Put Options Explained: Profiting from Downside Moves

⚡ Key Takeaways

- A put option gives the buyer the right to sell 100 shares at the strike price before expiration

- Puts profit when the underlying stock declines, making them ideal for hedging and bearish speculation

- The maximum loss for a put buyer is limited to the premium paid

- Put sellers collect premium but are obligated to buy shares at the strike price if assigned

- Protective puts act as portfolio insurance, capping downside risk while preserving upside potential

How Put Options Work

A put option is a contract that gives the buyer the right to sell 100 shares of an underlying stock at a specified strike price before the expiration date. The buyer pays a premium for this right, and the seller receives that premium in exchange for the obligation to buy shares if the put is exercised.

Puts are the mirror image of call options. While calls profit from rising prices, puts profit from falling prices. This makes puts uniquely valuable in a trader's toolkit because they allow you to profit from declines or protect your portfolio against them.

Every put contract is defined by:

- Strike price — The price at which you can sell the stock

- Expiration date — The last day to exercise the contract

- Premium — The price paid for the contract

When the stock price falls below the strike price, the put is in the money and has intrinsic value. If the stock stays above the strike, the put expires worthless.

Buying Puts: Profiting from Declines

Buying a put is the most direct way to profit from a stock's decline without short selling. When you buy a put, you pay a premium and gain the right to sell 100 shares at the strike price.

Here is a concrete example. Stock XYZ trades at $80. You buy a $75 put expiring in 30 days for $2.00 per share, costing you $200 total.

Put Buyer Profit = (Strike Price − Stock Price at Expiration − Premium Paid) × 100| Scenario | Stock at Expiration | Option Value | Profit/Loss |

|---|---|---|---|

| Stock crashes | $60 | $15.00 | +$1,300 (650% return) |

| Moderate decline | $70 | $5.00 | +$300 (150% return) |

| Slight decline | $74 | $1.00 | -$100 (-50% loss) |

| Flat | $80 | $0.00 | -$200 (100% loss) |

| Stock rises | $90 | $0.00 | -$200 (100% loss) |

The breakeven point for a long put is the strike price minus the premium paid:

Put Breakeven = Strike Price − Premium PaidIn this example, the breakeven is $75 − $2.00 = $73.00. The stock must fall 8.75% from $80 just to break even.

Pro Tip

Puts for Hedging: Portfolio Insurance

One of the most practical uses of put options is hedging — protecting an existing stock position against a decline. This strategy is called a protective put or a married put.

Suppose you own 100 shares of ABC stock at $120 per share ($12,000 position). You are concerned about a potential pullback over the next 60 days but do not want to sell the stock and trigger a taxable event.

Protective put setup:

- Own 100 shares at $120

- Buy 1 ABC $115 put, 60 DTE, for $3.50

- Cost of protection: $350

| Stock at Expiration | Stock P/L | Put Value | Net P/L |

|---|---|---|---|

| $140 | +$2,000 | $0 | +$1,650 |

| $130 | +$1,000 | $0 | +$650 |

| $120 | $0 | $0 | -$350 |

| $115 | -$500 | $0 | -$850 |

| $110 | -$1,000 | $5.00 (+$500) | -$850 |

| $100 | -$2,000 | $15.00 (+$1,500) | -$850 |

| $80 | -$4,000 | $35.00 (+$3,500) | -$850 |

No matter how far the stock falls, your maximum loss is capped at $850 ($500 from stock decline to the strike + $350 premium). Without the put, a crash to $80 would cost you $4,000.

The trade-off is clear: you give up $350 of potential profit (the premium) in exchange for catastrophic downside protection. Think of it as paying for insurance on your house — you hope you never need it, but it provides peace of mind.

Puts for Speculation: Bearish Bets

Beyond hedging, puts are powerful instruments for speculating on stock declines. Traders buy puts when they believe a stock is overvalued, facing headwinds, or about to report disappointing earnings.

Advantages of buying puts over short selling:

| Factor | Buying Puts | Short Selling |

|---|---|---|

| Max loss | Premium paid | Unlimited |

| Capital required | Premium only | 50%+ margin |

| Borrowing costs | None | Interest on borrowed shares |

| Dividend risk | None | Must pay dividends |

| Timing pressure | Expiration date | Indefinite (but margin calls) |

The key disadvantage of buying puts is time decay. Your option loses value every day, so you need the stock to move down quickly enough to overcome the daily erosion of theta.

Selling Puts: Collecting Premium

Selling (writing) puts is a popular income strategy. When you sell a put, you collect the premium and accept the obligation to buy 100 shares at the strike price if the buyer exercises.

The most common version is the cash-secured put, where you set aside enough cash to buy the shares if assigned. This strategy works best when you are willing to own the stock at a lower price.

