Covered Calls: How to Generate Income from Your Stock Holdings

⚡ Key Takeaways

- A covered call involves selling a call option against 100 shares of stock you own

- Maximum profit is capped at the strike price minus your stock cost plus the premium collected

- The strategy generates income in flat or slowly rising markets

- Assignment risk means you may be forced to sell your shares at the strike price

- Covered calls reduce your cost basis over time but limit upside participation in strong rallies

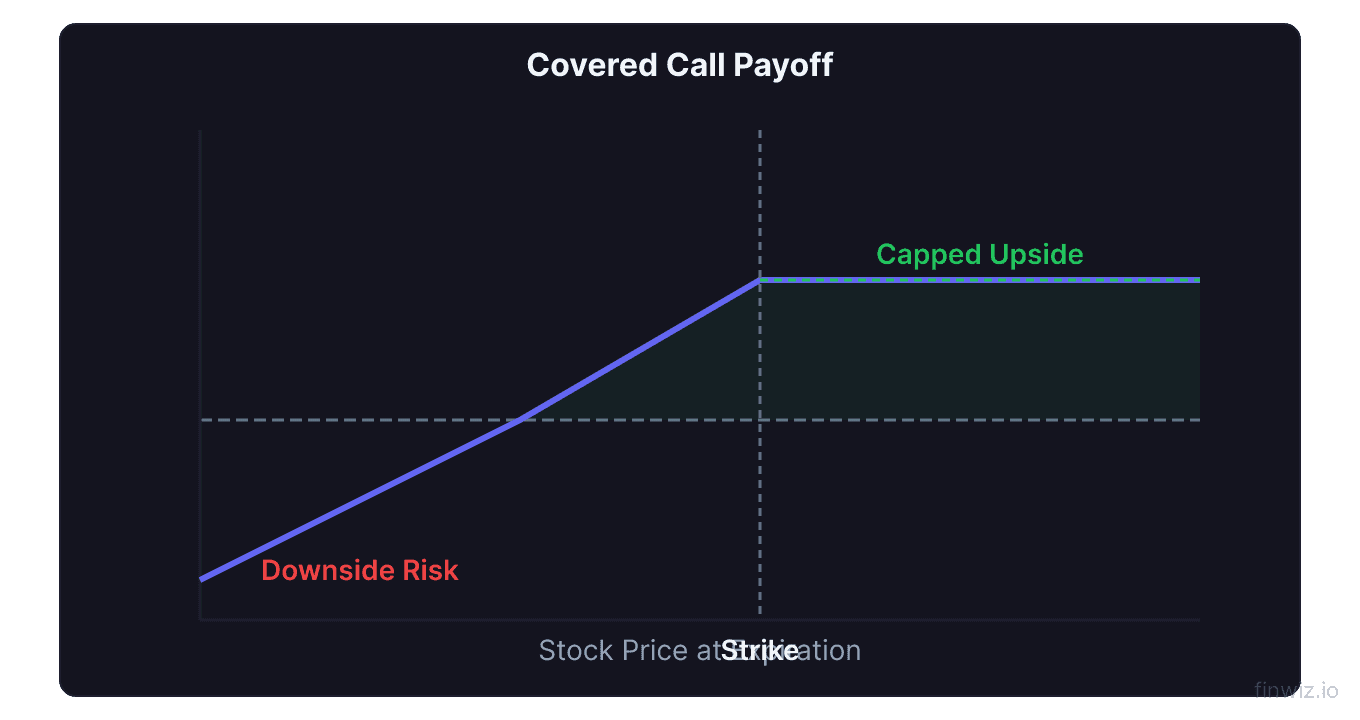

What Is a Covered Call?

A covered call is an options strategy where you sell a call option against shares of stock you already own. For every 100 shares, you sell one call contract. The call is "covered" because your stock position acts as collateral, eliminating the unlimited risk associated with naked calls.

This is one of the most popular and beginner-friendly options strategies. It generates income from your stock holdings by collecting premium from call buyers who want exposure to your stock's upside.

The trade-off is straightforward: you receive income today in exchange for capping your upside potential. If the stock surges past your strike price, you must sell your shares at the strike, missing out on additional gains above that level.

