Bonds vs Stocks: Risk, Returns & When to Own Each

⚡ Key Takeaways

- Stocks represent ownership in a company with unlimited upside potential, while bonds represent a loan to a company or government with fixed interest payments and return of principal at maturity

- Historically, stocks have returned approximately 10% annually (S&P 500) versus 5-6% for bonds (Bloomberg Aggregate Bond Index), but with significantly greater volatility

- Bonds provide predictable income and capital preservation, acting as a portfolio stabilizer during stock market downturns when investors flee to safety

- Stock dividends qualify for lower tax rates (0-20%), while bond interest is taxed as ordinary income (up to 37%), creating a meaningful after-tax difference

- Most portfolios hold both asset classes, with the allocation between them being one of the most consequential investment decisions you can make

Bonds vs Stocks: What Is the Difference?

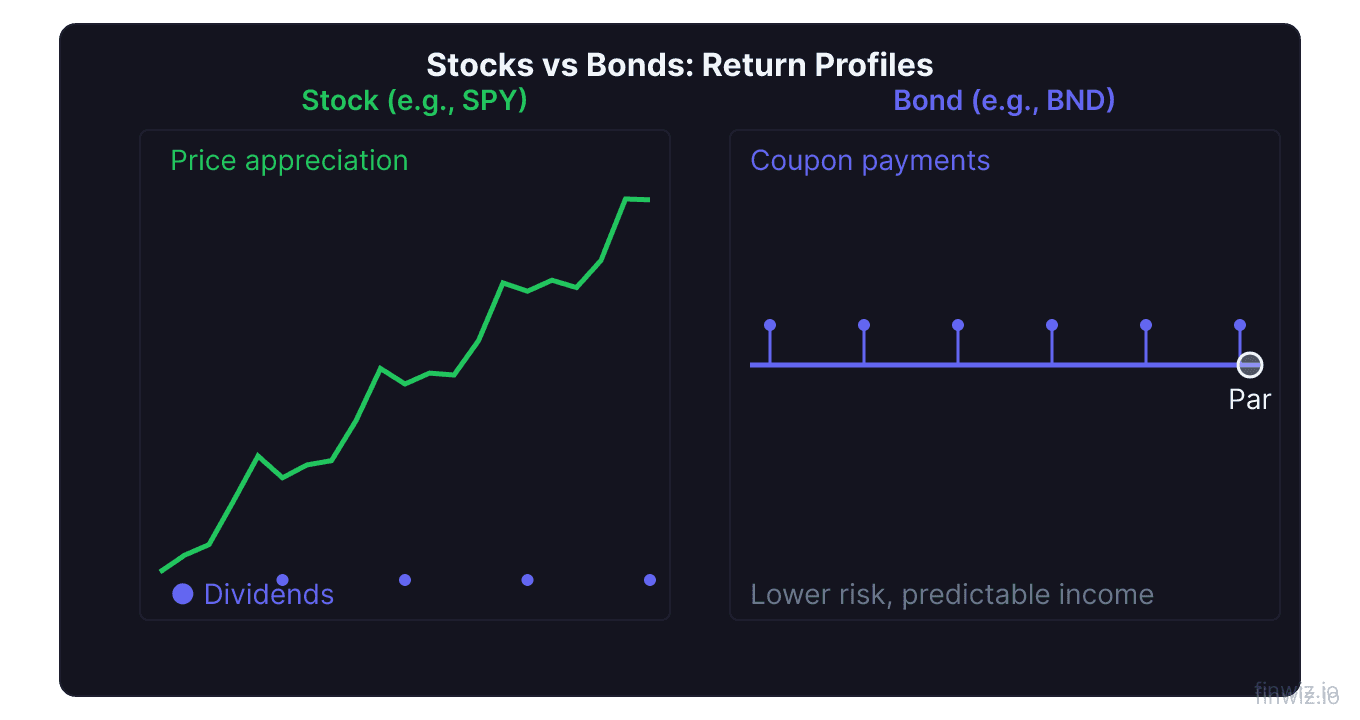

The fundamental difference between bonds and stocks is the relationship you have with the issuer. When you buy a stock, you become a partial owner of the company, sharing in its profits and losses. When you buy a bond, you become a lender, providing capital in exchange for regular interest payments and the return of your principal at a set date. This distinction between ownership and lending drives every meaningful difference in risk, return, income, and tax treatment between these two asset classes.

Stocks offer higher long-term returns but subject you to significant volatility along the way. Bonds offer lower returns but deliver predictable income and preserve capital more reliably. Understanding how bonds and stocks differ, and when each performs best, forms the foundation of portfolio diversification and sound investing.

