How the IPO Process Works: From Filing to First Trade

⚡ Key Takeaways

- An Initial Public Offering (IPO) is the process by which a private company sells shares to the public for the first time, typically taking 6 to 12 months from start to first trade.

- The IPO process involves hiring underwriters (investment banks), filing an S-1 registration statement with the SEC, completing a roadshow, pricing shares, and finally trading on a public exchange.

- The lock-up period (typically 90-180 days) prevents insiders from selling shares immediately after the IPO, and its expiry often creates significant selling pressure.

- IPO pricing is a negotiation between the company, its underwriters, and institutional investors — retail investors rarely receive shares at the IPO price.

- Most IPOs experience a "quiet period" during which the underwriting analysts cannot publish research, creating an information gap for retail investors.

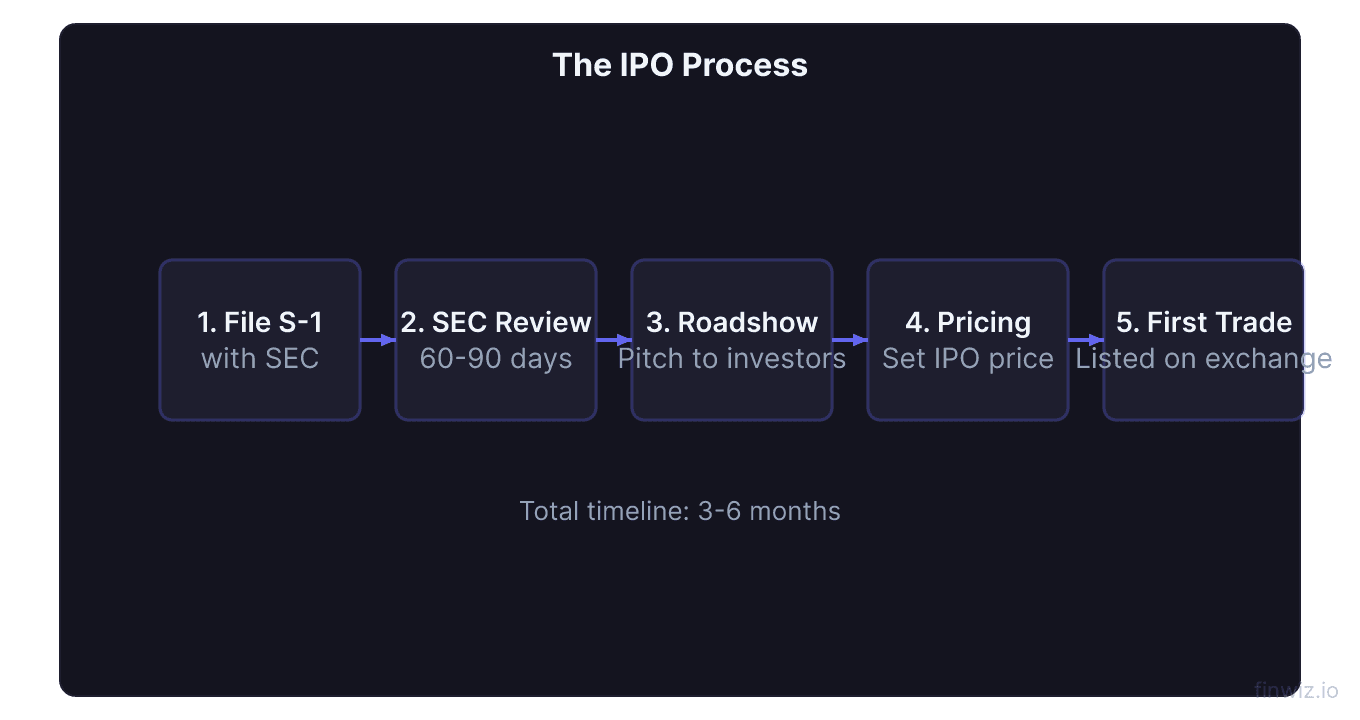

What Is the IPO Process?

