Margin Account vs Cash Account: Key Differences Explained

⚡ Key Takeaways

- A cash account requires you to pay in full for every trade, while a margin account lets you borrow up to 50% of a purchase price from your broker under Regulation T

- Margin accounts provide 2:1 buying power (4:1 intraday for pattern day traders), meaning $25,000 in cash can control up to $50,000 in securities

- The Pattern Day Trader rule applies only to margin accounts, requiring $25,000 minimum equity for four or more day trades in five business days

- Cash accounts eliminate margin call risk entirely but impose T+1 settlement delays that limit how quickly you can reuse proceeds

- Margin interest typically ranges from 5% to 13% annually and accrues daily on borrowed balances, creating an ongoing cost that cash accounts never incur

Margin Account vs Cash Account: What Is the Difference?

The difference between a margin account and a cash account comes down to borrowing. A cash account requires you to pay the full purchase price of every security with settled funds. A margin account allows you to borrow money from your broker, using your existing holdings as collateral, to purchase additional securities beyond what your cash balance would normally allow. This single distinction creates a cascade of differences in buying power, trading flexibility, costs, and regulatory treatment.

For long-term investors who buy and hold index funds, a cash account is often sufficient. For active traders who need to short sell, execute rapid round trips, or deploy advanced options strategies, a margin account is a practical necessity. Choosing the right account type depends on your trading frequency, account size, and tolerance for leverage risk.

What Is a Cash Account?

A cash account is the simplest type of brokerage account. You deposit funds, and every purchase must be paid for entirely with settled cash. If your account holds $10,000, you can buy exactly $10,000 worth of stock. There is no borrowing, no leverage, and no debt to your broker.

When you sell a position in a cash account, the proceeds enter a T+1 settlement period. Under current SEC rules, equity trades settle one business day after execution. Until settlement completes, those funds are unavailable for new purchases. Attempting to buy securities with unsettled proceeds creates a good faith violation. Accumulating three good faith violations within 12 months restricts your account to settled-cash-only trading for 90 days.

Cash accounts do have clear advantages. You face zero risk of margin calls, you pay no interest on borrowed funds, and the PDT rule does not apply regardless of how frequently you trade. For investors focused on building wealth through buy-and-hold strategies, these limitations are rarely meaningful.

What Is a Margin Account?

A margin account allows you to borrow against your portfolio. Under Regulation T, your broker can lend you up to 50% of the purchase price of marginable securities. This means a $25,000 cash deposit provides $50,000 in buying power for overnight positions.

Beyond leverage, margin accounts offer practical benefits that matter for active trading. Sale proceeds are available immediately without waiting for settlement. You can short sell stocks, and you gain access to the full range of options strategies, including spreads and uncovered positions that require margin.

The tradeoff is amplified risk. If you use $50,000 in buying power on a $25,000 deposit and the position drops 10%, you lose $5,000 — a 20% hit to your actual equity. If your equity falls below the maintenance margin requirement (typically 25% at most brokers, though many set it at 30% or higher), you receive a margin call demanding additional deposits or forced liquidation of your positions.

Buying Power = Account Equity / Initial Margin RequirementKey Differences: Margin Account vs Cash Account

| Feature | Cash Account | Margin Account |

|---|---|---|

| Leverage | None (1:1 buying power) | Up to 2:1 overnight, 4:1 intraday for PDT |