How to Set Up a Covered Call

Setting up a covered call requires two components:

- Own 100 shares (or multiples of 100) of the underlying stock

- Sell 1 call option per 100 shares at a strike price above the current stock price

Example: You own 100 shares of XYZ at $50 per share. You sell a $55 call expiring in 30 days for $1.50 per share.

| Component | Details |

|---|---|

| Stock position | 100 shares at $50 ($5,000 invested) |

| Call sold | 1x $55 call, 30 DTE |

| Premium collected | $1.50 × 100 = $150 |

| Max profit | ($55 − $50 + $1.50) × 100 = $650 |

| Breakeven | $50 − $1.50 = $48.50 |

| Max loss | ($48.50 − $0) × 100 = $4,850 |

The premium collected ($150) lowers your effective cost basis from $50 to $48.50 per share, providing a small cushion against declines.

Covered Call Max Profit = (Strike Price − Stock Purchase Price + Premium Collected) × 100The Income Strategy

Covered calls shine as an income-generating strategy. By repeatedly selling calls against your shares, you can generate a steady stream of premium income that supplements dividends.

Here is what a year of covered calls might look like on a $50 stock:

| Month | Strike | Premium | Stock Price | Outcome |

|---|---|---|---|---|

| Jan | $55 | $1.20 | $52 | Expired worthless, keep premium |

| Feb | $55 | $1.40 | $54 | Expired worthless, keep premium |

| Mar | $53 | $1.80 | $51 | Expired worthless, keep premium |

| Apr | $55 | $1.00 | $57 | Assigned, sold stock at $55 |

| Total | — | $5.40 | — | $540 income + $500 appreciation |

Over four months, you collected $540 in premium income on a $5,000 investment (10.8% return), plus $500 in stock appreciation when assigned in April. The total return was $1,040 or 20.8%.

Without the covered calls, you would have made $700 in April (from $50 to $57). So the covered call outperformed in months 1-3 but limited your gain in April when the stock rallied strongly.

Pro Tip

Strike Price Selection

Choosing the right strike price is the most important decision in covered call writing. It determines your income, probability of assignment, and upside cap.

Out-of-the-money (OTM) calls — strike above current price:

- Lower premium income

- Higher probability the call expires worthless (you keep shares)

- More room for stock appreciation

- Best for moderately bullish outlook

At-the-money (ATM) calls — strike near current price:

- Highest extrinsic value, most premium income

- Roughly 50% chance of assignment

- Less room for appreciation

- Best for neutral outlook

In-the-money (ITM) calls — strike below current price:

- Highest total premium but includes intrinsic value

- High probability of assignment

- Provides the most downside protection

- Best for slightly bearish outlook (you want to exit the position)

| Strike | Stock at $50 | Premium | Max Profit | Prob. Expires Worthless |

|---|---|---|---|---|

| $45 ITM | $50 | $6.50 | $150 | ~20% |

| $50 ATM | $50 | $3.00 | $300 | ~50% |

| $55 OTM | $50 | $1.20 | $620 | ~75% |

| $60 OTM | $50 | $0.40 | $1,040 | ~90% |

Most covered call writers use the 30-delta call (approximately one standard deviation OTM), which offers a balance between premium income and the probability of keeping your shares.

Rolling Covered Calls

Rolling is the process of closing your current short call and opening a new one with a later expiration or different strike. This is the primary management technique for covered calls.

Roll out (in time): When your call is near expiration and the stock is below the strike, buy back the current call (cheap) and sell a new call with the same strike but a later expiration. This extends your trade and collects additional premium.

Roll up and out: When the stock has risen above your strike, buy back the current call at a loss and sell a higher-strike, later-dated call to collect more premium. This avoids assignment and raises your cap.

Roll down: When the stock has dropped significantly, buy back the current call (cheap) and sell a lower-strike call to collect more premium. This lowers your breakeven but also lowers your maximum profit.

Example of rolling up and out:

- Original position: Sold $55 call for $1.50, stock now at $57

- Buy back $55 call for $2.50 (loss of $1.00)

- Sell $60 call with later expiration for $2.00 (new credit)

- Net credit from roll: $2.00 − $2.50 = -$0.50 (small debit)

- But you raised your cap from $55 to $60, adding $500 in potential stock appreciation

Pro Tip

Assignment Risk

Assignment occurs when the call buyer exercises their option, and you are obligated to sell your 100 shares at the strike price. This can happen at any time before expiration on American-style options, though it most commonly occurs:

- At expiration — when the call is in the money

- Before an ex-dividend date — if the remaining extrinsic value is less than the upcoming dividend, early assignment is likely

Assignment is not inherently bad. If your strike is above your purchase price, you profit from both the premium collected and the stock appreciation up to the strike.

