Strangle: A Cheaper Way to Trade Big Moves

⚡ Key Takeaways

- A long strangle involves buying an out-of-the-money (OTM) call and an OTM put with the same expiration date but different strike prices

- Break-even points are calculated as the call strike plus total premium paid (upper) and the put strike minus total premium paid (lower)

- A strangle costs less than a straddle but requires a larger price move to become profitable because both options start OTM

- Maximum loss is the total premium paid, which occurs if the stock stays between the two strike prices at expiration

- Strangles are ideal before high-volatility events like earnings when you expect a big move but want cheaper exposure than a straddle

What Is a Strangle in Options Trading?

A strangle is an options strategy that involves buying an out-of-the-money (OTM) call option and an out-of-the-money put option on the same underlying stock with the same expiration date. Like the straddle, the strangle profits from large price moves in either direction and is a pure volatility play with no directional bias. The key difference is that both options are OTM, making the strangle cheaper to establish but requiring a larger move in the underlying stock to reach profitability.

Traders use strangles when they expect a significant price move — often around earnings announcements, FDA decisions, or other binary events — but are uncertain about the direction. The lower cost of a strangle compared to a straddle appeals to traders who want volatility exposure without paying the higher premiums required for at-the-money options.

How a Long Strangle Works

To construct a long strangle, you buy one OTM call (strike price above the current stock price) and one OTM put (strike price below the current stock price), both with the same expiration date.

| Component | Action | Strike Position | Premium |

|---|---|---|---|

| Call option | Buy 1 contract | OTM (above stock price) | Debit |

| Put option | Buy 1 contract | OTM (below stock price) | Debit |

| Total cost | Call premium + Put premium |

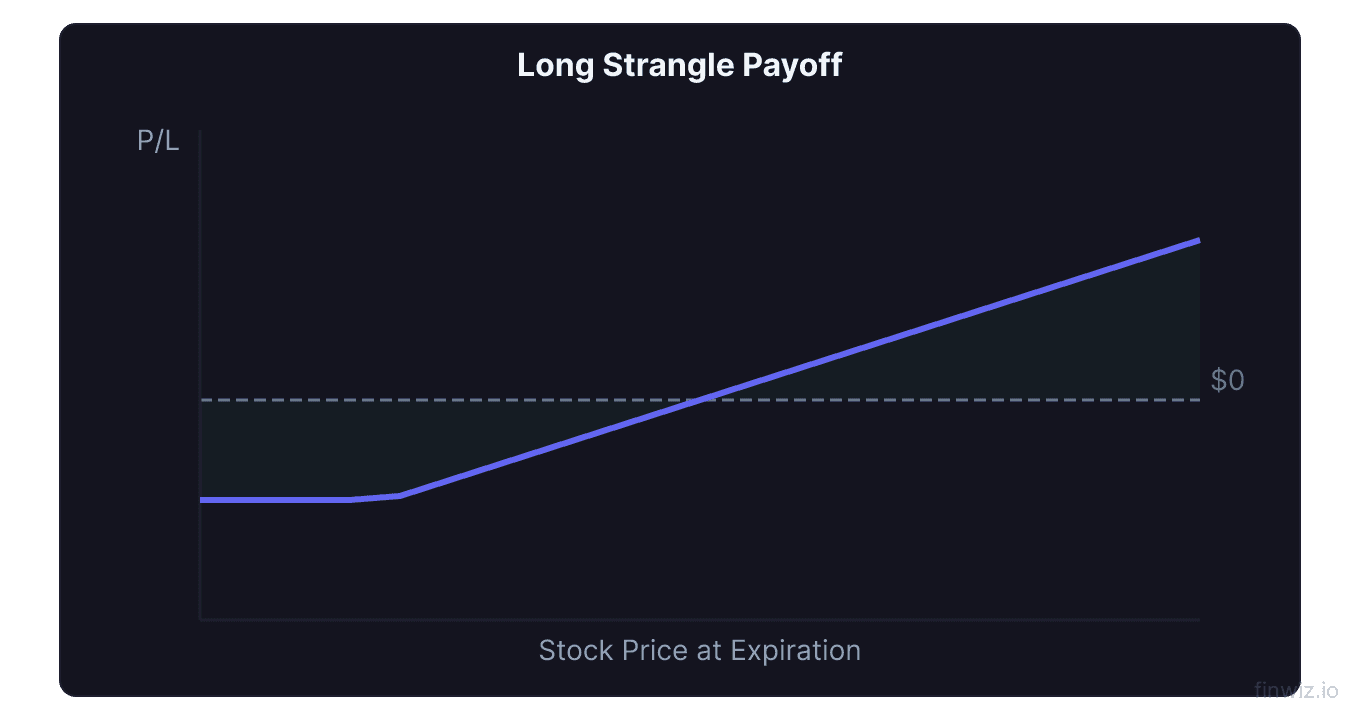

The strangle's payoff diagram forms a wider, shallower V-shape compared to the straddle. The flat bottom of the V (where maximum loss occurs) spans the entire range between the two strike prices, rather than being a single point as in a straddle.

