Straddle: Profiting from Big Moves in Either Direction

⚡ Key Takeaways

- A long straddle involves buying an at-the-money (ATM) call and an ATM put with the same strike price and expiration date

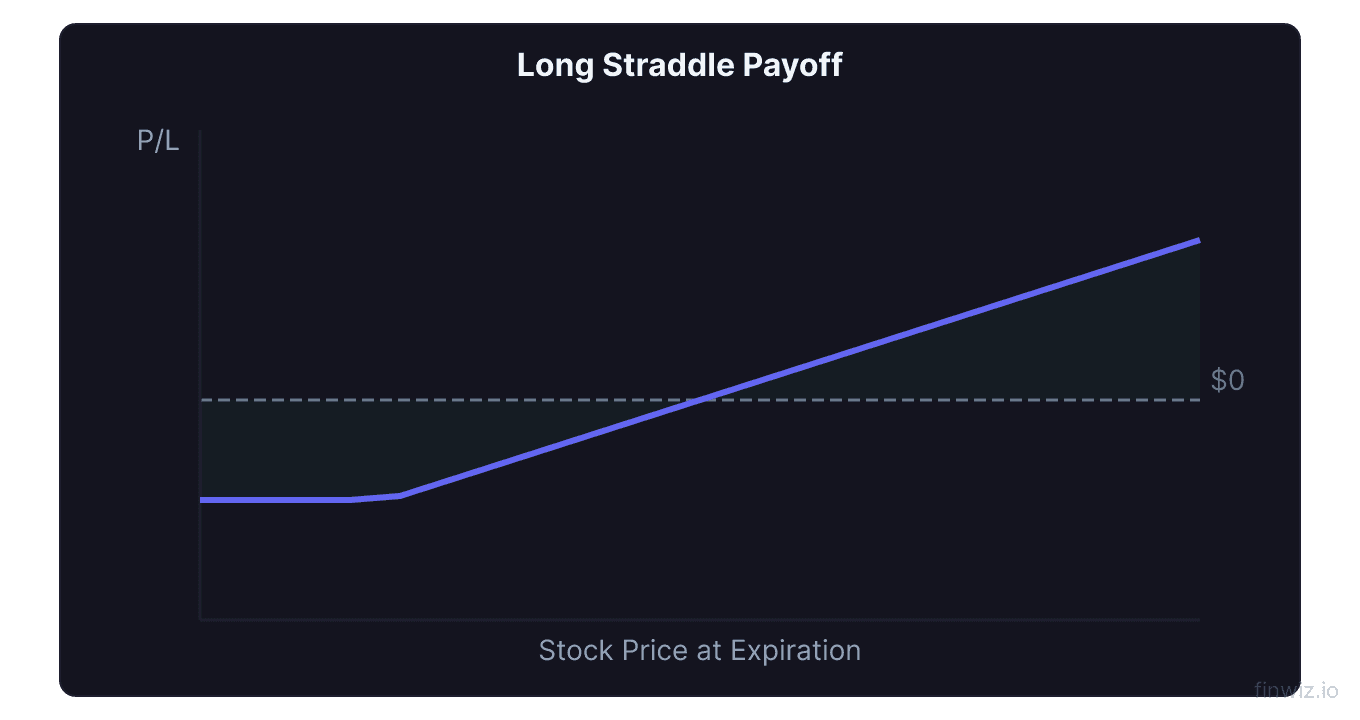

- The payoff diagram forms a V-shape, with profit potential in both directions and maximum loss limited to the total premium paid

- Break-even points are the strike price plus the total premium (upside) and the strike price minus the total premium (downside)

- Straddles work best before high-impact events like earnings announcements, FDA decisions, or major economic reports

- Implied volatility significantly affects straddle pricing — buying when IV is low and selling when IV spikes is the ideal scenario

What Is a Straddle in Options Trading?

A straddle is an options strategy that involves simultaneously buying a call option and a put option at the same strike price and expiration date, with both options at the money (ATM). The strategy profits when the underlying stock makes a large move in either direction, making it a pure volatility play rather than a directional bet. Your maximum loss is limited to the total premium paid for both options, which occurs if the stock stays exactly at the strike price through expiration.

Traders use straddles when they expect a significant price move but are uncertain about the direction. The classic straddle scenario is an upcoming earnings announcement, where the stock could gap sharply higher or lower depending on results. As long as the move exceeds the combined cost of the two options, the straddle is profitable.

How a Long Straddle Works

To construct a long straddle, you buy one ATM call and one ATM put with identical strike prices and expiration dates. Both options should be as close to at the money as possible, meaning the strike price is nearest to the current stock price.

Here is the structure:

| Component | Action | Strike | Premium |

|---|---|---|---|

| Call option | Buy 1 contract | ATM (nearest to stock price) | Debit |

| Put option | Buy 1 contract | ATM (same strike as call) | Debit |

| Total cost | Call premium + Put premium |

The payoff diagram of a straddle forms a distinctive V-shape. The bottom of the V sits at the strike price, where both options expire worthless and you lose the total premium. As the stock moves away from the strike in either direction, one of the two options gains value while the other expires worthless.

