Treasury Bills vs Bonds: Maturity, Yield & How They Pay

⚡ Key Takeaways

- Treasury bills (T-bills) mature in 4 to 52 weeks and are sold at a discount to par, while Treasury bonds (T-bonds) mature in 20 to 30 years and pay semiannual coupon interest

- T-bills carry virtually no interest rate risk due to their short maturities, while T-bond prices can swing 20% or more when long-term rates shift by just one percentage point

- Both are backed by the full faith and credit of the U.S. government, making them effectively free of credit risk

- T-bill yields reflect short-term Federal Reserve policy, while T-bond yields reflect long-term inflation expectations, growth forecasts, and term premium — the relationship between the two defines the yield curve

- Interest from both T-bills and T-bonds is exempt from state and local income taxes, though it remains subject to federal income tax

Treasury Bills vs Treasury Bonds: What Is the Difference?

The fundamental difference between Treasury bills and Treasury bonds is the time horizon and how they pay you. T-bills are short-term instruments that mature in one year or less and pay no periodic interest — instead, you buy them at a discount and receive full face value at maturity. T-bonds are long-term instruments that mature in 20 or 30 years and pay fixed interest every six months. This difference in maturity drives nearly every other distinction between the two: price volatility, yield behavior, investor profile, and role in a portfolio.

Both are issued by the U.S. Department of the Treasury and carry the same credit guarantee, making them the benchmark for "risk-free" investments. But the risk profiles are vastly different. A 4-week T-bill is one of the safest, most liquid instruments in existence. A 30-year T-bond can lose 20-30% of its market value during a rising rate environment. Understanding which Treasury security fits your needs starts with understanding these mechanics.

How Treasury Bills Work

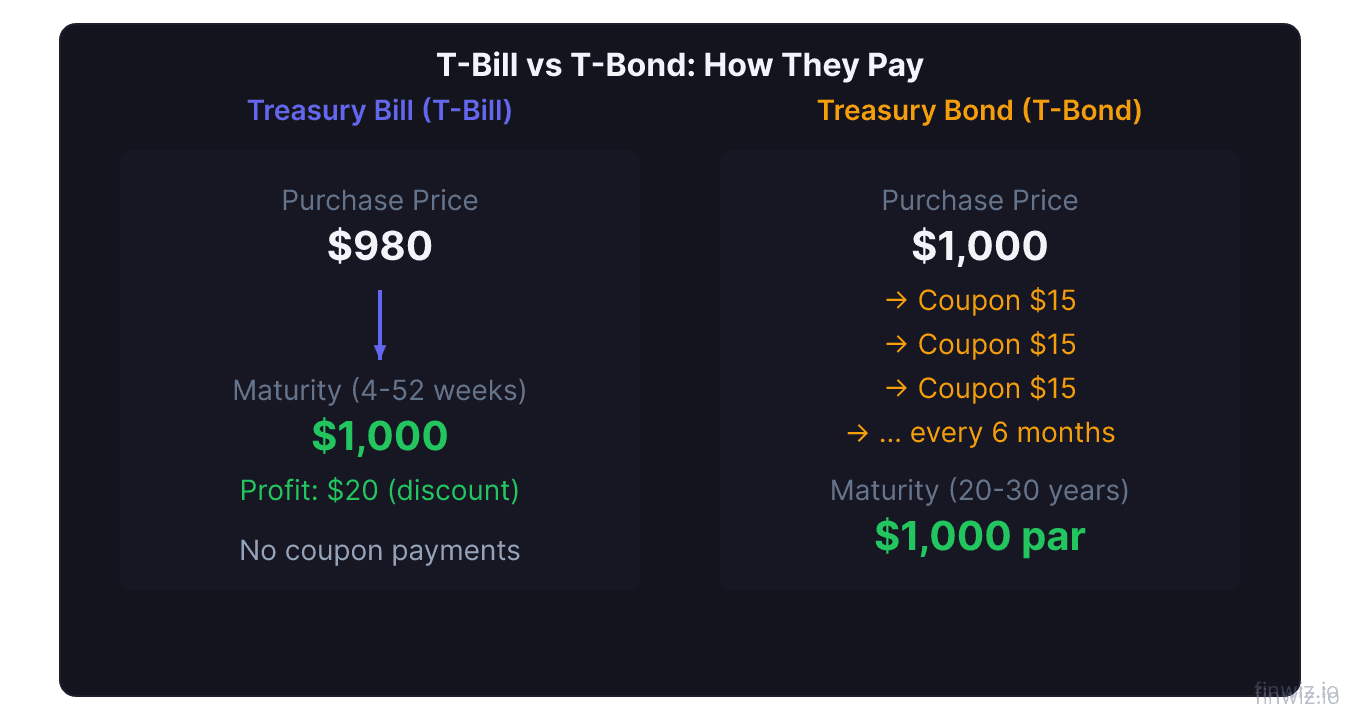

A Treasury bill is a short-term government obligation with maturities of 4, 8, 13, 17, 26, or 52 weeks. T-bills do not pay coupons. Instead, they are issued at a discount to par value ($100 face value per bill) and return the full par value at maturity. The difference between the purchase price and par is your interest income.