Cash-secured put example:

- Stock trades at $50

- Sell 1 $45 put, 30 DTE, for $1.50

- Cash set aside: $4,500 (to buy 100 shares at $45)

- Premium collected: $150

Best case: The stock stays above $45, the put expires worthless, and you keep the $150 premium. That is a 3.3% return on your $4,500 in just 30 days.

Worst case: The stock crashes to $30. You are assigned 100 shares at $45 and your effective cost basis is $43.50 (strike minus premium). Your unrealized loss is $1,350.

Pro Tip

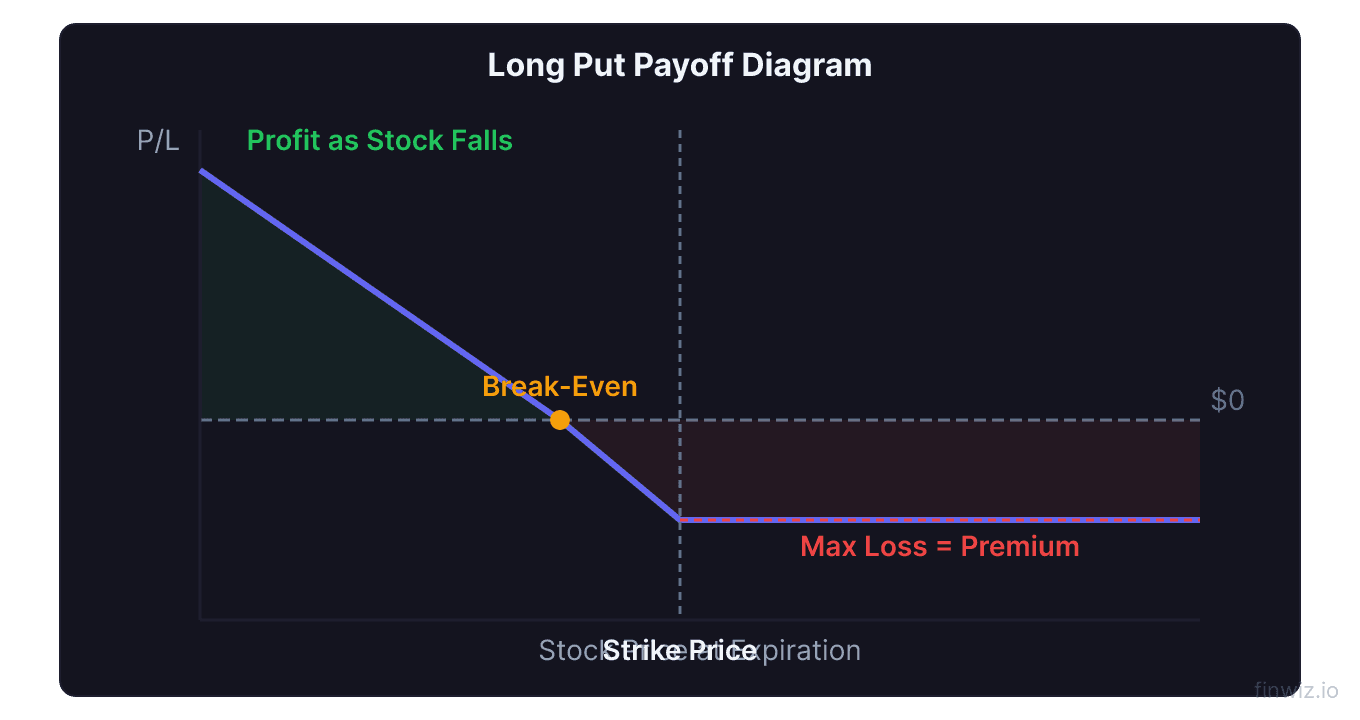

Put Option Payoff Diagram

The payoff diagram for a long put shows:

- A flat line at the maximum loss (premium paid) for all stock prices above the strike

- A breakeven point where the line crosses zero at strike price minus premium

- A downward-sloping profit line as the stock falls below breakeven

For a long put at a $100 strike purchased for $4.00:

| Stock Price | Payoff | Net P/L |

|---|---|---|

| $115 | $0 | -$400 |

| $105 | $0 | -$400 |

| $100 | $0 | -$400 |

| $96 | $4 | $0 (breakeven) |

| $90 | $10 | +$600 |

| $80 | $20 | +$1,600 |

| $70 | $30 | +$2,600 |

The maximum profit on a long put is theoretically limited because a stock cannot fall below zero. The maximum profit equals (Strike Price − Premium) × 100, which in this case would be ($100 − $4) × 100 = $9,600 if the stock went to $0.

