Call Options Explained: How They Work & When to Buy

⚡ Key Takeaways

- A call option gives the buyer the right to purchase 100 shares at the strike price before expiration

- Buying calls offers leveraged upside with risk limited to the premium paid

- Selling calls generates income but creates an obligation to deliver shares if assigned

- Call option payoff at expiration equals the stock price minus the strike price minus the premium paid

- Time decay and implied volatility changes affect call values even when the stock price stays flat

How Call Options Work

A call option is a contract that gives the buyer the right, but not the obligation, to purchase 100 shares of an underlying stock at a specified strike price before or on the expiration date. The buyer pays a premium for this right, and the seller (writer) collects that premium in exchange for accepting the obligation to sell shares if assigned.

Call options are the most straightforward way to profit from a bullish outlook on a stock. When the stock rises above the strike price by more than the premium paid, the call buyer profits. The higher the stock goes, the more the call is worth.

Every call option contract has three defining characteristics:

- Strike price — The price at which you can buy the stock

- Expiration date — The deadline for exercising the contract

- Premium — The cost of the contract (per share, multiply by 100 for total cost)

Buying Calls: The Bullish Bet

Buying a call option is the simplest bullish options strategy. You pay the premium upfront and gain the right to buy 100 shares at the strike price. Your risk is limited to the premium paid, while your profit potential is theoretically unlimited.

Here is a concrete example. Suppose stock XYZ trades at $100. You buy a $105 call option expiring in 30 days for $2.50 per share, costing you $250 total.

| Scenario | Stock at Expiration | Option Value | Profit/Loss |

|---|---|---|---|

| Stock surges | $115 | $10.00 | +$750 (200% return) |

| Moderate rise | $110 | $5.00 | +$250 (100% return) |

| Slight rise | $107 | $2.00 | -$50 (-20% loss) |

| Flat | $100 | $0.00 | -$250 (100% loss) |

| Stock drops | $90 | $0.00 | -$250 (100% loss) |

Notice the leverage effect. A 15% move in the stock ($100 to $115) generates a 200% return on your call option. But if the stock stays flat or drops, you lose your entire premium.

Call Buyer Profit = (Stock Price at Expiration − Strike Price − Premium Paid) × 100Pro Tip

The Breakeven Point

Your breakeven point on a long call is the strike price plus the premium paid. The stock must rise above this level by expiration for you to profit.

Call Breakeven = Strike Price + Premium PaidUsing the example above, the breakeven is $105 + $2.50 = $107.50. The stock needs to rise 7.5% from $100 just to break even. This highlights an important reality: buying out-of-the-money calls requires a significant move to profit.

This is why many experienced traders buy in-the-money (ITM) calls or at-the-money (ATM) calls instead of cheap OTM options. ITM calls have higher delta, meaning they capture more of the stock's movement, and lower breakeven hurdles.

Selling Calls: Collecting Premium

Selling (writing) a call option puts you on the other side of the trade. You collect the premium upfront but accept the obligation to sell 100 shares at the strike price if the buyer exercises.

There are two types of call selling:

Covered calls — You own the underlying stock and sell calls against it. This is a conservative income strategy covered in depth in our covered calls guide. Your stock acts as collateral, limiting your risk.

Naked calls — You sell calls without owning the stock. This carries theoretically unlimited risk because the stock can rise indefinitely. Naked call selling is discussed in our naked calls and puts guide.

