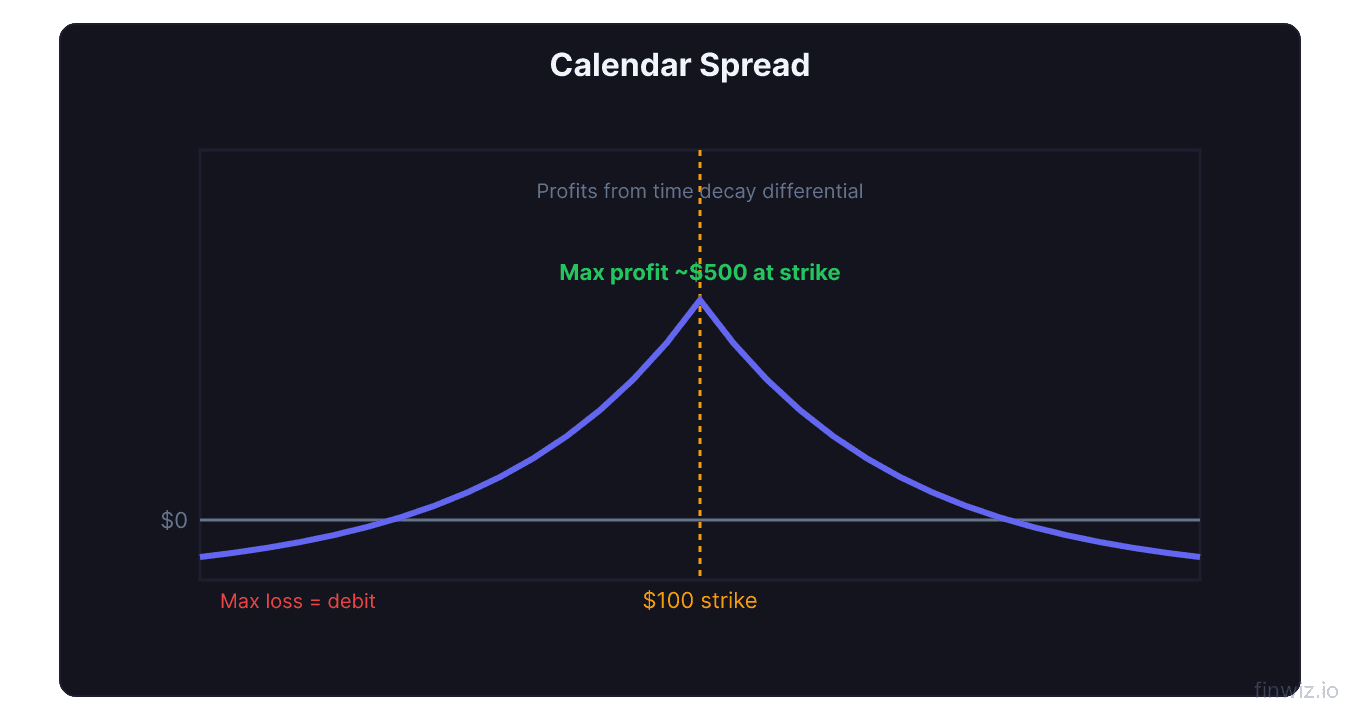

Maximum Profit, Loss, and Breakeven

The profit and loss profile of a calendar spread is different from vertical spreads because it depends on the value of the back-month option at the front-month expiration.

Maximum profit occurs when the stock is exactly at the strike price at front-month expiration. At that point, the short option expires worthless and the long option retains its maximum time value. The exact max profit depends on the back-month option's value at that point, which is influenced by IV and days remaining.

Maximum loss is the net debit paid ($1.50 in our example). This occurs if the stock moves far away from the strike in either direction. When the stock is far ITM or far OTM, both options have similar values (either mostly intrinsic or nearly zero), and the spread collapses.

Breakeven points cannot be calculated with a simple formula because they depend on the back-month option's value at front-month expiration. You need an options pricing model or your broker's profit/loss analyzer to determine the exact breakeven range.

Typically, the profit zone covers a range of approximately 1 standard deviation around the strike price, though this varies with the specific options and time remaining.

Managing Calendar Spreads

Calendar spreads require active management because the two different expirations add complexity.

