Margin Account vs Cash Account: Which Should You Use?

⚡ Key Takeaways

- A cash account requires full payment for every trade, while a margin account lets you borrow up to 50% of a purchase from your broker

- Margin accounts unlock short selling, options strategies, and same-day settlement but expose you to margin calls and amplified losses

- The Pattern Day Trader (PDT) rule only applies to margin accounts and requires a minimum equity of $25,000 to make four or more day trades in five business days

- Regulation T sets the initial margin requirement at 50%, meaning you must fund at least half of any leveraged position

- Cash accounts avoid PDT restrictions entirely but limit you to settled funds, creating a T+1 settlement waiting period between trades

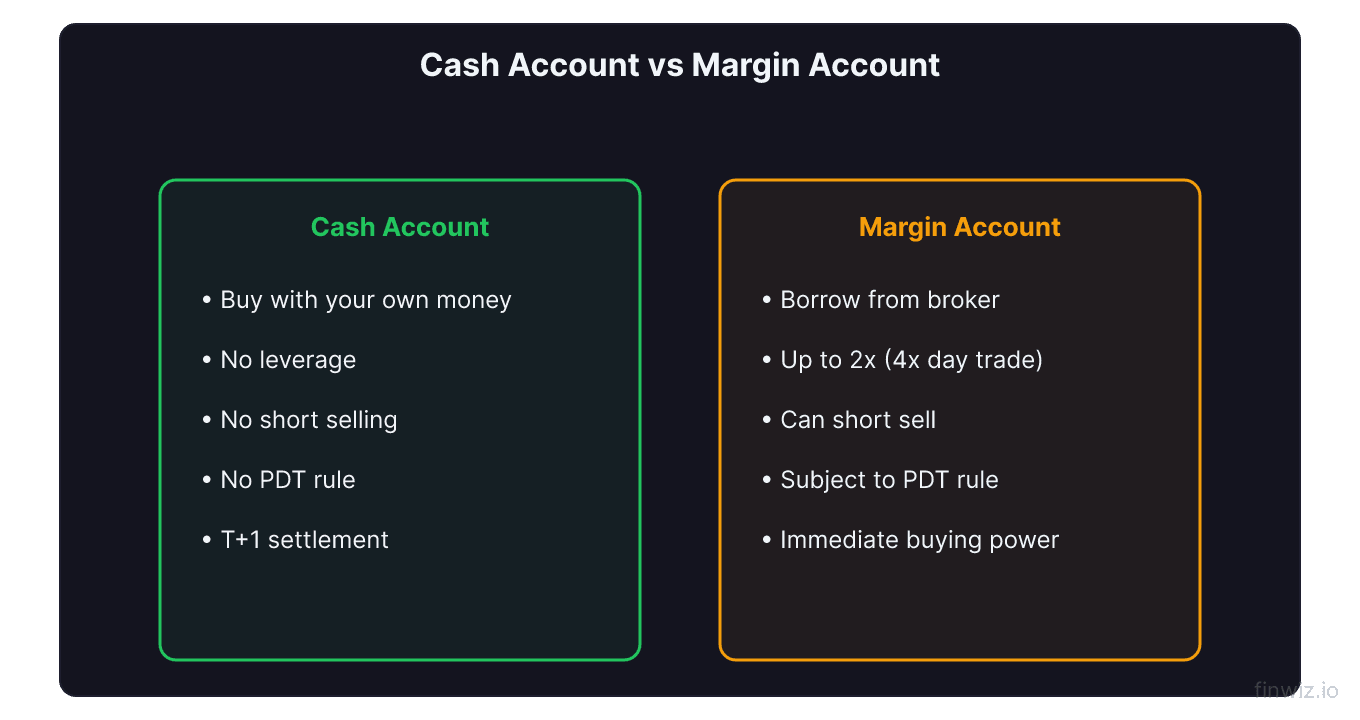

What Is a Cash Account?

A cash account is the most basic type of brokerage account. Every purchase must be fully funded with settled cash. If you have $10,000 in your account, you can buy up to $10,000 worth of stock. No borrowing. No leverage.

When you sell a position, the proceeds must settle before you can use them again. Under the current T+1 settlement cycle, this means waiting one business day after selling before those funds are available for a new purchase. Violating this creates a good faith violation, and accumulating three within a 12-month period can restrict your account to settled-cash-only trades for 90 days.

