Options Expiration & Quadruple Witching: What Happens & Why It Matters

⚡ Key Takeaways

- Options expire on specific dates — monthly options on the third Friday, weekly options every Friday

- Quadruple witching occurs four times per year when stock options, index options, stock futures, and index futures expire simultaneously

- Pin risk occurs when the stock closes very near a strike price at expiration, creating uncertainty about assignment

- Max pain is the strike price at which the most options contracts expire worthless, theoretically where market makers benefit most

- Always manage positions before expiration day to avoid unexpected assignment and margin issues

Understanding Options Expiration

Options expiration is the date and time when an options contract ceases to exist. After this point, the holder no longer has the right to buy or sell the underlying asset, and the contract becomes worthless. Understanding how expiration works is essential for every options trader because it affects strategy selection, trade management, and risk.

Every options contract has a defined lifespan. Unlike stocks, which you can hold indefinitely, options are time-limited instruments. This expiration creates both the opportunity (leverage and defined risk) and the primary challenge (time decay) of options trading.

The expiration date is not just an academic detail. It directly impacts the value of your position, the urgency of your trade management, and the risks you face in the final days and hours of the contract's life. Traders who do not understand expiration mechanics often face unexpected losses, unwanted stock positions, or missed opportunities.

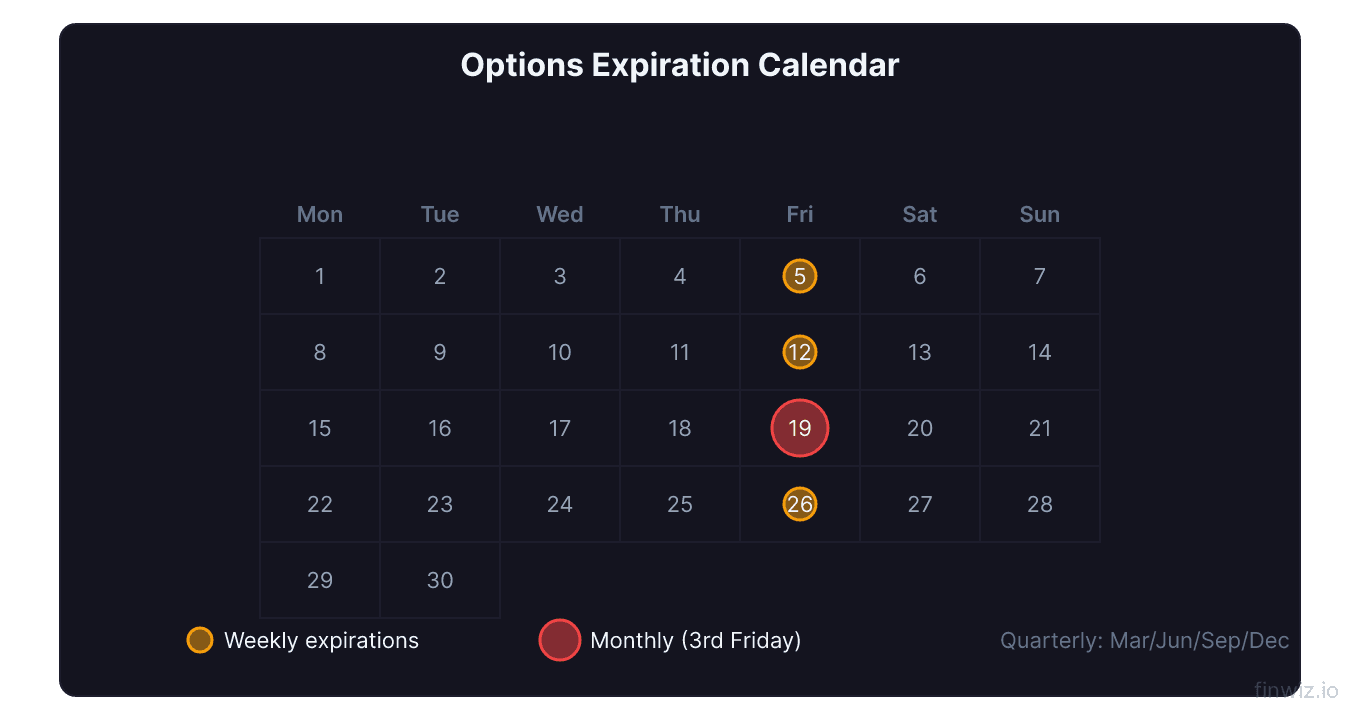

Monthly and Weekly Expiration Cycles

Options are available in multiple expiration cycles, each serving different trading purposes.

Monthly options expire on the third Friday of each month (or the Thursday before if Friday is a holiday). These are the original and most liquid options contracts. Monthly expirations are available for 2-3 months out on most stocks, and further out on popular names.

Weekly options (also called "weeklies") expire every Friday. They were introduced in 2005 and have grown enormously in popularity. Weeklies offer shorter time frames for traders who want to:

- Make short-term directional bets

- Sell premium with rapid time decay

- Trade around specific events (earnings, economic data)

LEAPS (Long-Term Equity Anticipation Securities) expire in January of each year, typically 1-3 years out. These provide long-term exposure similar to stock ownership.

| Expiration Type | Frequency | Typical Use | Liquidity |

|---|---|---|---|

| Weekly | Every Friday | Short-term trading, events | High (popular stocks) |

| Monthly | 3rd Friday | Core trading, strategies | Highest |

| Quarterly | End of quarter | Institutional hedging | Moderate |