The IPO process is the multi-step journey a private company undertakes to list its shares on a public stock exchange like the NYSE or NASDAQ. From start to finish, this process typically spans 6 to 12 months and involves investment banks, securities lawyers, the SEC, institutional investors, and the company's leadership team.

For investors and traders, understanding the IPO timeline matters because each phase creates distinct opportunities and risks. Knowing when an S-1 is filed, when the roadshow begins, and when the lock-up expires can help you make better-informed decisions about whether and when to participate in a newly public stock.

The IPO remains the most common path for large private companies to access public capital markets, though alternatives like direct listings and SPACs have gained popularity. In a traditional IPO, the company works with investment banks (underwriters) who guarantee a minimum capital raise in exchange for fees typically ranging from 3% to 7% of the total offering.

Phase 1: Selecting Underwriters

The first major step is choosing one or more investment banks to serve as underwriters. The company evaluates banks based on their industry expertise, distribution network, research capabilities, and past IPO track records.

Lead vs. Co-Underwriters

The lead underwriter (also called the bookrunner) manages the entire process. They coordinate the S-1 drafting, organize the roadshow, build the order book, and ultimately set the IPO price. Companies often select two to four co-underwriters to broaden the distribution network and provide additional analyst coverage after the IPO.

Top-tier banks like Goldman Sachs, Morgan Stanley, and JPMorgan command premium fees but bring extensive institutional client networks. Smaller companies may work with mid-market banks like Jefferies or Piper Sandler.

The Engagement Letter

The underwriting relationship is formalized through an engagement letter that outlines the banks' roles, fee structure, and the type of underwriting agreement (firm commitment vs. best efforts). In a firm commitment, the underwriter purchases all shares and resells them — taking on the risk. In a best efforts agreement, the underwriter simply tries to sell as many shares as possible without guaranteeing the full amount.

Pro Tip

Phase 2: The S-1 Filing

The S-1 registration statement is the comprehensive disclosure document filed with the SEC. This is the single most important document in the entire IPO process.

What the S-1 Contains

The S-1 includes the company's full financial history (typically three years of audited financials), business model description, risk factors, management team biographies, compensation details, use of proceeds, and ownership structure. Key sections investors should focus on:

- Business overview — how the company makes money

- Risk factors — management's own assessment of what could go wrong

- Financial statements — revenue growth, profitability, cash flow

- Use of proceeds — whether the money goes to growth or paying off existing investors

- Dilution — how much your ownership gets reduced

Initial vs. Amended S-1

The first filing is called the initial S-1 and often uses a placeholder price range (e.g., "$X to $Y per share"). The company then files one or more amended S-1s (S-1/A) as the SEC reviews the document and requests changes. The final amendment includes the actual price range.

You can track all S-1 filings on the SEC's EDGAR database at sec.gov/cgi-bin/browse-edgar. Search by company name to find their filing history.

Phase 3: SEC Review Period

After the S-1 is filed, the SEC's Division of Corporation Finance reviews the document. This review typically takes 30 to 60 days but can extend longer for complex offerings.

Comment Letters

The SEC sends comment letters requesting clarification, additional disclosure, or changes to the S-1. These letters are publicly available on EDGAR approximately 20 business days after the company responds. Common areas where the SEC requests changes include:

- Revenue recognition policies

- Non-GAAP financial metrics

- Related-party transactions

- Executive compensation disclosure

- Risk factor specificity

The company responds to each round of comments, and there may be two to four rounds of back-and-forth before the SEC is satisfied.

Declaring the S-1 Effective

Once all comments are resolved, the SEC declares the registration statement effective, meaning the company is cleared to proceed with the offering. This does not mean the SEC endorses the investment — it simply confirms that the disclosure meets regulatory requirements.

