Collar Strategy: Protecting Gains with Puts & Covered Calls

⚡ Key Takeaways

- A collar strategy combines long stock, a long protective put, and a short covered call on the same underlying

- The put protects against downside while the call premium offsets the put cost, often creating a zero-cost collar

- Maximum profit is capped at the call strike, and maximum loss is limited to the put strike minus the stock price plus net premium

- Collars are ideal for protecting gains on appreciated stock positions without spending money on pure insurance

- The strategy sacrifices upside potential in exchange for downside protection at little or no cost

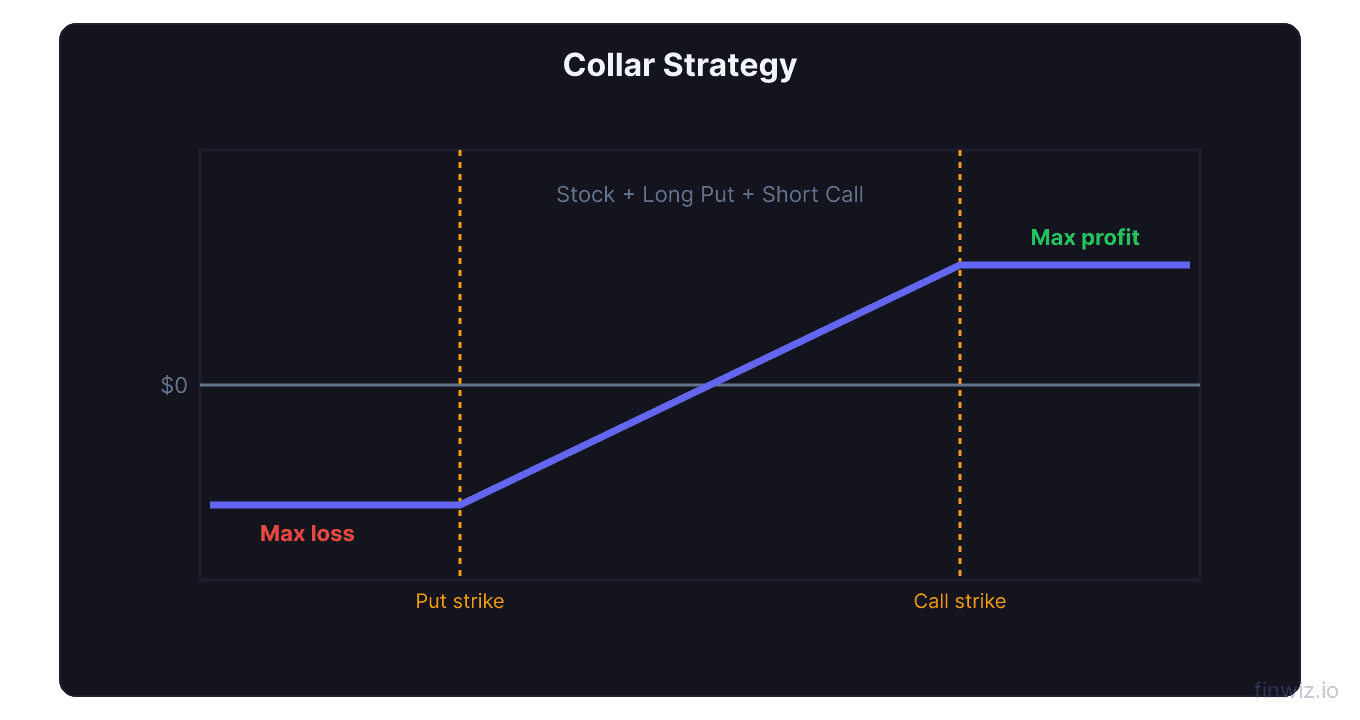

What Is a Collar Strategy?

A collar strategy is a three-part options position consisting of long stock, a long put option, and a short call option, all on the same underlying security. The put provides downside protection while the call generates premium income that offsets the put's cost.

If you own 100 shares of a stock that has appreciated significantly and you want to protect your gains without selling, the collar locks in a range of outcomes. Your profit is capped at the call strike, and your loss is floored at the put strike. In between, you participate normally in the stock's movement.

The collar is essentially a protective put funded by a covered call. By combining these two strategies, you eliminate or dramatically reduce the cost of protection.

How to Construct a Collar

You need three components:

- Own 100 shares of the underlying stock

- Buy 1 put below the current stock price (downside protection)

- Sell 1 call above the current stock price (upside cap)

Both options should have the same expiration date.