Long Straddle Break-Even Points:AAPL Earnings Straddle Example

Let's walk through a real-world example using Apple (AAPL) ahead of a quarterly earnings report.

Setup: AAPL is trading at $195 ahead of earnings. You expect a big move but do not know whether the report will be bullish or bearish. Earnings are in 5 days.

You buy the $195 straddle expiring in one week:

| Leg | Contract | Premium per Share | Total Cost (x100 shares) |

|---|---|---|---|

| Long $195 call | 1 contract | $4.50 | $450 |

| Long $195 put | 1 contract | $4.00 | $400 |

| Total straddle cost | $8.50 | $850 |

Break-even calculation:

- Upper break-even: $195 + $8.50 = $203.50

- Lower break-even: $195 - $8.50 = $186.50

AAPL must move above $203.50 or below $186.50 for the straddle to be profitable at expiration. That is a 4.36% move in either direction.

Scenario 1: AAPL beats earnings, stock jumps to $212.

The $195 call is now worth $17.00 ($212 - $195). The $195 put expires worthless. Your profit is $17.00 - $8.50 = $8.50 per share, or $850 total (100% return on premium).

Scenario 2: AAPL misses earnings, stock drops to $178.

The $195 put is now worth $17.00 ($195 - $178). The $195 call expires worthless. Your profit is $17.00 - $8.50 = $8.50 per share, or $850 total.

Scenario 3: AAPL reports in-line earnings, stock stays at $196.

The $195 call is worth $1.00. The $195 put expires worthless. Your loss is $8.50 - $1.00 = $7.50 per share, or $750 total.

This example illustrates the core dynamic: the straddle needs a move larger than the total premium in either direction to profit.

How Implied Volatility Affects Straddles

Implied volatility (IV) is the single most important factor in straddle pricing, and understanding its impact is critical to straddle profitability. Implied volatility represents the market's expectation of how much the stock will move, and it directly determines option premiums.

Before events like earnings, IV typically rises as traders anticipate a large move. This phenomenon is called the IV run-up. Higher IV means more expensive options, which means a more expensive straddle with wider break-even points.

After the event, IV collapses sharply. This is known as IV crush or volatility crush. Even if the stock moves in your favor, the rapid decline in IV can erode option value and reduce or eliminate your profit.

| Timing | IV Level | Straddle Cost | Break-Even Width | Challenge |

|---|---|---|---|---|

| 2 weeks before earnings | Moderate | Lower | Narrower | Stock may not move before event |

| Day before earnings | Elevated | Higher | Wider | IV crush will be severe |

| After earnings | Collapsed | N/A | N/A | Move already happened |

This creates a dilemma for straddle buyers. Buying early means cheaper premiums but waiting longer for the catalyst. Buying late means paying inflated premiums that require a larger move to overcome.

Pro Tip

The Greeks and Your Straddle

Understanding how the options Greeks affect a straddle helps you manage the position effectively.

Delta: An ATM straddle starts with a near-zero delta because the positive delta of the call roughly offsets the negative delta of the put. This confirms the straddle is direction-neutral at entry. As the stock moves, delta shifts — moving higher increases delta (call dominates), moving lower decreases delta (put dominates).

Gamma: Straddles have high gamma, especially near expiration. This means delta changes rapidly as the stock moves, accelerating profits once the stock breaks past a break-even point. High gamma is the straddle buyer's friend.

Theta: Straddles have high negative theta because you own two options, both losing time value every day. Time decay is the straddle's biggest enemy. Each day that passes without a significant stock move erodes the value of both legs. Theta accelerates as expiration approaches.

Vega: Straddles have high positive vega because you own two options whose values increase when IV rises. A straddle benefits from rising volatility expectations and suffers from declining volatility. This is why IV crush is so damaging to straddle positions.

| Greek | Straddle Exposure | Implication |

|---|---|---|

| Delta | Near zero (neutral) | No directional bias at entry |

| Gamma | High positive | Profits accelerate with stock movement |

| Theta | High negative | Time decay erodes value daily |

| Vega | High positive | Benefits from rising IV, hurt by IV crush |

When to Use a Straddle

Straddles are appropriate in specific market situations. Using them outside these contexts often leads to losses from time decay.

Before earnings announcements. Quarterly earnings are the most common straddle catalyst. Companies like AAPL, TSLA, AMZN, and NVDA routinely move 5% to 10% or more after earnings, making straddles viable if premiums are not already pricing in the expected move.

Ahead of FDA decisions. Biotech and pharmaceutical stocks facing binary FDA approval decisions can move 20% to 50% or more. Companies like those in clinical-stage drug development offer prime straddle setups, though premiums will be extremely elevated.

Before major economic data. Federal Reserve interest rate decisions, jobs reports, and inflation data can trigger broad market moves. Straddles on index options (SPY, QQQ) can capture these moves.