Phase 4: The Roadshow

The roadshow is a one-to-two-week marketing blitz where the company's CEO, CFO, and lead underwriters present to institutional investors across major financial centers. The roadshow typically visits New York, Boston, San Francisco, London, and other cities with major institutional investor bases.

What Happens During the Roadshow

Management presents a polished slide deck covering the company's growth story, competitive advantages, financial projections, and vision. Institutional investors — mutual funds, hedge funds, pension funds — ask questions and decide whether they want to participate in the IPO and at what price.

The underwriters gauge investor demand at various price points. This process is called building the book. Strong demand allows the company to price at the higher end of its range (or even above it), while weak demand forces a lower price or a reduced offering size.

The Retail Investor Gap

Retail investors are largely excluded from the roadshow process. Some brokerages (like Fidelity and Schwab) occasionally offer IPO access to qualified clients, but most individual investors cannot buy shares at the IPO price. They must wait until shares begin trading on the open market, often at a premium.

Pro Tip

Phase 5: Pricing the IPO

IPO pricing occurs the evening before the first day of trading. The lead underwriter, in consultation with the company, sets the final offering price based on roadshow demand.

How the Price Is Set

The underwriter analyzes the order book — a list of institutional investors and how many shares they want at various prices. The goal is to set a price that:

- Raises the desired amount of capital for the company

- Creates enough demand for a modest first-day "pop" (typically 10-20%)

- Avoids pricing so low that the company leaves money on the table

- Avoids pricing so high that shares trade below the IPO price

Price Range Revisions

The initial S-1 includes a preliminary price range (e.g., $18-$21 per share). During the roadshow, this range can be revised upward or downward based on demand. A range increase is a bullish signal — it means institutional demand exceeded expectations. A range decrease is bearish — demand was weaker than anticipated.

For example, when Snowflake went public in September 2020, the initial range was $75-$85. It was raised to $100-$110, and then priced at $120 — far above the original range. Shares opened at $245 on the first day of trading.

Allocation of Shares

After pricing, the underwriter allocates shares to institutional investors. This process is opaque and favors the underwriter's best clients. Large mutual funds and hedge funds with long-standing relationships receive the bulk of the allocation.

Phase 6: First Day of Trading

The first trade occurs when the exchange's designated market maker matches buy and sell orders and establishes an opening price. This opening price is typically higher than the IPO price — the difference is known as the first-day pop.

Opening Cross vs. IPO Price

The opening cross is the process by which the exchange determines the first publicly traded price. On the NYSE, the designated market maker (DMM) manages this process. On NASDAQ, it is handled electronically. The opening price reflects the balance of buy and sell orders from both institutional allocations and retail demand.

In 2020 and 2021, many high-profile IPOs saw first-day pops exceeding 50% — Airbnb doubled on its first day, opening at $146 versus its $68 IPO price.

First-Day Trading Dynamics

First-day trading is often characterized by extreme volatility, wide bid-ask spreads, and high volume. Without historical price data, traders have no support/resistance levels, no moving averages, and limited technical reference points.

IPO First-Day Return = (Closing Price - IPO Price) / IPO Price x 100Phase 7: The Quiet Period

The quiet period begins after the S-1 is filed and extends for 25 days after the first day of trading (under SEC rules). During this window, the underwriting banks' research analysts are prohibited from publishing research reports or making public recommendations about the stock.

Why the Quiet Period Matters

The expiration of the quiet period is significant because it triggers a flood of analyst initiations — typically with "Buy" ratings, since the underwriting analysts are inherently conflicted. This wave of positive coverage often creates a short-term price bump.

Traders who understand this dynamic can position ahead of the quiet period expiration. However, be aware that the expected "bump" is sometimes priced in advance.

Phase 8: Lock-Up Expiry

The lock-up period is a contractual agreement (not an SEC regulation) that prevents company insiders — founders, executives, early employees, and pre-IPO investors — from selling their shares for a specified period after the IPO, typically 90 to 180 days.

