Market Makers: Who They Are & How They Influence Prices

⚡ Key Takeaways

- Market makers are firms that continuously provide buy and sell quotes for securities, creating liquidity for other traders

- They profit primarily from the bid-ask spread, buying at the bid and selling at the ask

- Market makers take on inventory risk by holding shares and must manage this risk through hedging and position limits

- High-frequency trading (HFT) firms now dominate market making, using speed advantages to capture tiny spreads at massive volume

- Without market makers, bid-ask spreads would be wider, execution would be slower, and markets would be less efficient

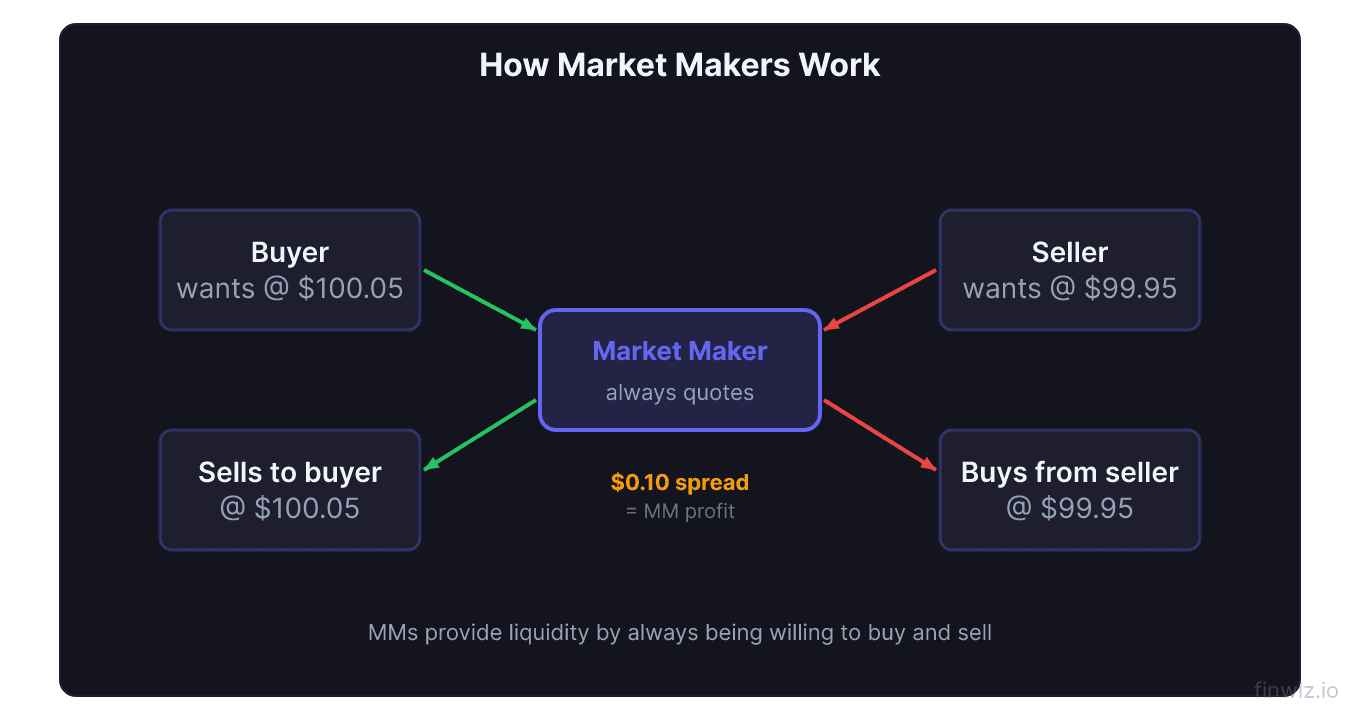

What Is a Market Maker?

A market maker is a firm or individual that stands ready to buy and sell a particular security at publicly quoted prices throughout the trading day. By continuously providing both a bid price (the price at which they will buy) and an ask price (the price at which they will sell), market makers create the liquidity that allows other traders to execute their orders quickly and efficiently.