During legal or regulatory uncertainty. Antitrust rulings, patent decisions, or regulatory actions can cause significant price dislocations. If a major ruling is imminent but the outcome is genuinely uncertain, a straddle captures the move regardless of direction.

When IV is historically low. Comparing current IV to its historical range (IV rank or IV percentile) helps identify cheap straddles. If IV rank is below 20%, options are relatively cheap, and a straddle may offer favorable risk-reward even without a specific catalyst.

Straddle vs. Strangle

The straddle and the strangle are closely related strategies, both designed to profit from large moves. The key difference is strike selection.

| Feature | Straddle | Strangle |

|---|---|---|

| Call strike | ATM | OTM (above stock price) |

| Put strike | ATM (same as call) | OTM (below stock price) |

| Total premium | Higher | Lower |

| Break-even width | Narrower | Wider |

| Max loss | Higher (more premium at risk) | Lower |

| Required move to profit | Smaller | Larger |

| Delta at entry | Near zero | Near zero |

A straddle costs more but needs a smaller move to profit. A strangle costs less but needs a larger move. The choice depends on your conviction about the magnitude of the expected move and your risk tolerance.

Managing a Straddle Position

Once you enter a straddle, active management can improve outcomes.

Close early if profitable. If the stock makes a large move before expiration, close the straddle to lock in gains rather than waiting for expiration. Time decay and potential mean reversion can erode profits if you hold too long.

Close the losing leg. If the stock moves significantly in one direction, the losing leg will be nearly worthless. You can close it for a few cents to recover minimal value, or let it expire. Some traders close the losing leg and keep the winning leg to ride further momentum.

Set a maximum loss threshold. Determine before entry how much of the premium you are willing to lose. If the straddle has lost 50% of its value and no catalyst has occurred, it may be better to close and preserve the remaining capital.

Roll to a later expiration. If the expected catalyst is delayed, you can roll the straddle by closing the current position and opening a new one at a later expiration date. This resets time decay but costs additional premium.

Common Straddle Mistakes

Buying when IV is already elevated. This is the most costly mistake. If IV is at the 90th percentile of its historical range, options are expensive, and the straddle needs an unusually large move to be profitable. Always check IV rank or IV percentile before entering.

Holding through IV crush. Many traders buy before earnings and hold through the announcement, only to find that IV crush erases their gains even when the stock moves. If the stock moves 5% but IV drops 40%, the options may barely break even.

Using straddles in low-volatility stocks. Utility stocks and other low-beta names rarely make moves large enough to justify straddle premiums. Focus straddles on stocks with a history of large moves around catalysts.

Ignoring the expected move. The options market prices in an expected move for earnings and other events. This expected move equals approximately the straddle price at expiration. If the actual move is less than the expected move, the straddle loses money. Always compare the straddle cost to the stock's historical earnings moves.

Frequently Asked Questions

How much can you lose on a straddle?

Your maximum loss on a long straddle is the total premium paid for both the call and the put. This occurs if the stock closes exactly at the strike price at expiration, causing both options to expire worthless. In the AAPL example above, the maximum loss was $850 (the $8.50 total premium times 100 shares). You cannot lose more than this amount, which makes straddles a defined-risk strategy.

Is a straddle bullish or bearish?

A straddle is neither bullish nor bearish — it is a volatility strategy. It profits from large moves in either direction and has a near-zero delta at entry, meaning it has no directional bias. You are essentially betting that the stock will move more than the market expects, regardless of whether it moves up or down.

When should you close a straddle?

Close a straddle when one of three conditions is met: the position has reached your profit target, the position has lost more than your predetermined maximum loss, or the expected catalyst has passed. After an earnings announcement, close the straddle promptly because IV crush will rapidly erode remaining time value. If the stock has moved significantly and you are profitable, take the gain rather than waiting for expiration — time decay and mean reversion can give back profits quickly.

Can you sell a straddle instead of buying one?

Yes, a short straddle involves selling an ATM call and an ATM put, collecting premium and profiting when the stock stays near the strike. However, short straddles carry unlimited risk on the upside (stock can rise indefinitely) and substantial risk on the downside (stock can fall to zero). Short straddles are reserved for experienced traders with high risk tolerance and proper margin. Selling iron condors offers a similar but risk-defined alternative.

How do you calculate expected move from a straddle price?

The straddle price at the nearest expiration after an event approximates the market's expected move. If AAPL's ATM straddle expiring the Friday after earnings costs $8.50 with a $195 strike, the market expects AAPL to move roughly $8.50, or about 4.4%, in either direction. If you believe the actual move will exceed this, the straddle is underpriced and potentially a good buy. Historical earnings move data, available on most options platforms, helps you evaluate whether the expected move is reasonable.

Disclaimer

This is educational content, not financial advice. Trading involves risk, and you should consult a qualified financial advisor before making any investment decisions. Past performance does not guarantee future results.

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.