Long Strangle Break-Even Points:Earnings Strangle Example: NVDA

Let's walk through a detailed example using NVIDIA (NVDA) ahead of a quarterly earnings report.

Setup: NVDA is trading at $480 three weeks before earnings. You expect a large post-earnings move based on the stock's history of volatile earnings reactions, but you are uncertain about the direction. You choose a strangle instead of a straddle to reduce your premium outlay.

You buy the $500/$460 strangle expiring the Friday after earnings:

| Leg | Contract | Premium per Share | Total Cost (x100 shares) |

|---|---|---|---|

| Long $500 call (OTM) | 1 contract | $8.00 | $800 |

| Long $460 put (OTM) | 1 contract | $7.00 | $700 |

| Total strangle cost | $15.00 | $1,500 |

Break-even calculation:

- Upper break-even: $500 + $15.00 = $515.00

- Lower break-even: $460 - $15.00 = $445.00

NVDA must move above $515 or below $445 for the strangle to be profitable at expiration. That requires a 7.3% move to the upside or a 7.3% move to the downside from the current $480 price.

Scenario 1: NVDA crushes earnings, stock rallies to $540.

The $500 call is worth $40.00 ($540 - $500). The $460 put expires worthless. Profit = $40.00 - $15.00 = $25.00 per share, or $2,500 total (167% return on premium).

Scenario 2: NVDA misses earnings badly, stock drops to $420.

The $460 put is worth $40.00 ($460 - $420). The $500 call expires worthless. Profit = $40.00 - $15.00 = $25.00 per share, or $2,500 total.

Scenario 3: NVDA reports solid but unexciting results, stock moves to $490.

The $500 call is worth $0 (still OTM). The $460 put is worth $0 (still OTM). Both options expire worthless. Loss = $15.00 per share, or $1,500 total (100% loss of premium).

Scenario 4: NVDA drops modestly to $465.

The $460 put is worth $0 (still OTM at $465). The $500 call is worthless. Loss = $15.00 per share, or $1,500 total. Even though the stock moved $15, it did not move past either strike price, so the strangle loses its full premium.

This final scenario illustrates the strangle's key weakness: the stock can move meaningfully and you still lose everything if the move stays between the two strikes.

Strangle vs. Straddle: Complete Comparison

The strangle and straddle are the two primary volatility strategies. Choosing between them depends on your conviction about the magnitude of the expected move and your willingness to pay premium.

| Feature | Strangle | Straddle |

|---|---|---|

| Call strike | OTM (above stock price) | ATM (at stock price) |

| Put strike | OTM (below stock price) | ATM (same as call) |

| Total premium | Lower | Higher |

| Maximum loss | Lower (less premium at risk) | Higher |

| Break-even width | Wider | Narrower |

| Required move to profit | Larger | Smaller |

| Maximum loss zone | Between two strikes (a range) | Single point (strike price) |

| Delta at entry | Near zero | Near zero |

| Gamma | Lower | Higher |

| Vega | Lower | Higher |

| Theta decay | Lower daily decay | Higher daily decay |

When to choose a strangle over a straddle:

- You believe the stock will make a very large move (greater than the strangle width plus premium)

- You want to reduce your capital at risk per trade

- Implied volatility is already elevated, making ATM options disproportionately expensive

- You are making multiple volatility trades and want to allocate capital across several positions rather than concentrating in one expensive straddle

When to choose a straddle over a strangle:

- You expect a large move but want a lower hurdle to profitability

- The stock has a history of moderate (not extreme) earnings moves

- IV is relatively low, making ATM premiums reasonable

- You want higher gamma to accelerate profits once the stock moves

Pro Tip

Strike Selection for Strangles

Choosing the right strike prices is critical to strangle success. Too close to ATM and you are paying nearly straddle prices. Too far OTM and the required move becomes unrealistic.