Think of a market maker as a middleman. When you want to buy a stock, you do not need to find another individual who wants to sell at that exact moment. The market maker is always there, willing to sell to you at the ask price. When you want to sell, the market maker is willing to buy from you at the bid price.

How Market Makers Profit

The Spread

The primary source of profit for market makers is the bid-ask spread. By buying at the bid and selling at the ask, they capture the difference.

Gross Profit per Share = Ask Price - Bid PriceTwo cents per share may seem trivial, but market makers trade millions of shares per day. At $0.02 per share on 10 million shares, the daily gross profit is $200,000.

Volume Over Margin

Market making is a high-volume, low-margin business. The profit on each trade is tiny, but the number of trades is enormous. This model requires sophisticated technology, fast execution, and careful risk management.

Rebates

Exchanges pay market makers rebates for providing liquidity (posting limit orders that other traders fill against). These rebates supplement the spread revenue and incentivize market makers to maintain tight quotes.

The Role of Market Makers in the Market

Providing Liquidity

Without market makers, traders would have to wait for a natural counterparty to appear before executing their orders. This would result in wider spreads, slower execution, and more volatile prices. Market makers smooth out the trading process by always being available.

Price Discovery

By continuously adjusting their bid and ask prices based on supply, demand, and new information, market makers contribute to price discovery, the process by which the market determines fair value for securities.

Absorbing Imbalances

When there is a sudden surge in buying or selling, market makers absorb the imbalance by taking the other side of the trade. During a sell-off, market makers buy shares from panicking sellers, providing a floor (albeit a temporary one). During a buying frenzy, they sell shares to eager buyers.

This role comes with significant inventory risk. If a market maker accumulates a large long position during a sell-off and the stock continues to fall, they incur losses.

Pro Tip

Types of Market Makers

Designated Market Makers (DMMs)

On the NYSE, Designated Market Makers are assigned to specific stocks and have both the obligation to maintain orderly markets and special privileges to see order flow. They are the successors to the traditional specialist system.

Electronic Market Makers

Most modern market making is done by electronic firms using algorithms. These firms simultaneously make markets in thousands of stocks, adjusting quotes hundreds of times per second.

Wholesale Market Makers

Wholesale market makers (also called internalizers) handle retail order flow. When your broker routes your order to a wholesale market maker rather than a public exchange, the market maker fills your order internally, often at a slightly better price than the public bid/ask. This is the basis of payment for order flow (PFOF).

High-Frequency Trading and Market Making

High-frequency trading (HFT) firms have transformed market making. Using co-located servers positioned physically close to exchange data centers, these firms can process information and adjust quotes in microseconds.

How HFT Market Makers Operate

- They continuously monitor order flow and price changes across all exchanges

- They adjust their bids and asks thousands of times per second

- They use statistical models to predict short-term price movements

- They maintain tiny inventories, rarely holding positions for more than seconds

- They profit from millions of small spread captures

Benefits of HFT Market Making

- Tighter spreads: Competition among HFT firms has driven spreads to historic lows

- Faster execution: Orders fill in milliseconds

- Greater liquidity: More market makers mean more shares available at each price level

Concerns About HFT Market Making

- Speed advantage: HFT firms can react to information before human traders

- Phantom liquidity: Quotes can be cancelled in microseconds, making the apparent liquidity illusory

- Flash crashes: HFT algorithms can withdraw liquidity simultaneously, exacerbating crashes

- Latency arbitrage: HFT firms can exploit tiny time delays between exchanges

Market Maker Obligations

Market makers on regulated exchanges have specific obligations:

- Continuous quoting: They must maintain bid and ask quotes during market hours

- Size obligations: They must offer to trade a minimum number of shares at their quoted prices

- Spread limits: Some markets set maximum allowable spreads

- Orderly market: They must help maintain orderly trading, especially during volatility

In exchange for these obligations, market makers receive privileges such as reduced fees, rebates, and in some cases, early access to order information.

