TIPS: Treasury Inflation-Protected Securities Explained

⚡ Key Takeaways

- TIPS (Treasury Inflation-Protected Securities) are U.S. government bonds whose principal adjusts with the Consumer Price Index (CPI), providing built-in inflation protection

- The coupon rate is fixed, but it is applied to the inflation-adjusted principal, so interest payments rise with inflation

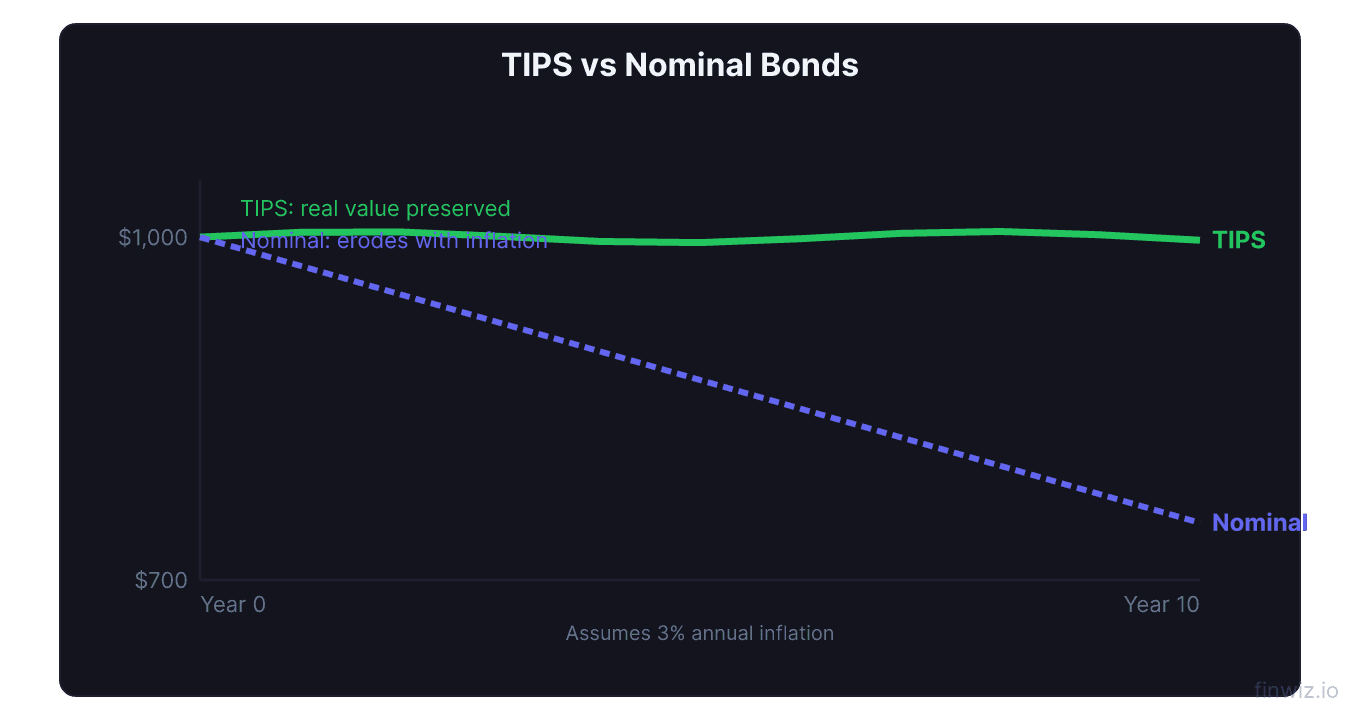

- TIPS provide a guaranteed real yield above inflation, unlike nominal bonds which can deliver negative real returns during inflationary periods

- A deflation floor protects TIPS holders — at maturity you receive the greater of the adjusted principal or the original face value

- You can buy TIPS through TreasuryDirect.gov, brokerage accounts, or ETFs like the iShares TIPS Bond ETF (TIP)

What Are TIPS Bonds?