Example: You own 100 shares of XYZ purchased at $80, now trading at $100.

| Component | Action | Details |

|---|---|---|

| Stock | Own | 100 shares at $100 current price |

| Put | Buy 1 $95 put | Pay $2.50 premium |

| Call | Sell 1 $110 call | Receive $2.50 premium |

| Net cost | $0.00 (zero-cost collar) |

The put premium exactly offsets the call premium, creating a zero-cost collar. Your downside is protected below $95 and your upside is capped at $110.

Zero-Cost Collar Explained

A zero-cost collar occurs when the premium received from selling the call equals the premium paid for buying the put. You spend nothing on the protection.

To achieve zero cost, you typically need to sell a call closer to the current price than the put. If the ATM call and ATM put had equal premiums, you could create a zero-cost collar with symmetric strikes. In practice, you adjust the strikes until the premiums match.

Finding the zero-cost strikes:

| Put Strike | Put Cost | Call Strike Needed for Zero Cost | Call Premium |

|---|---|---|---|

| $95 | $2.50 | $110 | $2.50 |

| $92 | $1.50 | $107 | $1.50 |

| $90 | $0.90 | $105 | $0.90 |

The further OTM your put (more risk), the further OTM your call can be (more upside). You are trading protection tightness for upside room.

Pro Tip

Payoff Analysis

Using our zero-cost collar example ($100 stock, $95 put, $110 call):

| Stock Price | Stock P/L | Put Value | Call Value | Net P/L |

|---|---|---|---|---|

| $120 | +$2,000 | $0 | -$1,000 | +$1,000 |

| $115 | +$1,500 | $0 | -$500 | +$1,000 |

| $110 | +$1,000 | $0 | $0 | +$1,000 |

| $105 | +$500 | $0 | $0 | +$500 |

| $100 | $0 | $0 | $0 | $0 |

| $95 | -$500 | $0 | $0 | -$500 |

| $90 | -$1,000 | +$500 | $0 | -$500 |

| $80 | -$2,000 | +$1,500 | $0 | -$500 |

| $50 | -$5,000 | +$4,500 | $0 | -$500 |

Maximum Profit = (Call Strike − Current Stock Price + Net Credit) × 100Key numbers:

- Maximum profit: ($110 - $100) x 100 = $1,000 (10% gain)

- Maximum loss: ($100 - $95) x 100 = $500 (5% loss)

- Breakeven: $100 (zero-cost collar)

- Risk-reward ratio: $1,000 / $500 = 2:1

No matter what happens, your outcome is between -$500 and +$1,000. The stock could crash 50% and you lose only $500. It could double and you gain only $1,000.

When to Use a Collar

Protecting unrealized gains. Your stock has doubled and you do not want to sell for tax reasons or long-term conviction, but you want to protect the gain. A collar locks in most of the profit.

Before earnings on a core holding. You own a stock you plan to hold for years, but earnings could cause a short-term drop. A collar protects against the gap without forcing you to sell and re-enter.

Concentrated stock positions. Employees with large holdings of company stock can collar the position to protect their net worth while maintaining ownership for tax or corporate reasons.

Near retirement. If your portfolio relies on a few large positions, collars protect against catastrophic loss during the critical years when you need the money.

Volatile markets. When the VIX is elevated and you are nervous about a broad market decline but do not want to sell, collars provide peace of mind.

Collar vs. Protective Put Alone

| Feature | Collar | Protective Put |

|---|---|---|

| Cost | Zero or near zero | Premium paid |

| Downside protection | Yes | Yes |

| Upside participation | Capped at call strike | Unlimited |

| Best for | Protecting gains at no cost | Protecting gains while keeping full upside |

| Net cash flow | Neutral or positive | Negative |

The collar wins on cost. The protective put wins on upside potential. Choose based on your priority.

If you believe the stock could rally significantly and you do not want to cap that potential, pay for the protective put. If you are more concerned about downside risk and willing to sacrifice some upside, use the collar.

Choosing Strike Prices

Put strike (downside floor): Place this at the maximum loss you are willing to accept. If you own a stock at $100 and can tolerate a 5% drop, buy the $95 put. If you can only tolerate 3%, buy the $97 put.

Call strike (upside cap): Place this at a level where you would be happy selling. If the stock is at $100 and you would be thrilled with a 10% gain, sell the $110 call.