| LEAPS | January, 1-3 years | Long-term investing | Lower |

Key timing detail: Options technically expire on Saturday, but the last trading day is Friday. All trading and decision-making must happen by market close on Friday (4:00 PM Eastern). After-hours trading on the underlying stock can still trigger exercise decisions through the OCC's cutoff (typically 5:30 PM Eastern).

Quadruple Witching Explained

Quadruple witching (sometimes still called triple witching) occurs four times per year on the third Friday of March, June, September, and December. On these dates, four types of derivatives contracts expire simultaneously:

- Stock index futures (S&P 500, Nasdaq, Dow futures)

- Stock index options (SPX, NDX options)

- Single stock options (regular equity options)

- Single stock futures (less common today)

The simultaneous expiration creates unusually high trading volume and increased volatility, particularly in the final hour of trading (known as the "witching hour"). On a typical quadruple witching day, volume can be 2-3 times the daily average.

| Quadruple Witching Dates | Typical Impact |

|---|---|

| 3rd Friday of March | High volume, increased volatility |

| 3rd Friday of June | Portfolio rebalancing activity |

| 3rd Friday of September | Heightened intraday swings |

| 3rd Friday of December | Year-end positioning adds to activity |

Why does this matter? The increased volume comes from institutional investors rolling positions, closing expiring contracts, and rebalancing portfolios. This can cause sharp, seemingly random price movements in the final hours that have nothing to do with fundamental news. Individual traders should be aware that their orders may fill at unexpected prices during these periods.

Pro Tip

Pin Risk: The Expiration Day Danger

Pin risk is the uncertainty that occurs when a stock's price is very close to a strike price at expiration. It creates a situation where you do not know whether your short option will be assigned or expire worthless.

Here is the problem: You sold a $100 call option, and at 3:55 PM on expiration Friday, the stock is trading at $100.05. Is the call in-the-money? Technically yes, but:

- The stock could drop below $100 in the final minutes

- After-hours trading could push it above or below $100

- The option holder might or might not choose to exercise

If assigned, you owe 100 shares. If not assigned, nothing happens. You will not know the outcome until the next business day. This uncertainty is pin risk.

Why stocks "pin" to strike prices:

There is a phenomenon where stocks tend to close at or very near popular strike prices on expiration day. This happens because of delta hedging by market makers. As the stock approaches a heavily traded strike, market makers buy or sell shares to maintain their delta-neutral hedge, which paradoxically pushes the stock toward the strike.