Cash accounts are straightforward, but they come with limitations. You cannot short sell stocks, and certain options strategies that require margin are off-limits. However, you are never at risk of a margin call, and the PDT rule does not apply.

What Is a Margin Account?

A margin account allows you to borrow money from your broker using your existing holdings as collateral. Under Regulation T, you can borrow up to 50% of the purchase price of a new position. This means $10,000 in cash gives you up to $20,000 in buying power.

Margin accounts also provide immediate access to sale proceeds without waiting for settlement. This is critical for active traders who need to enter and exit positions throughout the day.

The tradeoff is risk. When you borrow on margin, losses are amplified just like gains. A 10% decline on a fully margined position translates to a 20% hit on your equity. If your account equity drops below the maintenance margin (typically 25-30%, though many brokers set it higher), you receive a margin call requiring you to deposit additional funds or liquidate positions.

Buying Power = Account Equity / Initial Margin RequirementKey Differences at a Glance

| Feature | Cash Account | Margin Account |

|---|---|---|

| Leverage | None (1:1) | Up to 2:1 (4:1 intraday for PDT) |

| Short selling | Not allowed | Allowed |

| Settlement | Must wait T+1 | Immediate access |

| Margin calls | Never | Yes, if equity drops below maintenance |

| PDT rule | Does not apply | Applies if 4+ day trades in 5 days |

| Interest charges | None | Charged on borrowed funds |

| Options | Limited strategies | Full access |

PDT Rule and Account Type

The Pattern Day Trader rule is one of the biggest reasons account type matters for active traders. Under FINRA rules, if you execute four or more day trades within five rolling business days in a margin account, you are flagged as a pattern day trader and must maintain at least $25,000 in account equity.

In a cash account, PDT does not apply. You can technically day trade as often as your settled cash allows. The catch is settlement. After each sale, you wait one business day before reusing those funds. This naturally limits the frequency of trades.

Some traders with smaller accounts deliberately use cash accounts to sidestep the PDT restriction while still making occasional day trades. The constraint is capital efficiency, not regulation.

Pro Tip

Margin Interest and Borrowing Costs

Borrowing on margin is not free. Your broker charges margin interest on the borrowed amount, typically ranging from 5% to 13% annually depending on the broker and the loan size. This interest accrues daily and is charged monthly.

For swing trades held days to weeks, margin interest is usually negligible. For positions held months, it becomes a meaningful drag on returns. If you borrow $25,000 at 8% annually and hold for three months, you owe roughly $500 in interest regardless of whether the trade was profitable.

Short selling adds another layer of cost. Beyond margin interest, you pay a stock borrow fee that varies based on how difficult the shares are to locate. Easy-to-borrow blue chips like AAPL or MSFT might cost under 1% annually. Hard-to-borrow small caps can exceed 50%.

When to Use Each Account Type

Choose a cash account if you are a beginning investor, you have less than $25,000 and want to avoid PDT issues, or you prefer zero risk of margin calls. Long-term investors buying and holding ETFs or stocks in a diversified portfolio rarely need margin.

Choose a margin account if you plan to day trade, short sell, or use advanced options strategies. Active traders who execute short selling or need immediate settlement to cycle through positions during the day need margin.

Many brokers let you open a margin account without ever using the margin. This gives you the settlement benefits and options access while you choose whether to employ leverage on any given trade.

FAQ

Can I switch from a cash account to a margin account?

Yes. Most brokers allow you to upgrade by completing a margin agreement and meeting minimum equity requirements (typically $2,000). The process usually takes one to three business days. Downgrading from margin to cash is also possible but may require closing any existing margin positions first.

What happens if I cannot meet a margin call?

Your broker will liquidate positions in your account to bring equity above the maintenance requirement. You do not get to choose which positions are sold. Brokers typically give you two to five business days to deposit funds, but they reserve the right to sell immediately without notice. This forced selling often happens at the worst prices during volatile markets.

Does margin interest affect my taxes?

Margin interest is potentially tax-deductible as an investment expense, but only up to the amount of your net investment income. You cannot use margin interest deductions to create or increase a net loss from investments. Consult a tax professional for your specific situation, as the rules around investment interest deductions involve several limitations under the Tax Cuts and Jobs Act.

Related Articles

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.