Compound Interest: The Most Powerful Force in Investing

⚡ Key Takeaways

- Compound interest is interest earned on both your original principal AND previously accumulated interest

- The Rule of 72 estimates how long it takes to double your money: divide 72 by the annual return rate

- Starting early is the most powerful factor — a 25-year-old investing $200/month will outpace a 35-year-old investing $400/month

- Compound interest works exponentially: growth accelerates dramatically in later years

- The difference between compound and simple interest grows enormous over long time periods

What Is Compound Interest?

Compound interest is the process of earning interest on your interest. It is the single most powerful force in personal finance and investing, and Albert Einstein reportedly called it the "eighth wonder of the world." Whether or not he actually said that, the sentiment is accurate.

With simple interest, you earn returns only on your original investment (the principal). With compound interest, you earn returns on your principal plus all the interest that has accumulated before. Over time, this creates a snowball effect where your money grows exponentially rather than linearly.

Here is a simple example. You invest $1,000 at 10% annual interest:

| Year | Simple Interest | Compound Interest |

|---|---|---|

| 1 | $1,100 | $1,100 |

| 5 | $1,500 | $1,611 |

| 10 | $2,000 | $2,594 |

| 20 | $3,000 | $6,727 |

| 30 | $4,000 | $17,449 |

After 30 years, simple interest turns $1,000 into $4,000. Compound interest turns it into $17,449 — more than four times as much. The difference is entirely due to earning returns on your accumulated returns.

The Compound Interest Formula

Understanding the math behind compounding helps you appreciate its power and make better financial decisions.

A = P(1 + r/n)^(n*t)Where:

- A = Final amount (future value)

- P = Principal (initial investment)

- r = Annual interest rate (as a decimal)

- n = Number of times interest compounds per year

- t = Number of years

For a $10,000 investment at 8% compounded monthly for 20 years:

A = $10,000 x (1 + 0.08/12)^(12 x 20) = $10,000 x (1.00667)^240 = $10,000 x 4.926 = $49,268Your $10,000 grew to $49,268 — nearly five times your original investment. The $39,268 in growth came entirely from compounding.

Compounding frequency affects the result, but the differences are relatively small:

| Frequency | Value after 20 years ($10,000 at 8%) |

|---|---|

| Annually | $46,610 |

| Quarterly | $48,010 |

| Monthly | $49,268 |

| Daily | $49,530 |

| Continuously | $49,530 |

The jump from annual to monthly compounding is meaningful, but beyond monthly, the differences are negligible. For most investments (stocks, funds), returns compound continuously in practice since stock prices change by the second.

Try It: Compound Interest Calculator

The Rule of 72

The Rule of 72 is a simple mental math shortcut for estimating how long it takes to double your money at a given rate of return.

Years to Double = 72 / Annual Rate of Return| Annual Return | Years to Double |

|---|---|

| 4% | 18 years |

| 6% | 12 years |

| 8% | 9 years |

| 10% | 7.2 years |

| 12% | 6 years |

At 10% average annual returns (the historical stock market average), your money doubles approximately every 7.2 years. This means:

- $10,000 at age 25 becomes $20,000 by age 32

- $20,000 becomes $40,000 by age 39

- $40,000 becomes $80,000 by age 46

- $80,000 becomes $160,000 by age 53

- $160,000 becomes $320,000 by age 60

That original $10,000 becomes $320,000 through five doublings over 35 years — without adding another dollar. This is compounding in action.

Pro Tip

Compound Interest vs Simple Interest

The difference between compound and simple interest is the difference between linear and exponential growth. Over short periods, they look similar. Over long periods, the gap becomes enormous.