What to do after assignment:

- Your shares are sold at the strike price

- You keep the premium collected

- You can re-enter the position by buying shares again

- Alternatively, sell a cash-secured put at a lower strike to potentially buy back in at a discount

Avoiding unwanted assignment is primarily about monitoring your call's extrinsic value. As long as there is meaningful extrinsic value, early assignment is unlikely because the call buyer would lose that value by exercising.

Tax Considerations

Covered calls have tax implications that traders should understand:

Qualified covered calls (OTM calls with more than 30 days to expiration) do not affect the holding period of your stock. Your long-term capital gains treatment remains intact.

Unqualified covered calls (deep ITM or short-term calls) can reset the holding period of your stock, potentially converting long-term gains into short-term gains.

If you are assigned, the premium collected is added to the sale price for tax purposes. Your gain is calculated as: (Strike Price + Premium − Purchase Price) × 100.

If the call expires worthless, the premium is treated as a short-term capital gain regardless of how long you held the stock.

Consult a tax professional for advice specific to your situation, as options taxation can be complex.

Covered Calls in Different Market Conditions

| Market Condition | Covered Call Performance | Alternative |

|---|---|---|

| Strong uptrend | Underperforms — capped upside | Hold stock without calls |

| Moderate uptrend | Outperforms — premium + gains | Ideal environment |

| Flat market | Outperforms — premium income | Ideal environment |

| Moderate decline | Better than stock — premium cushion | Consider a collar |

| Strong decline | Loses — premium is small offset | Sell stock or buy puts |

Covered calls are not a hedge. The premium collected provides a small buffer (typically 2-5%), but in a severe decline, you still lose most of your stock value. For true downside protection, combine covered calls with protective puts to create a collar.

Common Mistakes

Selling calls on stocks you do not want to own. Only write covered calls on stocks you are happy holding long-term. If the stock drops, you will be stuck with it.

Selling strikes too close to the current price. While ATM calls pay the most premium, they also have the highest probability of assignment. Give yourself room for moderate appreciation.

Chasing high premiums on volatile stocks. Stocks with high premiums have high premiums for a reason — they are volatile and more likely to make large moves that blow through your strike.

Selling calls right before earnings. Earnings announcements create large moves. If the stock jumps well above your strike, you miss the entire gain above it. Either sell calls with expirations that avoid earnings or skip the month.

Not considering dividends. If you sell a call with little extrinsic value right before the ex-dividend date, you face a high probability of early assignment. The call buyer may exercise to capture the dividend.

Frequently Asked Questions

How much income can I earn from covered calls?

Income varies based on the stock's volatility, the strike you choose, and the expiration timeframe. On average, covered call writers targeting 30-delta strikes can generate 1-3% per month in premium income. Over a year, this adds up to 12-36% in additional income, though results vary significantly with market conditions.

What happens if my covered call is assigned?

You sell 100 shares at the strike price and keep the premium. If the strike is above your purchase price, you earn a profit. If below, you realize a loss, offset partially by the premium. After assignment, you can buy the shares back and sell another covered call, or move on to a different stock.

Should I write covered calls on dividend stocks?

Yes, dividend stocks are excellent candidates for covered calls. The combination of dividends and premium income creates multiple income streams. Just be aware of early assignment risk near ex-dividend dates. Sell calls with enough extrinsic value to discourage early exercise.

What is the difference between a covered call and selling a naked put?

Economically, a covered call and a cash-secured put have the same risk profile. Both profit when the stock stays flat or rises, and both lose when the stock falls. The difference is mechanical: covered calls require stock ownership, while cash-secured puts require cash collateral. Some traders prefer selling puts because it requires less capital and avoids the two-step process of buying stock then selling the call.

Can I write covered calls in a retirement account?

Yes, most brokerages allow covered call writing in IRA and 401(k) accounts because it is considered a conservative strategy. You cannot write naked calls or puts in retirement accounts, but covered calls and cash-secured puts are generally permitted.

Disclaimer

This is educational content, not financial advice. Trading involves risk, and you should consult a qualified financial advisor before making any investment decisions. Past performance does not guarantee future results.

Related Articles

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.