| Short selling | Not allowed | Allowed |

| Settlement | Must wait T+1 for proceeds | Immediate access to sale proceeds |

| Margin calls | Never | Yes, if equity drops below maintenance margin |

| PDT rule | Does not apply | Applies with 4+ day trades in 5 days |

| Interest charges | None | 5-13% annually on borrowed funds |

| Options access | Limited to basic strategies | Full access including spreads |

| Minimum to open | Varies ($0 at some brokers) | Typically $2,000 |

Buying Power: 2:1 vs 1:1

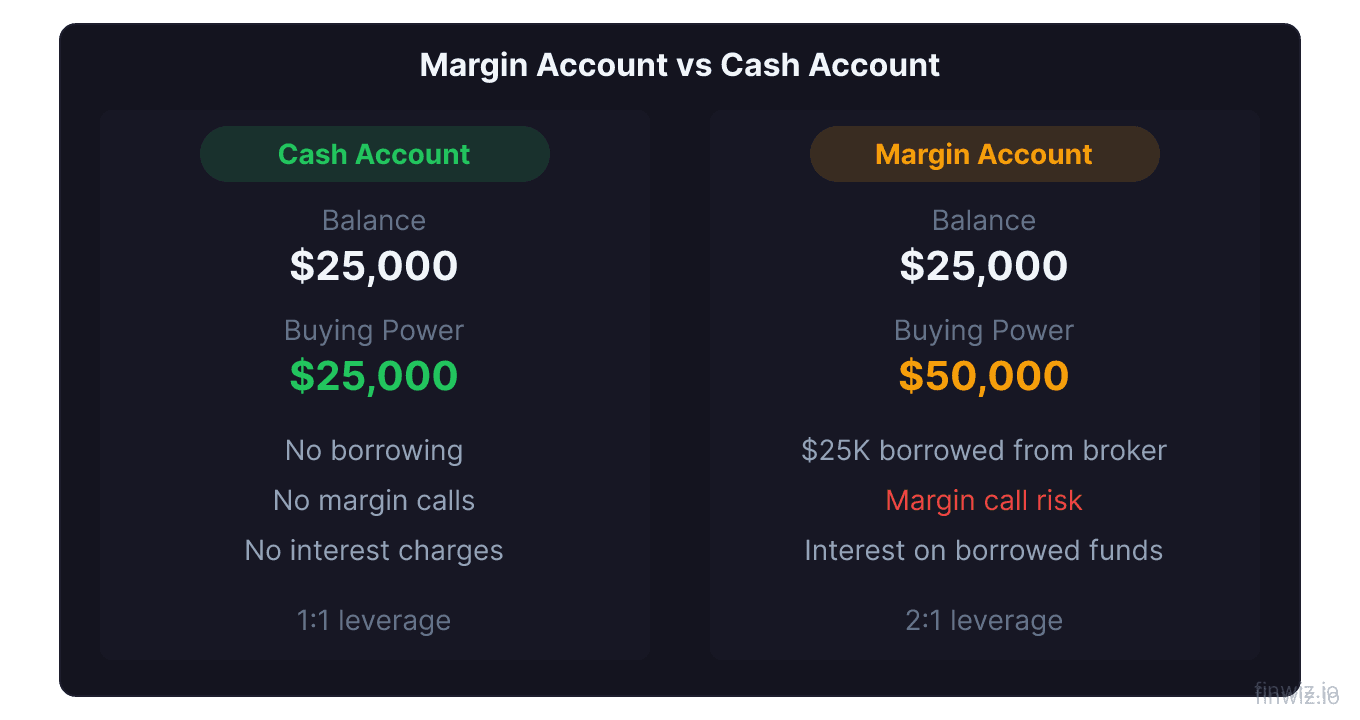

The buying power difference is the most tangible distinction between these account types. Consider an investor with $25,000 in cash.

In a cash account: You can purchase up to $25,000 worth of securities. That is the ceiling. After selling a position, you wait one business day before those funds become available again.

In a margin account: You can purchase up to $50,000 worth of securities for overnight positions (2:1 leverage). If you qualify as a pattern day trader with at least $25,000 in equity, your intraday buying power jumps to $100,000 (4:1 leverage), though all positions must be closed before the market closes to use this enhanced leverage.

This does not mean you should use all available margin. Leveraging your full buying power means a 50% decline in your positions would wipe out your entire equity in a 2:1 scenario. Experienced traders treat margin as a tool for occasional use, not a permanent multiplier. Solid risk management is especially critical when trading on margin.