How to manage pin risk:

- Close positions before 3:00 PM on expiration day if the stock is within 1-2% of your short strike

- Do not hold spreads to expiration if only one leg might be in-the-money

- Have a plan for being assigned — ensure you have sufficient capital and margin

Assignment: What Happens When Your Option Is Exercised

Assignment occurs when the option holder exercises their right, and you (as the seller) must fulfill your obligation.

Call assignment: You must sell 100 shares at the strike price. If you own the shares (covered call), they are delivered. If you do not own them (naked call), you are short 100 shares and must eventually buy them back.

Put assignment: You must buy 100 shares at the strike price. If you have the cash (cash-secured put), the shares are purchased. If you do not have sufficient cash, you may face a margin call.

When does assignment happen?

- At expiration: Any option that is in-the-money by $0.01 or more is automatically exercised by the OCC (Options Clearing Corporation) unless the holder submits a "do not exercise" instruction

- Before expiration (early assignment): Can happen at any time with American-style options, but is most common:

- On puts when the stock drops well below the strike

- On calls just before an ex-dividend date

- When the option has very little or no time value remaining

| Assignment Scenario | Your Obligation | Capital Impact |

|---|---|---|

| Short call assigned | Sell 100 shares at strike | Deliver shares or go short |

| Short put assigned | Buy 100 shares at strike | Purchase shares |

| Spread — one leg assigned | Complex — may need to exercise other leg | Potential margin impact |

Pro Tip

Max Pain Theory

Max pain (also called the maximum pain point or max pain price) is the strike price at which the greatest number of options contracts (both puts and calls) would expire worthless. The theory suggests that the stock price tends to gravitate toward this level at expiration.

Max Pain = The strike price where the total dollar value of expiring in-the-money options is minimized across all strikesThe theory behind max pain:

Options market makers and institutional sellers collect premium when they sell options. Their maximum profit occurs when the most options expire worthless. Max pain theory suggests that these large players may use their trading power to push the stock toward the max pain price, minimizing the total payout to option holders.

How to calculate max pain:

For each strike price, calculate the total intrinsic value of all in-the-money calls and puts at that price. The strike where this total is lowest is the max pain price. Most options analytics tools calculate this automatically.

| Strike | Total Call Pain (all ITM calls) | Total Put Pain (all ITM puts) | Combined Pain |

|---|---|---|---|

| $95 | $5,000,000 | $500,000 | $5,500,000 |

| $97.50 | $3,200,000 | $900,000 | $4,100,000 |

| $100 | $1,800,000 | $1,800,000 | $3,600,000 |

| $102.50 | $800,000 | $3,100,000 | $3,900,000 |

| $105 | $300,000 | $5,200,000 | $5,500,000 |

In this example, $100 is the max pain price.

Does max pain work? Research shows that stocks close near the max pain level more often than random chance would suggest, especially on monthly expiration dates with high open interest. However, it is not a reliable trading signal on its own. Strong fundamental or technical factors easily override the max pain effect.

Expiration Week Strategy Adjustments

The final week before expiration requires specific adjustments to your trading approach because of accelerating theta decay and increasing gamma risk.

Gamma risk is the biggest concern. Gamma measures how quickly delta changes. In the final week, gamma spikes for at-the-money options. This means your position's delta (and therefore its profit/loss) can change dramatically with small stock movements.

For long option holders (buyers):

- If your option is profitable, take profits early in the week. Do not wait for Friday.

- If your option is at-the-money with modest profit, time decay will erode value rapidly. Close it.

- If your option is out-of-the-money with a few days left, it will likely expire worthless. Close for whatever residual value remains.

For short option holders (sellers):

- If your short option is well out-of-the-money (less than $0.05-$0.10), you may let it expire. But buying it back for $0.01-$0.05 eliminates all risk for minimal cost.

- If your short option is at-the-money, the gamma risk is extreme. Close it to avoid sudden adverse moves.