| Covered Call | Naked Call | |

|---|---|---|

| Stock ownership | Required | Not required |

| Max profit | Premium + (strike − stock price) | Premium collected |

| Max loss | Stock price − premium | Unlimited |

| Margin required | None (stock is collateral) | Substantial |

| Risk level | Moderate | Very high |

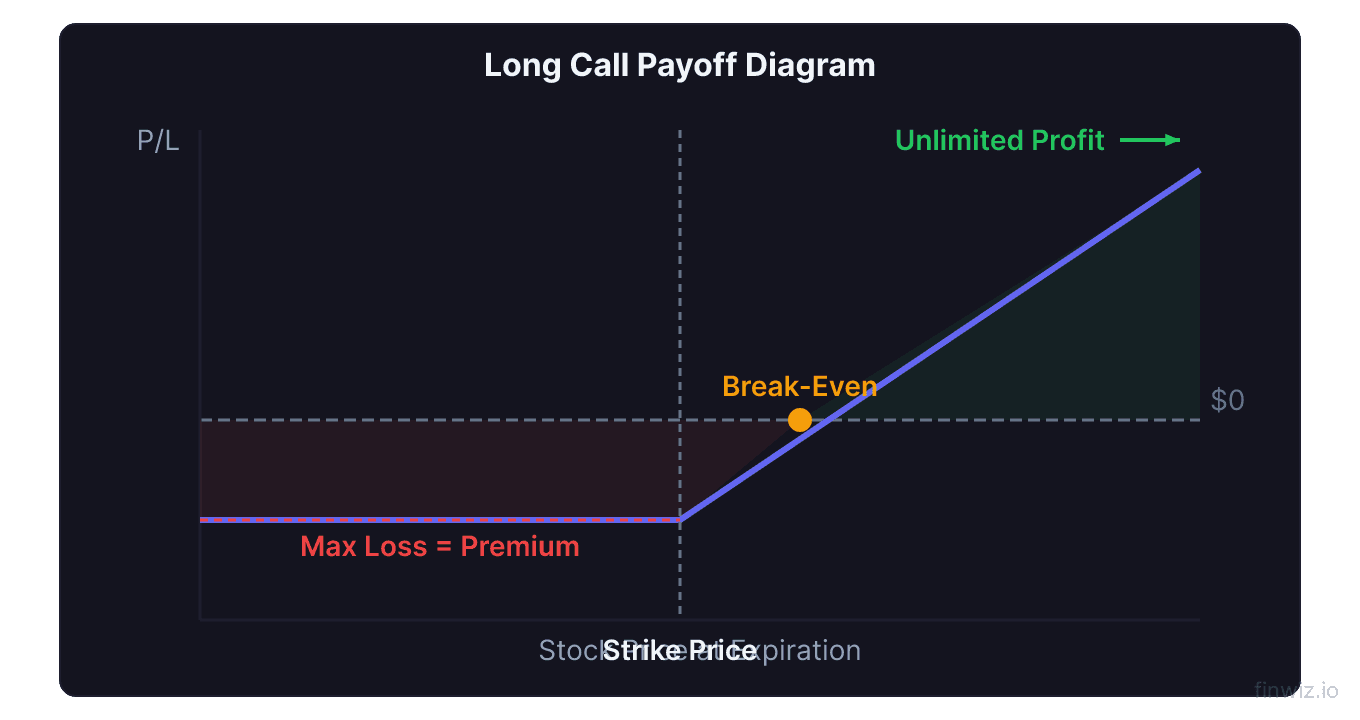

Call Option Payoff Diagram

The payoff diagram visually shows your profit and loss at various stock prices at expiration. For a long call, the diagram shows:

- A flat line at the maximum loss (premium paid) for all stock prices below the strike

- A breakeven point where the line crosses zero at strike price + premium

- An upward-sloping line showing increasing profit as the stock rises above breakeven

For a long call purchased at a $100 strike for $3.00:

| Stock Price | Payoff | Net P/L |

|---|---|---|

| $90 | $0 | -$300 |

| $95 | $0 | -$300 |

| $100 | $0 | -$300 |

| $103 | $3 | $0 (breakeven) |

| $110 | $10 | +$700 |

| $120 | $20 | +$1,700 |

For a short call sold at a $100 strike for $3.00, the diagram is the mirror image. Profit is capped at $300 (the premium), and losses grow as the stock rises above $103.

When to Buy Call Options

Not every bullish outlook warrants buying a call. The best conditions for buying calls include:

Strong directional conviction. You believe the stock will move up significantly, not just a few percent. The move needs to exceed your breakeven to profit.

Defined timeframe. You expect the move to happen before expiration. Time works against call buyers because of theta decay. Every day that passes without a move costs you money.

Low to moderate implied volatility. When implied volatility is low, options are cheaper. Buying calls in a low-IV environment means you pay less premium and may benefit from a subsequent IV expansion.

Upcoming catalyst. Earnings announcements, FDA decisions, product launches, or other binary events can drive the sharp, quick moves that call buyers need. However, be aware of IV crush — the sharp drop in implied volatility after the event passes.

Pro Tip

Real-World Example: Buying a Call Before Earnings

Let us walk through a realistic trade. Company ABC reports earnings in two weeks. The stock trades at $150, and you are bullish.