Common strike selection approaches:

Delta-based selection. Many traders use the option delta to standardize strike selection. A popular approach is to buy the 25-delta call and the 25-delta put, meaning each option has approximately a 25% probability of being in the money at expiration. Some traders prefer 30-delta strikes for tighter strangles or 20-delta for wider, cheaper strangles.

Percentage-based selection. Choose strikes that are equidistant from the current stock price by a fixed percentage. For example, if the stock is at $480, a 5% strangle would use the $505 call and $455 put. A 10% strangle would use the $530 call and $430 put.

Expected move comparison. The options market prices in an expected move for each expiration cycle. Choose strikes just inside or at the expected move to maximize the probability that the stock reaches your strike if the actual move equals or exceeds the expected move.

| Selection Method | Call Strike | Put Strike | Cost | Required Move | Trade-Off |

|---|---|---|---|---|---|

| Tight (near ATM) | $490 | $470 | Higher | Smaller | Nearly a straddle — high cost |

| Moderate (25 delta) | $500 | $460 | Moderate | Moderate | Best balance of cost and probability |

| Wide (far OTM) | $520 | $440 | Lower | Larger | Cheap but low probability of profit |

How Implied Volatility Affects Strangles

Implied volatility (IV) is a critical factor in strangle pricing, and its behavior before and after events determines a significant portion of the trade's outcome.

IV and entry timing. Strangles are long volatility positions, meaning they benefit from rising IV and suffer from declining IV (vega exposure). Before earnings, IV typically increases as the market anticipates a large move. This IV expansion inflates option premiums, making strangles more expensive to enter.

IV crush. After the earnings announcement, IV collapses sharply — often dropping 30% to 50% or more overnight. This volatility crush reduces the value of both strangle legs regardless of whether the stock moves. Even a favorable stock move may not overcome the damage from IV crush if the move is not large enough.

How to evaluate IV levels. Before entering a strangle, check the IV rank or IV percentile of the underlying stock:

| IV Rank | IV Level | Strangle Premium | Entry Recommendation |

|---|---|---|---|

| 0-20% | Low relative to history | Cheap | Favorable for buying strangles |

| 20-50% | Below average | Moderate | Acceptable |

| 50-80% | Above average | Expensive | Less favorable, larger move needed |

| 80-100% | Very high | Very expensive | Generally avoid buying strangles |

The ideal strangle entry occurs when IV is in the lower half of its historical range and you have reason to believe IV will increase (an upcoming event, technical breakout setup, or news catalyst).

Managing a Strangle Position

Active management can significantly improve strangle outcomes.

Close early when profitable. If the stock makes a large move before expiration, take profits. Do not wait for expiration hoping for additional movement. Time decay accelerates as expiration approaches, and the stock could reverse, giving back your gains.

Adjust the untested side. If the stock moves significantly in one direction (say upward), the put side becomes nearly worthless while the call side gains value. Some traders roll the put up closer to the current stock price, creating a new strangle centered around the higher price. This "rolling" costs additional premium but refreshes the position.

Close the position before earnings if IV has expanded sufficiently. Some traders buy strangles 1 to 2 weeks before earnings specifically to profit from the IV expansion, then close before the announcement to avoid IV crush. This approach treats the strangle as a vega trade rather than a directional bet on the earnings outcome.

Set a time-based exit rule. If the expected catalyst is one week away and the strangle has already lost 30% of its value due to time decay, consider closing to preserve remaining capital rather than watching it erode further.

The Greeks of a Strangle

Understanding the options Greeks helps you manage strangle risk in real time.

Delta: A well-constructed strangle starts with near-zero net delta (the positive delta of the call roughly offsets the negative delta of the put). As the stock moves, delta shifts toward the winning leg. Unlike a straddle, the delta changes more slowly because both options start further from the money.

Gamma: Strangles have positive gamma, meaning delta accelerates as the stock moves in either direction. However, gamma is lower than a straddle's because OTM options have less gamma than ATM options. Gamma increases as expiration approaches, which can help a late-moving stock produce profits.

Theta: Both legs of a strangle experience time decay, and the total theta is negative. However, OTM options decay more slowly (in absolute dollar terms) than ATM options, so the strangle's daily theta decay is lower than a straddle's. This slower decay gives the strangle more time to work.