TIPS (Treasury Inflation-Protected Securities) are U.S. Treasury bonds specifically designed to protect investors against inflation. Unlike conventional Treasury bonds that pay a fixed coupon on a fixed face value, TIPS adjust their principal value based on changes in the Consumer Price Index (CPI). When inflation rises, the principal increases, and when deflation occurs, the principal decreases — but it can never fall below the original face value at maturity. This mechanism ensures that TIPS holders earn a guaranteed real return (a return above inflation) for as long as they hold the bond.

TIPS were introduced by the U.S. Treasury in 1997 and have become a cornerstone of inflation-protected investing. They are issued in 5-year, 10-year, and 30-year maturities, pay interest semi-annually, and are backed by the full faith and credit of the U.S. government, making them among the safest investments available.

How TIPS Principal Adjustment Works

The defining feature of TIPS is the inflation-indexed principal. Every day, the Treasury adjusts the principal value of TIPS based on changes in the non-seasonally adjusted CPI-U (Consumer Price Index for All Urban Consumers).

Here is how the adjustment works with a concrete example:

| Timeline | CPI Change | Adjusted Principal (per $1,000 face) | Coupon Rate | Semi-Annual Interest Payment |

|---|---|---|---|---|

| At issue | Baseline | $1,000 | 1.5% | $7.50 |

| After 1 year (3% inflation) | +3.0% | $1,030 | 1.5% | $7.73 |

| After 2 years (3% more inflation) | +6.09% cumulative | $1,060.90 | 1.5% | $7.96 |

| After 3 years (2% more inflation) | +8.29% cumulative | $1,082.90 | 1.5% | $8.12 |

Adjusted Principal = Original Face Value x (Current CPI / CPI at Issue Date)Notice that the coupon rate stays fixed at 1.5% throughout the life of the bond. What changes is the principal on which that rate is applied. As inflation pushes the principal higher, the dollar amount of each interest payment increases proportionally. At maturity, you receive the inflation-adjusted principal, not the original $1,000 face value.

Real Yield vs. Nominal Yield

Understanding the difference between real yield and nominal yield is essential for evaluating TIPS versus conventional Treasury bonds.

Nominal yield is the yield on a conventional Treasury bond. It includes both the real return and an inflation component. A 10-year Treasury note yielding 4.5% might consist of a 2.0% real yield plus 2.5% expected inflation.

Real yield is the yield on TIPS. It represents the return above and beyond inflation. A 10-year TIPS yielding 2.0% guarantees you will earn 2.0% per year more than whatever inflation turns out to be.

Break-even inflation rate is the difference between the nominal Treasury yield and the TIPS real yield. It represents the inflation rate at which TIPS and conventional Treasuries would produce identical total returns.

Break-Even Inflation Rate = Nominal Treasury Yield - TIPS Real YieldThe break-even rate gives you a decision framework. If you believe inflation will run higher than the break-even rate over the bond's lifetime, TIPS are the better choice. If you believe inflation will be lower, conventional Treasuries offer a better return.

Pro Tip

The Deflation Floor

TIPS include a critical safety feature: the deflation floor. At maturity, the Treasury pays the greater of the inflation-adjusted principal or the original face value. This means that even if the CPI declines during the bond's lifetime (deflation), you are guaranteed to receive at least your original $1,000 per bond.

During the bond's life, the adjusted principal can fall below face value if deflation occurs, and your interest payments would temporarily decrease. However, the deflation floor ensures that you cannot lose principal if you hold to maturity.

| Scenario | During Bond's Life | At Maturity |

|---|---|---|

| Cumulative inflation of 20% | Principal = $1,200, higher interest payments | Receive $1,200 |

| Cumulative inflation of 0% | Principal = $1,000, unchanged interest | Receive $1,000 |

| Cumulative deflation of 5% | Principal = $950, lower interest payments | Receive $1,000 (deflation floor) |

This deflation floor is especially valuable for risk-averse investors. It means TIPS provide upside participation in inflation while guaranteeing you will not lose principal to deflation over the full holding period. The only scenario where you can lose money on TIPS is if you sell before maturity when real yields have risen (causing the market price to fall), similar to the interest rate risk on any bond.