Width of the collar determines your range of outcomes:

| Collar Width | Put Strike | Call Strike | Max Loss | Max Profit |

|---|---|---|---|---|

| Narrow ($5/$5) | $95 | $105 | $500 | $500 |

| Medium ($5/$10) | $95 | $110 | $500 | $1,000 |

| Wide ($5/$15) | $95 | $115 | $500 | $1,500 |

| Asymmetric ($10/$5) | $90 | $105 | $1,000 | $500 |

Wider collars give you more room to profit but may not achieve zero cost. Narrower collars are easier to make zero cost but restrict your outcomes to a tight band.

Expiration Selection

Short-term collars (30-60 DTE) work for specific events like earnings. They are cheaper and allow you to remove the collar after the event passes.

Quarterly collars (60-90 DTE) provide extended protection for uncertain periods. They require fewer roll transactions but tie up more extrinsic value.

LEAPS collars (6-12 months) are used for long-term hedging of concentrated positions. The call premium for selling a 12-month LEAPS can be substantial, funding a well-protected put. However, you cap your upside for an entire year.

Managing the Collar Position

If the stock rises to the call strike: Decide whether to let the shares be called away (sold at the strike), or roll the call up and out (buy back the current call, sell a higher-strike, later-dated call). Rolling costs money but preserves your stock position with a higher cap.

If the stock drops to the put strike: The put protection kicks in. You can exercise the put to sell shares at the strike, or sell the put for its intrinsic value. If you want to keep the shares, sell the put for profit, which offsets the stock loss.

If the stock stays flat: Both options decay toward zero. At expiration, you can let them expire and decide whether to put on a new collar for the next period.

Rolling the collar: As expiration approaches, close both options and open a new collar at a later expiration. This is standard maintenance for long-term hedging positions.

Real-World Example: Protecting a Winning Position

You bought 100 shares of NVDA at $120 a year ago. The stock is now $280, giving you an unrealized gain of $16,000. You are bullish long term but worried about a tech sector pullback.

Trade: Zero-cost collar, 60 DTE

- Buy 1 NVDA $260 put: $12.00 ($1,200)

- Sell 1 NVDA $310 call: $12.00 ($1,200)

- Net cost: $0

Outcomes:

- NVDA drops to $200: Your loss is limited to $280 - $260 = $20 per share ($2,000). You still keep $14,000 of your $16,000 gain.

- NVDA rises to $350: Your profit is capped at $310 - $280 = $30 per share ($3,000). Total gain from original purchase: $19,000.

- NVDA stays at $280: Both options expire worthless. No gain or loss from the collar.

Without the collar, a crash to $200 would cost you $8,000 of your unrealized gain. The collar saves you $6,000 in that scenario while only costing $3,000 of potential upside if NVDA rallies past $310.

Tax Considerations

Collars can trigger constructive sale rules if the put strike and call strike are too close to the current stock price. A constructive sale means the IRS treats you as if you sold the stock, triggering capital gains taxes even though you still hold the shares.

To avoid constructive sale treatment:

- Keep the put meaningfully out of the money (at least 5-10% below current price)

- Keep the call meaningfully out of the money (at least 5-10% above current price)

- Avoid using deep ITM options for either leg

Consult a tax professional before putting on a collar if you have significant unrealized gains and the tax implications are material.

Frequently Asked Questions

What is the main disadvantage of a collar?

The main disadvantage is capped upside. By selling the call, you give up all gains above the call strike. If the stock rallies significantly, you miss out on the excess return. This is the price of free (or cheap) downside protection.

Can I use a collar on an ETF or index?

Yes. Collars work on any optionable security, including ETFs like SPY, QQQ, and IWM. Index collars are popular for protecting broad portfolio exposure without selling individual positions.

What happens at expiration if the stock is between the put and call strikes?

Both options expire worthless, and you keep your shares unchanged. The collar had no effect on the final outcome. You can put on a new collar for the next period if you still want protection.

Is a collar the same as a risk reversal?

No. A risk reversal is a collar without the stock. It involves buying a call and selling a put (or vice versa) without an underlying stock position. A collar always includes ownership of the underlying shares.

How often should I roll my collar?

Most traders roll every 30-90 days, depending on the expiration chosen. Roll before the final week to avoid assignment risk on the short call and loss of time value on the long put. Some traders maintain continuous collar coverage on core holdings year-round.

Disclaimer

This is educational content, not financial advice. Trading involves risk, and you should consult a qualified financial advisor before making any investment decisions. Past performance does not guarantee future results.

Related Articles

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.