Trade setup:

- Buy 1 ABC $155 call, 14 DTE, for $4.00

- Total cost: $400

- Breakeven: $159.00

Scenario 1: Earnings beat, stock jumps to $170. The call is worth $15.00 at expiration. Profit: ($15 − $4) × 100 = $1,100 (275% return).

Scenario 2: Earnings miss, stock drops to $140. The call expires worthless. Loss: $400 (100% of premium).

Scenario 3: Stock rises modestly to $157. The call is worth $2.00 at expiration. Loss: ($2 − $4) × 100 = -$200 (50% loss). Even though the stock went up 4.7%, you still lost money because the move was not large enough to overcome the premium paid.

This third scenario illustrates why direction alone is not enough when buying options. You need the right magnitude and timing.

Choosing the Right Strike Price

Strike selection is one of the most important decisions in call buying. Here is how different strikes compare:

| Strike Type | Delta | Cost | Breakeven Distance | Win Rate |

|---|---|---|---|---|

| Deep ITM ($90 strike, stock at $100) | 0.85-0.95 | High | Small | High |

| ATM ($100 strike) | 0.45-0.55 | Moderate | Moderate | Moderate |

| OTM ($110 strike) | 0.15-0.30 | Low | Large | Low |

| Far OTM ($120 strike) | 0.05-0.10 | Very low | Very large | Very low |

Deep ITM calls behave like stock. They cost more but have a high probability of profit. Many traders use deep ITM LEAPS as stock replacement strategies.

ATM calls offer the best balance between cost, leverage, and probability. They have the highest gamma, meaning their delta changes quickly as the stock moves.

OTM calls are cheap lottery tickets. They offer maximum leverage but have a low probability of profit. Most OTM options expire worthless.

Managing Your Call Position

Buying a call is only half the trade. Managing it properly determines your overall success.

Take profits early. Do not wait for expiration hoping for more gains. If your call reaches 50-100% profit, consider closing it. A bird in the hand is worth two in the bush.

Cut losses at a threshold. Set a rule, such as closing the trade if the option loses 50% of its value. Do not let a losing call bleed to zero.

Roll forward. If you are still bullish but expiration is approaching, you can sell your current call and buy a later-dated call at the same or different strike. This extends your trade but costs additional premium.

Monitor the Greeks. Watch delta for directional exposure, theta for daily time decay, and vega for volatility risk. These numbers change constantly and affect your position value.

Call Options vs. Buying Stock

Understanding when calls are superior to stock, and when they are not, helps you choose the right instrument.

| Factor | Call Options | Stock |

|---|---|---|

| Capital required | Low (premium only) | Full share price |

| Leverage | High (control 100 shares) | None |

| Time limit | Yes (expiration) | No |

| Dividends | Not received | Received |

| Max loss | Premium paid | Full investment (to $0) |

| Voting rights | None | Yes |

Calls outperform stock when the move is large and quick. Stock outperforms calls when the move is small, slow, or takes longer than expected. If you are a long-term investor, stocks are almost always better. If you are a short-term trader with strong conviction, calls can amplify your returns.

Frequently Asked Questions

How much can I lose buying a call option?

Your maximum loss is the premium paid. If you buy a call for $3.00 per share ($300 per contract), the most you can lose is $300, regardless of how far the stock drops. This defined-risk feature is one of the primary advantages of buying calls over short selling puts.

What happens if my call option expires in the money?

If your call expires in the money, most brokers will auto-exercise it. This means you will buy 100 shares at the strike price. Make sure you have enough buying power in your account to cover the stock purchase, or sell the call before expiration to capture the profit without taking delivery.

Should I exercise my call or sell it?

In almost all cases, sell the call rather than exercising it. When you exercise, you only capture the intrinsic value. When you sell, you capture both intrinsic and any remaining extrinsic value. The only common exception is when you want to own the shares for the long term and the option has very little extrinsic value remaining.

Can I sell my call option before expiration?

Yes. You can sell any option you own at any time during market hours before expiration. Most options traders close their positions before expiration rather than exercising. Liquidity is generally best for ATM options with significant open interest and tight bid-ask spreads.

What is the difference between American and European style options?

American-style options can be exercised at any time before expiration. Most stock options are American-style. European-style options can only be exercised at expiration. Most index options (like SPX) are European-style. This distinction matters primarily for sellers who face early assignment risk on American-style options.

Disclaimer

This is educational content, not financial advice. Trading involves risk, and you should consult a qualified financial advisor before making any investment decisions. Past performance does not guarantee future results.

Related Articles

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.