Example: You buy a 26-week T-bill at $97.50 per $100 of face value. After 26 weeks, the Treasury pays you $100. Your return is $2.50 on a $97.50 investment, or approximately 2.56% for the half-year period (roughly 5.12% annualized).

T-bills are auctioned weekly by the Treasury. Investors can purchase them directly through TreasuryDirect.gov with a minimum investment of $100, or indirectly through a broker. The auction uses competitive and non-competitive bidding. Most individual investors submit non-competitive bids, accepting whatever discount rate the auction determines.

Because T-bills mature so quickly, their prices barely fluctuate in the secondary market. A 4-week T-bill's price moves are measured in fractions of a cent. This near-zero volatility makes T-bills function as cash equivalents in many portfolios and institutional cash management strategies.

T-Bill Discount Yield = ((Face Value - Purchase Price) / Face Value) x (360 / Days to Maturity)How Treasury Bonds Work

A Treasury bond is a long-term government obligation with maturities of 20 or 30 years. T-bonds pay a fixed coupon rate in semiannual installments and return the full $1,000 face value at maturity. The coupon rate is set at auction and does not change for the life of the bond.

Example: You buy a 30-year T-bond with a 4.25% coupon at par ($1,000). Every six months you receive $21.25 in interest ($42.50 per year). After 30 years, you receive your $1,000 principal back. Total interest collected over the life of the bond: $1,275.

T-bonds trade actively in the secondary market, and their prices fluctuate significantly based on interest rate movements. When market rates rise, existing T-bonds with lower coupon rates become less attractive, and their prices fall. When rates fall, existing T-bonds with higher coupons become more valuable, and their prices rise.

The 30-year T-bond is the longest-dated security issued by the Treasury and serves as a benchmark for long-term interest rates. Mortgage rates, corporate bond pricing, and pension fund liabilities all reference the 30-year yield. Understanding how bonds work at this maturity range is essential for grasping fixed-income markets.

Treasury Bills vs Treasury Bonds: Key Differences

| Feature | Treasury Bills | Treasury Bonds |

|---|---|---|

| Maturity | 4 to 52 weeks | 20 or 30 years |

| How they pay | Discount to par (no coupon) | Semiannual coupon payments |

| Minimum purchase | $100 (TreasuryDirect) | $100 (TreasuryDirect) |

| Interest rate risk | Very low | Very high |

| Price volatility | Near zero | Can swing 15-30%+ |

| Typical investor | Cash management, short-term parking | Pension funds, income investors, insurers |

| State/local tax | Exempt | Exempt |

| Federal tax | Taxed as ordinary income | Taxed as ordinary income |

| Inflation risk | Minimal (short duration) | Significant (30 years of purchasing power erosion) |

| Liquidity | Extremely high | High but with wider bid-ask spreads |

Interest Rate Sensitivity: Duration in Practice

The most critical practical difference between T-bills and T-bonds is how they respond to interest rate changes. This relationship is measured by duration, which estimates the percentage price change for a one-percentage-point shift in yields.

A 4-week T-bill has a duration near zero. If rates rise by 1%, its price barely moves because it matures in days. A 30-year T-bond, by contrast, has a duration of roughly 18-20 years. If rates rise by 1%, its price falls approximately 18-20%. During the 2022-2023 rate-hiking cycle, long-term T-bonds lost over 40% of their market value from peak to trough — a drawdown rivaling some stock market crashes.

Approximate Price Change = -Duration x Change in Yield x 100Example: A 30-year T-bond with a duration of 19 experiences a 0.50% rate increase. The estimated price decline is approximately 9.5% (19 x 0.005 x 100). On a $1,000 bond, that translates to a $95 price drop, wiping out roughly two years' worth of coupon payments in a single move.

This is why T-bonds are not "safe" in the way many investors assume. They are free of credit risk but loaded with interest rate risk. T-bills are safe in both dimensions.

Pro Tip

The Yield Curve: How T-Bills and T-Bonds Connect

The yield curve plots Treasury yields across all maturities, from the shortest T-bills to the longest T-bonds. Normally, longer maturities offer higher yields to compensate investors for the added risk of time. This produces an upward-sloping curve.