How to Buy TIPS

There are three primary ways to purchase TIPS, each suited to different investor profiles.

TreasuryDirect.gov is the U.S. government's online platform for buying Treasury securities directly. You can purchase TIPS at auction with no commission or fees, in amounts as low as $100. TIPS are auctioned multiple times per year in 5-year, 10-year, and 30-year maturities. TreasuryDirect is ideal for buy-and-hold investors who plan to hold to maturity.

Brokerage accounts allow you to buy TIPS in the secondary market through any major broker (Schwab, Fidelity, Vanguard, etc.). You can purchase previously issued TIPS at current market prices, which may be above or below face value depending on current real yields and accumulated inflation adjustments. This approach offers more flexibility in terms of selecting specific maturities and durations.

TIPS ETFs and mutual funds provide the easiest access for most investors. These funds hold diversified portfolios of TIPS across multiple maturities and automatically reinvest interest payments.

| TIPS ETF | Ticker | Expense Ratio | Average Duration | Description |

|---|---|---|---|---|

| iShares TIPS Bond ETF | TIP | 0.19% | ~6.5 years | Broad TIPS exposure, most popular |

| Vanguard Short-Term Inflation-Protected Securities ETF | VTIP | 0.04% | ~2.5 years | Short-duration, lower rate risk |

| Schwab U.S. TIPS ETF | SCHP | 0.03% | ~6.5 years | Lowest cost broad TIPS fund |

| PIMCO 15+ Year U.S. TIPS Index ETF | LTPZ | 0.20% | ~20 years | Long-duration, maximum inflation sensitivity |

Pro Tip

TIPS and Taxes: The Phantom Income Problem

One significant drawback of TIPS is the phantom income tax issue. The IRS taxes the annual increase in TIPS principal as ordinary income in the year it occurs, even though you do not actually receive the principal adjustment until maturity. This means you owe taxes on income you have not yet received in cash.

For example, if your $10,000 TIPS investment has its principal adjusted upward by 3% ($300), you owe federal income tax on that $300 even though it simply increased the bond's face value. You also owe tax on the coupon payments received.

This phantom income problem makes TIPS less tax-efficient in taxable brokerage accounts. There are two common solutions:

Hold TIPS in tax-advantaged accounts. Placing TIPS in an IRA, 401(k), or other tax-deferred account eliminates the phantom income issue entirely. The principal adjustments and interest payments compound tax-free until withdrawal.

Use TIPS ETFs. While TIPS ETFs do not eliminate the tax issue, they simplify accounting. The fund handles the inflation adjustments internally, and you only need to report the distributions you receive.

When TIPS Make Sense in Your Portfolio

TIPS are not always the optimal choice. Their value depends on the inflation environment and your portfolio objectives.

TIPS are most valuable when:

- You believe inflation will exceed market expectations (the break-even rate)

- You want a risk-free real return above inflation

- You need to fund future obligations that are inflation-linked (like retirement living expenses)

- Real yields are historically high (above 1.5% to 2.0%), locking in attractive above-inflation returns

- You want portfolio diversification that performs well during inflationary periods when stocks and nominal bonds may struggle

TIPS are less attractive when:

- Inflation expectations are well-anchored and unlikely to surprise to the upside

- Real yields are near zero or negative, offering minimal return above inflation

- You are in a high tax bracket and holding in a taxable account (phantom income drag)

- You prefer liquidity and simplicity (I-bonds or index funds may be more practical)

TIPS vs. I-Bonds

Both TIPS and I-bonds protect against inflation, but they work differently and suit different investors.