At front-month expiration, you have several choices:

Choice 1: Close the entire spread. If the spread is profitable (worth more than the $1.50 you paid), close both legs. This is the simplest approach and locks in your gain.

Choice 2: Roll the front month. If the stock is near the strike and you want to continue the trade, buy back the expired front-month option and sell the next month's option at the same strike. This creates a new calendar spread and collects additional credit.

Choice 3: Keep the back-month option. If you have a directional view, let the front-month expire and hold the back-month option as a standalone position. This changes the trade from neutral to directional.

Before front-month expiration:

- If the spread reaches 50-75% of expected max profit, consider closing early

- If the stock has moved significantly away from the strike, the spread will lose value. Close it to preserve capital rather than hoping for a reversal

- If IV drops sharply, the spread's value will decline. Evaluate whether to close or hold

Double and Triple Calendar Spreads

More advanced traders use multiple calendar spreads at different strikes to create a wider profit zone.

A double calendar places calendars at two different strikes, typically one above and one below the current price. This widens the profit zone significantly and creates a structure similar to a strangle but with defined risk.

For example, with the stock at $100:

- Calendar 1: Sell/buy $97 calls (30/60 day)

- Calendar 2: Sell/buy $103 calls (30/60 day)

The double calendar profits if the stock stays between approximately $94 and $106, a much wider range than a single calendar. The trade-off is higher cost since you are paying two debits.

A triple calendar adds a third strike, typically at-the-money, creating an even wider profit zone. This further increases cost but provides the widest range of profitability.

| Variation | Strikes | Cost | Profit Zone Width |

|---|---|---|---|

| Single calendar | 1 | Low | Narrow |

| Double calendar | 2 | Moderate | Wide |

| Triple calendar | 3 | Higher | Widest |

Calendar Spreads vs Other Neutral Strategies

Calendars compete with several other neutral strategies. Understanding the trade-offs helps you pick the right tool.

| Strategy | IV Preference | Theta Benefit | Max Risk | Complexity |

|---|---|---|---|---|

| Calendar spread | Low (benefits from rising) | Moderate | Debit paid | Moderate |

| Butterfly | Low | High at pin | Debit paid | Moderate |

| Iron condor | High (benefits from falling) | High | Strike width - credit | Moderate |

| Short straddle | High | Very high | Unlimited | Low |

Calendars are best when you expect the stock to stay range-bound and implied volatility to rise or stay stable. If you expect IV to drop, iron condors or butterflies are better choices since they benefit from falling volatility.

Frequently Asked Questions

What is the ideal stock price relative to the strike for a calendar spread?

The stock should be at or very near the strike price when you enter the trade. Calendar spreads are neutral strategies that profit from the stock staying in place. If you have a directional bias, you can place the strike slightly above (bullish) or below (bearish) the current price, but the stock should not need to make a large move to reach the strike.

How do calendar spreads handle earnings announcements?

Calendars can profit from the IV build-up before earnings because rising IV benefits the back-month option more than the front-month. However, if you hold through earnings and the stock makes a large move, both legs may lose value. The safest approach is to close the calendar before the earnings announcement or structure it so the front-month option expires before earnings while the back month spans the event.

Can I construct a calendar spread for a net credit?

Standard calendars are always entered for a debit because longer-dated options cost more than shorter-dated options at the same strike. However, in unusual situations with inverted volatility term structures (near-term IV much higher than long-term IV), it is theoretically possible but very rare. A reverse calendar (selling the back month and buying the front month) generates a credit but has the opposite risk profile.

How wide should the expiration gap be between the two options?

The most common approach is 30 days apart (e.g., 30-day front month and 60-day back month). Wider gaps (30 and 90 days) provide more theta differential but cost more. Narrower gaps reduce cost but also reduce the theta advantage. A 30-day gap offers the best balance for most traders.

What is the biggest risk with calendar spreads?

The biggest risk is a large price move in either direction. If the stock gaps up or down significantly, the spread collapses because both options end up with similar values (either deep ITM with mostly intrinsic value or deep OTM with near-zero value). The second major risk is a sharp drop in implied volatility, which hurts the back-month option more than the front month.

Disclaimer

This is educational content, not financial advice. Trading involves risk, and you should consult a qualified financial advisor before making any investment decisions. Past performance does not guarantee future results.

Related Articles

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.