Choosing the Right Put Strike

Strike selection determines your balance between cost, probability, and potential reward.

In-the-money puts (strike above stock price) cost more but have a higher probability of profit. They have high delta values (closer to -1.0) and behave more like short stock.

At-the-money puts offer the most extrinsic value and the best balance of leverage and probability. They have deltas around -0.50.

Out-of-the-money puts are cheap but require a significant drop to profit. They are popular for hedging because you can protect against large drops at a low cost.

| Strike Type | Example (stock at $100) | Typical Cost | Delta | Breakeven |

|---|---|---|---|---|

| Deep ITM | $115 put | $16.50 | -0.90 | $98.50 |

| ATM | $100 put | $4.00 | -0.50 | $96.00 |

| OTM | $90 put | $1.20 | -0.20 | $88.80 |

| Far OTM | $80 put | $0.30 | -0.05 | $79.70 |

For hedging, most traders buy 5-10% OTM puts because they provide meaningful protection at a reasonable cost. For speculation, ATM or slightly OTM puts offer the best risk-reward.

Real-World Example: Buying Puts Before Earnings

Company DEF is trading at $200. You believe the stock is overvalued and expect a disappointing earnings report in one week.

Trade setup:

- Buy 2 DEF $195 puts, 10 DTE, for $5.50 each

- Total cost: $1,100

- Breakeven: $189.50

Outcome: Stock drops to $175 after a revenue miss. Put value at expiration: $20.00 each. Total value: $4,000. Profit: $4,000 − $1,100 = $2,900 (264% return).

Compare this to short selling 200 shares at $200:

- Short sale proceeds: $40,000

- Buy to cover at $175: $35,000

- Profit: $5,000

- But margin required: approximately $20,000 (50% margin requirement)

The put trade risked $1,100 and returned $2,900. The short sale risked $20,000+ in margin (with unlimited risk) and returned $5,000. On a percentage-of-capital-risked basis, the puts were far more efficient.

Managing Put Positions

Effective management separates profitable put traders from those who consistently lose.

Close winners early. If your put reaches 50-80% of its maximum profit, consider closing. The last 20% of profit is often not worth the risk of a reversal.

Use stop losses. If the stock moves against you and the put loses 40-50% of its value, cut your losses. Do not let a thesis hold you hostage.

Roll down and out. If the stock drops but not enough, you can sell your current put and buy a lower-strike, later-dated put to give the trade more time and a better breakeven.

Convert to a spread. If implied volatility spikes after you buy a put, sell a lower-strike put against it to lock in some of the IV gain. This creates a bear put spread.

Puts vs. Short Selling

Both strategies profit from declines, but they differ in fundamental ways.

Short selling involves borrowing shares and selling them, hoping to buy them back at a lower price. The risk is theoretically unlimited because the stock can rise indefinitely. Short sellers must maintain margin, pay borrowing costs, and can face short squeezes.

Buying puts involves paying a fixed premium for the right to sell at a set price. The risk is limited to the premium. There are no borrowing costs, no margin calls, and no short squeeze risk.

For most retail traders, puts are the safer and more practical way to bet on declines. Short selling is best left to institutional traders with sophisticated risk management systems.

Frequently Asked Questions

Can I sell a put option if I do not own the stock?

Yes. Selling a put does not require stock ownership. You are agreeing to buy shares at the strike price if assigned. The most conservative approach is a cash-secured put, where you hold enough cash to purchase the shares. If you sell puts without sufficient cash or margin, you face the risk of a margin call.

What happens if my put option is assigned?

If your short put is assigned, you are obligated to buy 100 shares at the strike price. The shares will appear in your account, and cash equal to the strike price times 100 will be debited. Your effective cost basis is the strike price minus the premium you collected.

Why do puts get more expensive when the market drops?

When markets fall, fear increases and demand for protective puts surges. This drives up implied volatility, which inflates put premiums. This phenomenon is captured by the VIX, often called the "fear gauge," which measures implied volatility of S&P 500 options.

Is buying puts the same as being short the stock?

Not exactly. Buying puts gives you leveraged, time-limited, defined-risk bearish exposure. Being short stock gives you unleveraged, indefinite, undefined-risk bearish exposure. Puts also benefit from rising implied volatility, while short stock does not. The two strategies have different risk profiles, capital requirements, and profit characteristics.

When should I buy puts instead of using a bear put spread?

Buy outright puts when you expect a large, quick move and implied volatility is low. Use a bear put spread when IV is elevated (to offset the cost) or when you expect a moderate decline rather than a crash. Spreads cost less but cap your profit potential.

Disclaimer

This is educational content, not financial advice. Trading involves risk, and you should consult a qualified financial advisor before making any investment decisions. Past performance does not guarantee future results.

Related Articles

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.