Pro Tip

PDT Rule Implications for Each Account Type

The Pattern Day Trader rule is one of the most consequential differences between margin and cash accounts. Under FINRA rules, executing four or more day trades within five rolling business days in a margin account flags you as a pattern day trader. Once flagged, you must maintain a minimum equity balance of $25,000 at all times. Falling below that threshold restricts your account until you deposit additional funds or wait 90 days.

In a cash account, the PDT rule simply does not exist. You can make as many day trades as your settled cash allows. The natural constraint is settlement: after each sale, proceeds are locked for one business day. If you have $25,000 and divide it into five $5,000 positions, you can day trade one position per day and cycle through your capital over the week.

Some traders with less than $25,000 deliberately choose cash accounts to bypass PDT restrictions entirely. The tradeoff is reduced capital efficiency and the inability to short sell, but for traders who plan their entries the night before and execute selectively, a cash account can be surprisingly effective.

Interest and Costs

Borrowing on margin is not free. Your broker charges margin interest on any borrowed balance, calculated daily and billed monthly. Rates vary by broker and loan size, typically falling between 5% and 13% annually.

For short-term swing trades held a few days, interest costs are negligible. On a $10,000 borrowed balance at 8% annually, one week of interest is roughly $15. For positions held weeks or months, the cost compounds into a meaningful drag. That same $10,000 balance held for six months generates approximately $400 in interest charges, reducing your net return regardless of whether the trade profits.

Short selling adds a stock borrow fee on top of margin interest. Easily borrowed large caps like AAPL or MSFT carry borrow fees under 1% annually. Hard-to-borrow small caps with high short interest can carry fees exceeding 50% annually, making extended short positions extremely expensive.

Cash accounts incur none of these costs. Your only trading expense is the bid-ask spread and any commissions (now zero at most major brokers).

When to Use Each Account Type

Choose a cash account when:

- You are a buy-and-hold investor building a long-term portfolio

- Your account balance is under $25,000 and you want to avoid PDT restrictions

- You want zero risk of margin calls or forced liquidation

- You prefer simplicity with no borrowing costs

- You are new to trading and want guardrails against over-leveraging

Choose a margin account when:

- You actively day trade or swing trade and need immediate settlement

- You want the ability to short sell stocks

- You use multi-leg options strategies that require margin

- Your account exceeds $25,000 and you want maximum flexibility

- You want the option to use leverage selectively on high-conviction trades

Many investors maintain both: a cash account (or retirement account) for long-term holdings and a margin account for active trading. This separation keeps your long-term investments insulated from the risks of leveraged trading.

Frequently Asked Questions

Can I convert a cash account to a margin account?

Yes. Most brokers allow you to upgrade by completing a margin agreement and meeting the minimum equity requirement, typically $2,000. The process usually takes one to three business days. You can also downgrade a margin account to a cash account, though you must first close any existing margin positions and repay any borrowed balance.

What happens if I get a margin call?

Your broker notifies you that your account equity has fallen below the maintenance margin requirement. You typically have two to five business days to deposit additional funds or sell positions to restore compliance. If you fail to act, the broker will liquidate positions at their discretion, often at unfavorable prices during volatile markets. You do not get to choose which positions are sold.

Is margin interest tax deductible?

Margin interest is potentially deductible as an investment interest expense, but only up to the amount of your net investment income for the year. You cannot use it to create or increase a net investment loss. The deduction is claimed on IRS Form 4952. Consult a tax professional for your specific situation, as several limitations apply under current tax law.

Can I day trade in a cash account?

Yes. The PDT rule does not apply to cash accounts, so there is no minimum equity requirement for day trading. However, you are limited by settled funds. After selling a position, you must wait one business day (T+1) before reusing those proceeds. This effectively caps your daily trading frequency based on how much settled cash is available each morning.

Do all brokers offer both account types?

All major U.S. brokers offer both cash and margin accounts. Some brokers default new accounts to margin, while others start with cash and require an upgrade request. Brokers like Fidelity, Schwab, and Interactive Brokers allow you to choose during account setup. If you are unsure which type your account is, check your account settings or contact your broker directly.

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.