Simple Interest: A = P x (1 + r x t)Compound Interest: A = P x (1 + r)^tLet's compare $10,000 at 8% over various periods:

| Time | Simple Interest | Compound Interest | Difference |

|---|---|---|---|

| 1 year | $10,800 | $10,800 | $0 |

| 5 years | $14,000 | $14,693 | $693 |

| 10 years | $18,000 | $21,589 | $3,589 |

| 20 years | $26,000 | $46,610 | $20,610 |

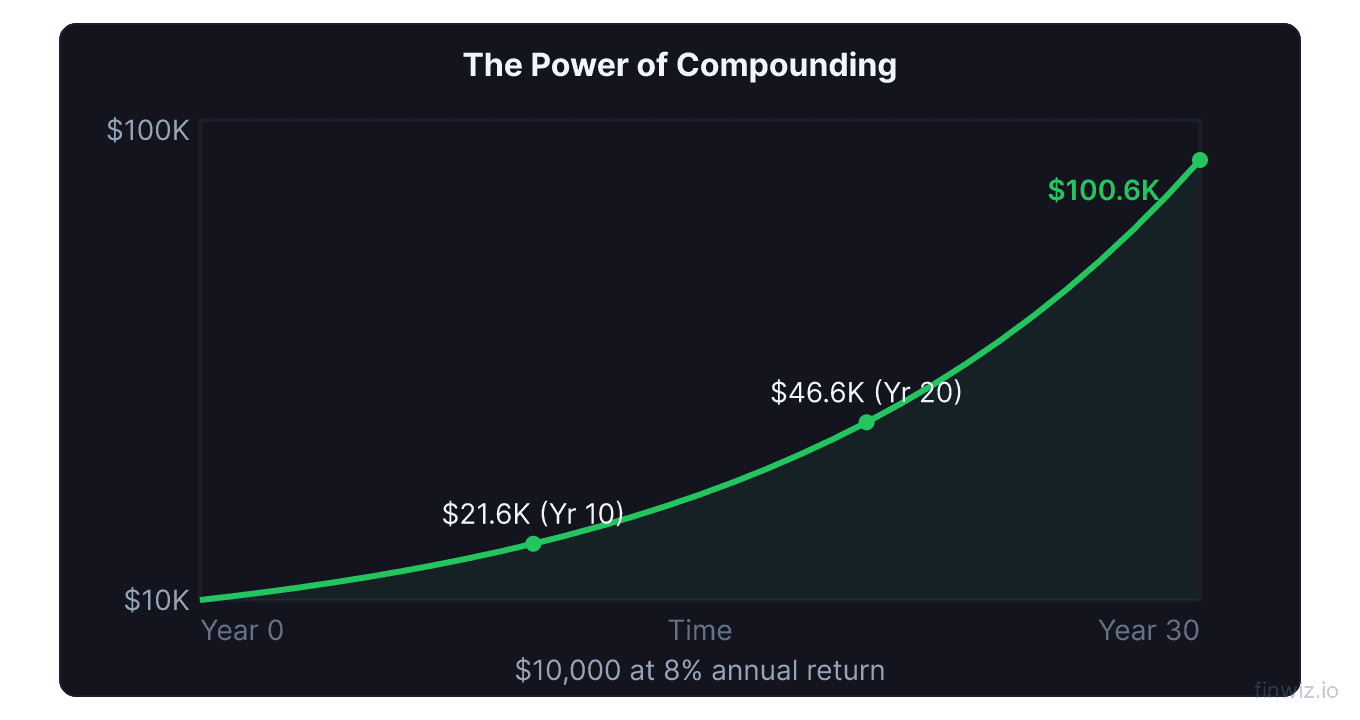

| 30 years | $34,000 | $100,627 | $66,627 |

| 40 years | $42,000 | $217,245 | $175,245 |

After 40 years, compound interest produces more than 5 times the result of simple interest from the same starting investment. The magic happens in the later years. In year 1, compounding adds zero extra. By year 40, compounding is generating more annual growth than the entire simple interest total.

This exponential nature is why time in the market is the single most important factor in building wealth. The longer your money compounds, the more dramatically it grows.

The Power of Starting Early

The most consequential decision in investing is when you start. Starting even a few years earlier can make a difference of hundreds of thousands of dollars by retirement.

Consider two investors, both targeting retirement at age 65:

Investor A starts at age 25, investing $200/month at 8% average annual return.

Investor B starts at age 35, investing $400/month (twice as much!) at the same 8% return.

| Age | Investor A (started at 25) | Investor B (started at 35) |

|---|---|---|

| 25 | $0 | — |

| 35 | $36,589 | $0 |

| 45 | $118,589 | $73,178 |

| 55 | $298,072 | $219,326 |

| 65 | $702,856 | $478,513 |

Investor A contributes a total of $96,000 ($200 x 480 months). Investor B contributes $144,000 ($400 x 360 months). Despite contributing $48,000 less, Investor A ends up with $224,343 more. The extra 10 years of compounding is worth more than doubling the monthly contribution.