When short-term T-bill yields exceed long-term T-bond yields, the curve inverts. An inverted yield curve has historically preceded every U.S. recession since the 1960s, though the lead time varies from 6 to 24 months. The inversion signals that the market expects the Federal Reserve to cut rates in the future due to economic weakness.

During bull markets, the yield curve tends to steepen as growth expectations push long-term yields higher. During periods of monetary tightening, the front end of the curve (T-bill yields) rises faster than the long end, flattening or inverting the curve.

How to read the spread: Subtract the 3-month T-bill yield from the 10-year Treasury note yield (or the 30-year T-bond yield). A positive spread means the curve is normal. A near-zero spread means it is flat. A negative spread means it is inverted.

T-Bills as Cash Alternatives

Many investors use T-bills as higher-yielding alternatives to savings accounts and money market funds. With T-bill yields reflecting current Fed policy, they often offer competitive rates compared to bank deposits with the added benefit of state tax exemption.

Laddering T-bills is a popular strategy. You divide your cash allocation into equal portions and buy T-bills maturing at staggered intervals — for example, 4-week, 8-week, 13-week, and 26-week bills. As each bill matures, you reinvest at the current rate. This provides regular liquidity while capturing the prevailing short-term yield.

T-bills are also the backbone of money market funds. Government money market funds hold almost exclusively T-bills and repurchase agreements backed by Treasuries. When you park cash in a government money market fund, you are essentially holding T-bills indirectly.

For portfolio diversification, T-bills serve as the risk-free anchor. They contribute no volatility, generate modest income, and provide dry powder for opportunistic purchases during market declines.

T-Bonds for Long-Term Income

Treasury bonds serve a different purpose: locking in a known income stream for decades. Pension funds, insurance companies, and endowments buy T-bonds to match their long-dated liabilities. An insurance company that knows it will owe claims in 25 years can buy a 30-year T-bond today and match that obligation with a guaranteed cash flow.

Individual investors sometimes buy T-bonds for retirement income planning. A retiree who buys a 30-year T-bond at a 4.5% coupon receives $45 per $1,000 invested every year for three decades, regardless of what happens to stock markets, real estate, or the economy. The trade-off is that $45 in year 30 buys significantly less than $45 today due to inflation.

T-bonds also function as portfolio hedges during economic crises. When stocks crash, investors often flee to long-term Treasuries, driving T-bond prices up sharply. During the 2008 financial crisis, the 30-year T-bond gained approximately 26% while the S&P 500 lost 37%. This negative correlation makes T-bonds a valuable counterweight in a diversified portfolio during periods of extreme stress.

Pro Tip

Tax Treatment of Treasury Securities

All Treasury interest — whether from T-bill discount income or T-bond coupon payments — is exempt from state and local income taxes. This is a meaningful advantage for investors in high-tax states like California (13.3% top rate), New York (10.9%), and New Jersey (10.75%).

At the federal level, T-bill income and T-bond coupons are taxed as ordinary income. T-bill discount income is reported in the year the bill matures. T-bond coupons are reported in the year they are received.

If you buy a T-bond in the secondary market at a premium (above par) and hold it to maturity, you can amortize that premium over the remaining life of the bond, reducing your taxable interest each year. If you buy at a discount, the discount is treated as ordinary income at maturity unless you elect to accrete it annually.

Frequently Asked Questions

Are Treasury bills safer than Treasury bonds?

Both carry the same credit guarantee from the U.S. government, so default risk is identical. However, T-bills are safer in terms of price stability. A T-bill's value barely fluctuates because it matures in weeks to months. A T-bond's market price can drop 20% or more if interest rates rise. If you hold a T-bond to its full 20- or 30-year maturity, you will receive par value regardless of interim price swings — but the opportunity cost of holding a below-market coupon for decades is real.

Can I sell Treasury bills or bonds before maturity?

Yes, both T-bills and T-bonds trade actively in the secondary market through any brokerage account. T-bills are extremely liquid and can be sold with negligible price impact. T-bonds are also liquid, but you may receive more or less than you paid depending on how interest rates have moved since you purchased. Selling a T-bond when rates have risen means selling at a loss.

How do I choose between T-bills and T-bonds?

The choice depends on your time horizon and purpose. If you need a safe place to park cash for weeks to months, T-bills are appropriate. If you want to lock in long-term income and are comfortable with price volatility, T-bonds serve that role. Most investors hold neither directly — instead, they gain Treasury exposure through bond ETFs or mutual funds that hold a mix of maturities matched to their investment goals and diversification strategy.

What is the current yield on T-bills and T-bonds?

Treasury yields change daily based on auction results and secondary market trading. You can find current rates at TreasuryDirect.gov or on any financial data site. Yields are influenced by Federal Reserve policy (especially for T-bills), inflation expectations, economic growth forecasts, and global demand for safe-haven assets.

Related Articles

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.