Why Lock-Up Expiry Creates Selling Pressure

When the lock-up expires, a massive supply of previously restricted shares becomes eligible for sale. In many cases, the number of shares unlocked exceeds the total number of shares sold in the IPO itself.

For example, if a company sold 20 million shares in its IPO but insiders hold 200 million shares, the lock-up expiry increases the potential float by 10x. Even if only a fraction of insiders sell, the impact on supply can be dramatic.

Historical Lock-Up Expiry Patterns

Studies show that stocks decline an average of 1-3% around lock-up expiry, with the effect more pronounced for:

- Companies that are unprofitable

- Stocks that have risen significantly since the IPO

- Companies with high insider ownership percentages

- Venture capital-backed companies (VCs often sell early)

The selling pressure typically begins a few days before the actual expiry date as short sellers anticipate the supply increase.

Pro Tip

The Complete IPO Timeline

Here is a consolidated timeline showing the typical duration of each phase:

| Phase | Duration | Key Activity |

|---|---|---|

| Underwriter selection | 1-3 months | Evaluate banks, sign engagement letter |

| S-1 preparation | 2-4 months | Draft financials, risk factors, business overview |

| SEC review | 1-2 months | Comment letters, amendments |

| Roadshow | 1-2 weeks | Management presents to institutional investors |

| Pricing | 1 day (evening) | Set final price, allocate shares |

| First trade | Next morning | Opening cross, public trading begins |

| Quiet period | 25 days post-IPO | No underwriter research published |

| Lock-up expiry | 90-180 days post-IPO | Insiders can begin selling |

How to Evaluate an IPO as an Investor

Read the S-1 Thoroughly

Focus on the risk factors, revenue trends, customer concentration, and use of proceeds. If most proceeds are going to pay off existing investors rather than fund growth, that is a red flag.

Assess the Underwriter Quality

Top-tier underwriters with firm commitment agreements suggest institutional confidence. Multiple co-underwriters with strong distribution networks are a positive sign.

Watch the Price Range Revisions

An upward revision in the IPO price range signals strong institutional demand. A downward revision is a warning sign.

Wait for the Lock-Up to Expire

Many experienced investors prefer to wait until after the lock-up expiry to buy shares. This eliminates the overhang of potential insider selling and allows for more price discovery based on public-market fundamentals.

FAQ

How long does the IPO process take from start to finish?

The typical IPO process takes 6 to 12 months from selecting underwriters to the first day of trading. However, preparation (audit readiness, board composition, governance) often begins 1-2 years before the formal process kicks off.

Can retail investors buy shares at the IPO price?

In most cases, no. IPO shares are allocated almost exclusively to institutional investors. Some brokerages (Fidelity, Schwab, TD Ameritrade) offer limited IPO access to clients who meet certain account size and trading history requirements.

What is the difference between an IPO and a direct listing?

In a traditional IPO, the company issues new shares and raises capital with the help of underwriters. In a direct listing, no new shares are created — existing shareholders simply begin selling their shares on the exchange. There are no underwriters, no roadshow, and no lock-up period.

Why do IPOs often pop on the first day?

The first-day pop occurs because underwriters intentionally price the IPO below what they believe the market will pay. This creates goodwill with institutional clients who receive the allocation (they get an instant profit) and generates positive headlines for the company. Critics argue this "underpricing" costs the company billions in capital it could have raised.

Should I buy an IPO on the first day?

Most data suggests that buying on the first day at the inflated opening price leads to below-market returns over the following 3-12 months. The average IPO underperforms the broader market after the initial pop. Consider waiting for a few earnings reports and the lock-up expiry before establishing a position.

Disclaimer

This is educational content, not financial advice. Trading involves risk, and you should consult a qualified financial advisor before making any investment decisions. Past performance does not guarantee future results.

Related Articles

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.