| Feature | TIPS | I-Bonds |

|---|---|---|

| Issuer | U.S. Treasury | U.S. Treasury |

| Inflation mechanism | Principal adjusts with CPI | Interest rate adjusts with CPI |

| Market trading | Yes (secondary market, ETFs) | No (held directly with Treasury) |

| Annual purchase limit | None | $10,000 electronic + $5,000 paper |

| Minimum hold period | None (can sell anytime in market) | 1 year |

| Early redemption penalty | Market price risk if sold before maturity | 3 months interest if redeemed before 5 years |

| Deflation floor | Yes (at maturity only) | Yes (composite rate cannot go below 0%) |

| Phantom income tax issue | Yes | No (tax deferred until redemption) |

| Best for | Large allocations, portfolio-level inflation hedging | Small steady contributions, emergency savings |

For most individual investors, the optimal approach is to max out I-bond purchases ($10,000 per year) for their tax deferral advantage and simplicity, then use TIPS ETFs for any additional inflation-protected allocation.

TIPS Performance During the 2021-2022 Inflation Surge

The 2021-2022 inflationary period demonstrated exactly why investors hold TIPS. As CPI surged from 1.4% in January 2021 to a peak of 9.1% in June 2022, TIPS principal adjustments skyrocketed, delivering significantly higher real returns than nominal Treasuries.

During 2021, TIPS returned approximately 5.7%, while conventional long-term Treasuries lost about 2.5%. The divergence was even more dramatic in late 2021 and early 2022, when investors who held nominal bonds were locked into coupons that fell far below the inflation rate, suffering negative real returns.

However, when the Federal Reserve aggressively raised interest rates in 2022 to combat inflation, even TIPS lost market value because rising real yields pushed TIPS prices down. Investors who held to maturity were not affected, but those holding TIPS funds saw price declines. This illustrates that TIPS protect against inflation but not against rising real interest rates.

Frequently Asked Questions

Are TIPS a good investment right now?

TIPS attractiveness depends on the current real yield and your inflation outlook. When real yields are above 1.5% to 2.0%, TIPS offer a historically attractive guaranteed return above inflation. Compare the break-even inflation rate to your personal inflation expectations. If you believe inflation will exceed the break-even rate over the bond's term, TIPS are likely a good choice. TIPS are especially compelling during periods of fiscal expansion, supply chain disruption, or other inflationary catalysts.

Can you lose money on TIPS?

If you hold TIPS to maturity, you cannot lose your original principal due to the deflation floor. However, if you sell TIPS before maturity, you may receive more or less than you paid depending on changes in real yields. Rising real yields cause TIPS prices to fall, just as rising nominal yields cause conventional bond prices to fall. In 2022, the iShares TIPS ETF (TIP) declined approximately 12% as the Fed raised rates aggressively, even though the inflation adjustments were positive.

How are TIPS different from regular Treasury bonds?

Regular Treasury bonds pay a fixed coupon on a fixed face value. If inflation rises, the purchasing power of your fixed payments erodes. TIPS pay a fixed coupon on an inflation-adjusted face value, so your payments and principal grow with CPI. The trade-off is that TIPS typically have lower coupon rates than comparable-maturity nominal Treasuries, reflecting the value of the inflation protection built into the bond.

Should I hold TIPS in a Roth IRA?

Holding TIPS in a Roth IRA is an excellent strategy because it solves the phantom income tax problem and allows all principal adjustments and interest to grow tax-free. Since TIPS returns are expected to be moderate (real yield plus inflation), the tax-free compounding in a Roth maximizes their value. A traditional IRA also works well since it defers the phantom income tax until withdrawal.

What happens to TIPS if there is deflation?

During deflationary periods, the adjusted principal of TIPS decreases, and your semi-annual interest payments decline proportionally. However, the deflation floor guarantees that at maturity, you receive the greater of the adjusted principal or the original face value. So even if prices decline over the bond's life, your principal is fully protected if you hold to maturity. During the bond's life, the market price of TIPS may fall below par in a deflationary environment, but this only matters if you sell before maturity.

Disclaimer

This is educational content, not financial advice. Trading involves risk, and you should consult a qualified financial advisor before making any investment decisions. Past performance does not guarantee future results.

Related Articles

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.