For spread holders:

- Close spreads before the final day to avoid the risk of having only one leg assigned

- Butterfly spreads near max profit should be closed early since pinning at the exact strike is unlikely

Rolling Positions Before Expiration

Rolling means closing your current options position and opening a new one at a later expiration. This is the primary alternative to letting an option expire.

Roll forward (same strike, later expiration): Used when your thesis is intact but needs more time. You buy back the current option and sell the same strike at a later date.

Roll up and out (higher strike, later expiration): Used for profitable positions where you want to capture more upside. Common with covered calls where the stock has risen.

Roll down and out (lower strike, later expiration): Used when a position is under pressure. Common with short puts where the stock has declined.

| Roll Type | When to Use | Typical Cost |

|---|---|---|

| Forward | Thesis intact, need time | Small debit or credit |

| Up and out | Position profitable, want higher target | Usually credit |

| Down and out | Position under pressure | Usually debit |

Roll Credit/Debit = New Option Premium - Current Option's Buyback CostWhen to roll vs when to close:

- Roll if your thesis is intact and the roll can be done for a net credit or small debit

- Close if the thesis has changed or the roll requires a large debit that worsens your risk-reward

- Close if you have already rolled once or twice and the position continues going against you

After-Hours Expiration Risks

An often-overlooked risk is what happens after the market closes on expiration day. Options officially stop trading at 4:00 PM Eastern, but the underlying stock continues to trade in the after-hours session.

The OCC allows option holders to submit exercise instructions until 5:30 PM Eastern. This means a stock could make a significant move between 4:00 and 5:30 that changes whether your option is in-the-money.

Example: You sold a $100 call. The stock closes at $99.90 at 4:00 PM — your call is out-of-the-money and you expect it to expire worthless. But at 5:15 PM, the company announces an acquisition and the stock jumps to $105 in after-hours trading. The option holder now exercises the call, and you are assigned despite the option appearing to be OTM at the close.

This is rare but it happens, particularly on days when companies release earnings after the close. To avoid this risk entirely, close positions before 3:30 PM on expiration day.

Frequently Asked Questions

What time do options expire on expiration day?

Options stop trading at 4:00 PM Eastern on expiration day (the market close). However, the official expiration is technically Saturday. Option holders have until 5:30 PM Eastern Friday to submit exercise instructions to the OCC. This after-hours window creates risk for sellers who think their OTM options are safe at the 4:00 PM close.

What happens if I do nothing with an expiring in-the-money option?

If your long option is in-the-money by $0.01 or more at expiration, it will be automatically exercised by the OCC. A long call results in purchasing 100 shares at the strike price. A long put results in selling 100 shares (or going short if you do not own shares). Ensure you have sufficient capital or shares to handle auto-exercise, or close the position before expiration.

Should I ever let options expire worthless?

For long options that are out-of-the-money near expiration, you can let them expire, but selling for whatever residual value remains ($0.01-$0.05) is often worth it. For short options that are far out-of-the-money, many traders buy them back for a few cents to eliminate assignment risk entirely. The peace of mind is worth the small cost.

How does expiration affect options pricing?

As expiration approaches, time value (theta) decays rapidly. An option with 30 days left might have $3.00 of time value. With 7 days left, that might drop to $1.20. With 1 day left, perhaps $0.30. This accelerating decay means the final week is when options lose value the fastest. Buyers should be cautious holding into this period; sellers benefit from it.

What is OpEx and why do traders watch it?

OpEx is trading shorthand for "options expiration." Traders watch it because expiration-related activity — delta hedging, rolling positions, and closing contracts — can cause unusual stock price behavior. Monthly OpEx (third Friday) typically has more impact than weekly expirations. Quadruple witching OpEx dates have the most extreme volume and volatility.

Disclaimer

This is educational content, not financial advice. Trading involves risk, and you should consult a qualified financial advisor before making any investment decisions. Past performance does not guarantee future results.

Related Articles

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.