What Is a Stock?

A stock represents fractional ownership in a publicly traded company. If a company has 10 million shares outstanding and you own 1,000 shares, you hold 0.01% of the business. Your returns come from two sources.

Capital appreciation occurs when the stock price rises. If you buy AAPL at $150 and sell at $200, your $50 per share gain represents a 33% return. Stock prices reflect the market's collective judgment about the company's current and future value, shifting with earnings reports, economic data, and investor sentiment.

Dividends are cash distributions paid from the company's profits. Companies like Johnson & Johnson (JNJ), Procter & Gamble (PG), and Coca-Cola (KO) have increased their dividends annually for over 50 consecutive years. Not all stocks pay dividends — many growth companies like Amazon (AMZN) reinvest all profits into expansion instead.

The risk with stocks is real. You can lose your entire investment if a company goes bankrupt. Even blue-chip stocks can decline 30-50% during bear markets. Individual companies can lose value permanently due to competitive disruption, mismanagement, or industry decline.

What Is a Bond?

A bond is a debt instrument. When you buy a bond, you lend money to the issuer — a corporation, municipality, or government — for a specified period. In return, the issuer pays you periodic interest (the coupon) and returns your original investment (the par value, typically $1,000) at maturity.

Example: You purchase a 10-year corporate bond with a $1,000 face value and a 4.5% coupon rate. Each year you receive $45 in interest. After 10 years, the issuer returns your $1,000 principal. Your total return is $450 in interest plus the return of par.

Bonds carry risks distinct from stocks. Interest rate risk causes bond prices to fall when market rates rise (an existing 3% bond becomes less attractive when new bonds offer 5%). Credit risk means the issuer might default on payments. Inflation risk means fixed coupon payments lose purchasing power over time. Despite these risks, bonds are generally far less volatile than stocks and provide more predictable cash flows.

U.S. Treasury bonds are considered the safest, backed by the full faith and credit of the federal government. Corporate bonds pay higher yields to compensate for greater credit risk. Municipal bonds offer tax-free interest for investors in high tax brackets.

Bonds vs Stocks: Key Differences

| Feature | Stocks | Bonds |

|---|---|---|

| What you own | Equity (partial ownership) | Debt (you are a creditor) |

| Income type | Dividends (variable, can grow) | Coupon interest (fixed) |

| Return potential | Unlimited upside | Capped at coupon + par recovery |

| Historical annual return | ~10% (S&P 500) | ~5-6% (aggregate bond index) |

| Volatility | High (20-50% drawdowns common) | Low to moderate (5-15% drawdowns) |

| Bankruptcy priority | Last (after all creditors) | Before stockholders |

| Maturity | None (perpetual ownership) | Fixed maturity date |

| Tax treatment | Qualified dividends at 0-20% | Interest taxed as ordinary income |

Risk and Volatility: SPY vs BND

Comparing the SPDR S&P 500 ETF (SPY) and the Vanguard Total Bond Market ETF (BND) illustrates the volatility gap between stocks and bonds in practical terms.

SPY, which tracks the S&P 500, has experienced multiple drawdowns exceeding 20% since its inception. During the 2008 financial crisis, SPY fell approximately 55% from peak to trough. During the 2020 COVID crash, it dropped 34% in about five weeks. These are stomach-turning declines that test even experienced investors.

BND, which tracks the Bloomberg U.S. Aggregate Bond Index, has a much narrower range of outcomes. Its worst calendar year performance was a roughly 13% decline in 2022 during the Federal Reserve's aggressive rate-hiking cycle. In typical years, BND fluctuates within a band of negative 2% to positive 8%.

The critical insight is that SPY's superior long-term returns come at the price of severe short-term drawdowns. An investor who panics and sells during a 40% stock decline locks in catastrophic losses and misses the recovery. Bonds serve as the emotional anchor that prevents this destructive behavior. Understanding market cycles helps you anticipate these shifts.

Pro Tip

Return Profiles Over Time

The compounding difference between stock and bond returns is dramatic over long periods. A $100,000 investment growing at 10% annually (stocks' historical average) becomes approximately $1,745,000 after 30 years. The same amount growing at 5.5% (bonds' historical average) reaches roughly $498,000. Stocks generate about 3.5 times more wealth over three decades.

However, sequence matters. Stocks do not deliver smooth 10% returns each year. They might gain 25% one year, lose 15% the next, then gain 30%. Bonds deliver more consistent, modest returns that make financial planning more predictable.