How Market Makers Affect Your Trading

Stop Loss Hunting

There is a persistent belief among retail traders that market makers "hunt" stop losses. While market makers do see order flow and know where stops cluster, the mechanics are more nuanced than deliberate hunting.

When many stops cluster at a specific level, the eventual triggering of those stops creates a cascade of sell orders. This can temporarily push the price through the level before it recovers. Whether this is intentional manipulation or natural market dynamics is debated.

Order Routing

Your broker's decision about where to route your order affects your execution quality. Orders routed to wholesale market makers may receive price improvement but contribute to dark pool volumes rather than public price discovery.

Frequently Asked Questions

Do market makers control stock prices?

No. Market makers influence short-term price movements by adjusting their quotes, but they do not control prices. The stock price is determined by the aggregate supply and demand from all market participants. Market makers facilitate this process, they do not dictate it.

Can retail traders be market makers?

Technically, some retail traders employ market-making-like strategies (posting limit orders on both sides of the spread). However, they lack the speed, technology, and rebate advantages of professional market makers. True market making requires institutional-level infrastructure.

Why did my stop loss get hit before the stock reversed?

This often occurs when stop orders cluster at obvious support levels. When the price reaches that level, the triggering of stops creates a brief burst of selling that pushes the price below support. Once the stops are cleared, buying interest returns. This is a natural consequence of clustered orders, not necessarily manipulation.

How do market makers handle earnings announcements?

During earnings announcements, market makers typically widen their spreads significantly to account for the increased uncertainty. They may also reduce the number of shares they are willing to trade at each price level. This is why bid-ask spreads are often much wider during volatile events.

Are market makers necessary for the market to function?

Market makers are not strictly necessary, but they significantly improve market quality. Without them, spreads would be wider, execution would be slower, and price volatility would be higher. They serve as the lubricant that keeps the market machine running smoothly.

Disclaimer

This is educational content, not financial advice. Trading involves risk, and you should consult a qualified financial advisor before making any investment decisions. Past performance does not guarantee future results.

Market Makers and Order Types

How Market Makers Interact with Different Orders

Understanding how market makers interact with your orders helps you choose the right order type:

Market orders: Market makers immediately fill your order at their quoted bid (for sells) or ask (for buys). In liquid stocks, this works smoothly. In illiquid stocks, your order may consume the available quotes and fill across multiple price levels.

Limit orders: Your limit order enters the order book and may be filled by a market maker or another trader. If your limit is at a price inside the current spread (better than the bid for buys, better than the ask for sells), you are effectively competing with the market maker for fills.

Stop orders: Market makers can see where stop orders cluster (at round numbers, obvious support levels). When the price reaches these levels, the triggered stops create a burst of orders that market makers absorb. This dynamic is why prices sometimes briefly spike through support levels before reversing.

Market Making Economics in Modern Markets

The economics of market making have changed dramatically over the past two decades:

- Decimalization (2001): Reduced the minimum spread from $0.125 to $0.01, compressing market maker profits by 90%+

- Electronic trading: Reduced the need for human specialists, shifting to algorithmic market making

- HFT competition: Multiple HFT firms compete to make markets, driving spreads to historical lows

- Payment for order flow: Created a new revenue stream for market makers willing to pay for retail order flow

These changes have made markets more efficient and cheaper for investors (tighter spreads) while making traditional market making less profitable. The survivors are firms with the fastest technology and most sophisticated risk management systems.

Impact on Individual Traders

For individual traders, the practical impact of modern market making is largely positive:

- Spreads are at historical lows, reducing your transaction costs

- Execution speed is near-instantaneous, allowing fast entries and exits

- Liquidity is generally abundant during regular market hours

However, during extreme volatility events, HFT market makers can withdraw liquidity simultaneously, causing spreads to widen dramatically and fills to deteriorate. This was seen during the 2010 Flash Crash and subsequent volatile events. Keep this risk in mind when trading during high-volatility periods and consider using limit orders rather than market orders.

Related Articles

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.