Vega: The strangle has positive vega exposure, benefiting from rising IV. Total vega is lower than a straddle because OTM options have less vega sensitivity. This means IV crush hurts a strangle less than a straddle in absolute dollar terms, but proportionally it can still be devastating relative to the lower premium paid.

| Greek | Strangle vs. Straddle | Practical Implication |

|---|---|---|

| Delta | Similar (near zero) | Both are direction-neutral |

| Gamma | Lower | Profits accelerate more slowly |

| Theta | Lower daily decay | More time for the trade to work |

| Vega | Lower total exposure | Less hurt by IV crush (but also less help from IV rise) |

Short Strangles: The Other Side of the Trade

While this article focuses on buying strangles, it is worth understanding the short strangle — selling an OTM call and OTM put simultaneously.

Short strangles profit when the stock stays between the two strike prices through expiration. The seller collects premium and hopes both options expire worthless. This is a high-probability strategy (the stock only needs to stay in a range) but carries undefined risk — if the stock makes a huge move, losses can be substantial.

| Feature | Long Strangle | Short Strangle |

|---|---|---|

| Outlook | Expects large move | Expects stock stays in range |

| Max profit | Unlimited | Premium collected |

| Max loss | Premium paid (defined) | Unlimited (undefined) |

| Probability of profit | Lower (~25-35%) | Higher (~65-75%) |

| Best IV environment | Low IV (options are cheap) | High IV (collect more premium) |

| Risk profile | Defined risk | Undefined risk |

Short strangles are popular among experienced options sellers because of their high probability of profit. However, the risk of a single catastrophic loss can wipe out months of collected premium. Many traders prefer selling iron condors instead, which add protective wings to cap maximum loss.

Common Strangle Mistakes

Buying strangles with strikes too far OTM. The cheaper the strangle, the bigger the move needed. A $2.00 strangle requiring a 15% stock move has very low probability of success.

Ignoring the expected move. The options market expected move approximately equals the ATM straddle price. If the expected move is 6% and your strangle requires 10%, you are betting on an outcome the market considers unlikely.

Holding through IV crush without adjustment. Passively holding through earnings means full exposure to IV crush. Plan your exit strategy before entering.

Using strangles on low-volatility stocks. Utility stocks and large consumer staples rarely move enough for strangles. Focus on high-beta stocks with a history of large moves around catalysts.

Frequently Asked Questions

How much can you lose on a strangle?

Your maximum loss on a long strangle is the total premium paid for both the call and the put. This occurs when the stock closes between the two strike prices at expiration, causing both options to expire worthless. In the NVDA example above, the maximum loss was $1,500 (the $15.00 total premium times 100 shares). Unlike a straddle where the maximum loss zone is a single point, the strangle's maximum loss zone spans the entire range between the call and put strikes.

Is a strangle better than a straddle?

Neither is universally better — it depends on the situation. A strangle is better when you want lower cost and are confident the stock will make a very large move. A straddle is better when you want a lower break-even threshold and are willing to pay more premium. If a stock historically moves 8% on earnings, a straddle with 5% break-evens is better than a strangle with 10% break-evens. If you believe the move will be 12% or more, the cheaper strangle maximizes your return on investment.

What is the probability of profit on a strangle?

The probability of profit on a long strangle is typically 20% to 35%, depending on how far OTM the strikes are. Wider strangles have lower probabilities. This low probability is offset by the potential for large returns when the stock does make a major move — a profitable strangle can return 100% to 500% or more on the premium invested. The key is ensuring that your average win is large enough to compensate for the frequency of losses.

When should you buy a strangle vs. sell a strangle?

Buy a strangle when you expect a large move (upcoming earnings, FDA decision, or major event) and IV is relatively low. Sell a strangle when you expect the stock to stay range-bound and IV is elevated (you collect rich premium that will decay as IV normalizes). Buying strangles is a defined-risk strategy suitable for most traders. Selling strangles involves undefined risk and is appropriate only for experienced options traders with sufficient capital and risk management systems.

Can you do a strangle with weekly options?

Yes, weekly options are commonly used for strangles around specific events like earnings. Weekly expirations allow you to target the exact week of the catalyst, minimizing the time value you pay for and focusing the trade on the event itself. The downside is that weekly options have high gamma and rapid theta decay, so if the event is delayed or the move does not happen immediately, the position loses value very quickly. For strangles without a specific catalyst, standard monthly expirations or 30-45 DTE options provide a better balance of time and cost.

Disclaimer

This is educational content, not financial advice. Trading involves risk, and you should consult a qualified financial advisor before making any investment decisions. Past performance does not guarantee future results.

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.