For investors accumulating wealth with a 20-30 year horizon, stocks are the primary engine of growth. For investors nearing retirement or drawing income from their portfolio, bonds provide the stability needed to avoid selling stocks during downturns. Most investors benefit from holding both, adjusting the ratio as their time horizon shortens.

The classic allocation formula uses age as a starting point:

Bond Allocation = Your Age (as a percentage)A 30-year-old would hold 30% bonds and 70% stocks. A 60-year-old would hold 60% bonds and 40% stocks. Many modern advisors consider this too conservative for younger investors and adjust the formula to (Age - 20), resulting in more aggressive stock exposure during the critical wealth-building years.

Tax Treatment: Bonds vs Stocks

Tax differences between stocks and bonds are often underappreciated and can meaningfully affect after-tax returns.

Stock dividends that qualify as "qualified dividends" (held for at least 61 days around the ex-dividend date) are taxed at preferential rates of 0%, 15%, or 20% depending on your income bracket. Long-term capital gains on stocks held over one year receive the same preferential treatment.

Bond interest is taxed as ordinary income at your marginal tax rate, which can be as high as 37% for federal taxes. For a high-income investor in the 37% bracket, a 5% bond coupon yields only 3.15% after federal tax. A 3% qualified stock dividend yields 2.4% after the 20% dividend rate — a narrower gap than the pre-tax numbers suggest.

Municipal bonds are the exception. Interest from muni bonds is exempt from federal income tax and often from state tax if the bond is issued within your state of residence. For high-income investors, a 3.5% muni bond yielding tax-free income can be equivalent to a 5.5%+ taxable bond.

Inside tax-advantaged accounts like Roth IRAs and 401(k)s, these distinctions disappear. All growth is tax-deferred or tax-free, making the pre-tax return the only consideration.

When to Own Each

Stocks work best when:

- Your investment horizon is 10 years or longer

- You can tolerate significant short-term declines without selling

- You are building wealth for retirement decades away

- You want income that grows over time through rising dividends

- You are dollar-cost averaging into broad index funds like SPY or VTI

Bonds work best when:

- You need predictable income with minimal volatility

- Your investment horizon is under 5 years (saving for a house, car, or college)

- You are retired and funding near-term living expenses

- You want to reduce overall portfolio volatility

- Interest rates are high, making bond yields attractive relative to historical averages

Both together work best when:

- You want the highest risk-adjusted returns (Sharpe ratio optimization)

- You need emotional stability to stay invested during stock market crashes

- You are transitioning from wealth accumulation to wealth preservation

- You want to rebalance systematically, buying whichever asset class has declined

Frequently Asked Questions

Are bonds safer than stocks?

In the short term, yes. Bonds, especially U.S. Treasuries, have far less price volatility than stocks and provide predictable income. However, bonds carry their own risks. Rising interest rates cause bond prices to decline. Inflation erodes the purchasing power of fixed coupon payments. And over very long periods (20+ years), stocks have historically always produced positive returns, while bonds have sometimes failed to outpace inflation. Safety depends on your definition and time horizon.

Should I own stocks or bonds right now?

Both. Attempting to time which asset class will outperform in the near term is unreliable even for professionals. A diversified portfolio holding both stocks and bonds ensures you benefit regardless of market direction. If you have a long horizon, weight more toward stocks. If you need money within five years, weight more toward bonds. Dollar-cost averaging into both over time is the most proven approach.

Can dividend stocks replace bonds?

Partially, but not fully. High-quality dividend stocks like those in the Dividend Aristocrats index provide growing income and tend to be less volatile than growth stocks. However, during severe market downturns, even the best dividend stocks can decline 30-40%, while Treasury bonds often appreciate. Bonds provide crisis-level capital preservation that no stock can match. A balanced approach uses dividend stocks for growing income and bonds for stability.

How do bond ETFs compare to individual bonds?

Individual bonds return your exact principal at maturity, providing certainty if held to term. Bond ETFs like BND hold a diversified portfolio of bonds and trade on exchanges, so their price fluctuates without a defined maturity date. Bond ETFs offer diversification, liquidity, and low minimums. Individual bonds offer guaranteed return of par at maturity. For most investors, bond ETFs are simpler and more practical.

What is the 60/40 portfolio?

The 60/40 portfolio allocates 60% to stocks and 40% to bonds. It has been the institutional standard for decades, historically delivering roughly 8% annualized returns with significantly less volatility than a 100% stock portfolio. During 2022, both stocks and bonds declined simultaneously, leading some to question the strategy. However, this positive correlation is unusual and historically temporary. The 60/40 portfolio remains a reasonable baseline for investors approaching or in retirement.

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.