This is the most compelling argument for starting to invest as early as possible, even with small amounts. Every year of delay costs you disproportionately.

How Compounding Works in Real Investments

The examples above use fixed interest rates, but real investments like stocks, index funds, and bonds compound differently.

Stocks and index funds compound through both price appreciation and reinvested dividends. When you reinvest dividends (buying more shares with the dividend payment), you increase the number of shares you own. Those additional shares then earn their own dividends and appreciation, creating the compounding effect.

| $10,000 invested in S&P 500 | Without Dividend Reinvestment | With Dividend Reinvestment |

|---|---|---|

| After 10 years (avg) | ~$21,000 | ~$26,000 |

| After 20 years (avg) | ~$44,000 | ~$67,000 |

| After 30 years (avg) | ~$92,000 | ~$174,000 |

Reinvesting dividends nearly doubles the 30-year result. This is why every investment account should have automatic dividend reinvestment turned on unless you specifically need the income.

Savings accounts and CDs compound in the traditional sense — interest is added to your balance at regular intervals, and future interest is calculated on the new, higher balance. Current high-yield savings rates of 4-5% provide meaningful compounding, though they barely keep pace with inflation after taxes.

Bonds compound when coupon payments are reinvested. A bond paying 5% annually compounds if you use those payments to buy more bonds, which then pay their own 5%.

Factors That Enhance or Diminish Compounding

Several factors can accelerate or slow down the compounding effect on your investments.

Enhancers:

- Higher returns. The higher your rate of return, the faster compounding works. This is why stocks (8-10% historical average) build wealth faster than bonds (4-5%) or savings accounts (2-4%).

- Longer time horizon. Compounding is exponential — the benefits are minimal in early years and enormous in later years. Maximize your time in the market.

- Regular contributions. Adding money consistently (dollar-cost averaging) gives compounding more fuel to work with.

- Dividend reinvestment. Every dividend reinvested buys more shares that earn their own returns.

- Tax-advantaged accounts. Roth IRAs and traditional IRAs shield your returns from taxes, letting 100% of your gains compound.

Diminishers:

- Fees and expenses. A 1% annual fee seems small but reduces your ending balance by 25-30% over 30 years.

- Taxes. Capital gains taxes and taxes on dividends siphon off money that could otherwise compound.

- Inflation. A 3% inflation rate means your 8% nominal return is really only a 5% real return.

- Withdrawals. Every dollar withdrawn is a dollar that stops compounding. Early withdrawals are especially costly.

- Interruptions. Selling during market downturns and buying back later breaks the compounding chain and typically results in buying back at higher prices.

Pro Tip

Real-World Compounding Scenarios

Here are practical scenarios showing how compound interest applies to common financial goals.

Scenario 1: Retirement savings $500/month starting at age 30, invested in index funds at 8% average return until age 65:

Future Value = $500 x [(1.00667^420 - 1) / 0.00667] = $1,148,226Total contributed: $210,000. Total growth: $938,226 — that is 4.5x your contributions.

Scenario 2: College fund $300/month for 18 years at 7% average return:

Future Value = $300 x [(1.00583^216 - 1) / 0.00583] = $130,353Total contributed: $64,800. Growth: $65,553 — compounding more than doubled your contributions.

Scenario 3: Emergency fund in high-yield savings $200/month at 4.5% APY for 2 years:

Future Value = $200 x [(1.00375^24 - 1) / 0.00375] = $5,002Total contributed: $4,800. Growth: $202. Over short periods, compounding adds relatively little because the exponential curve has not had time to steepen.

Frequently Asked Questions

How is compound interest different from return on investment?

Compound interest specifically describes the process of earning returns on previous returns over time. Return on investment (ROI) is a broader measure of how much profit an investment has generated relative to its cost. Compound interest is the mechanism; ROI is the measurement. An investment can have a high ROI without significant compounding if it is held for a short period.

Does the stock market compound?

Yes, though not through traditional "interest" payments. Stock investments compound through reinvested dividends (buying more shares) and continuous price appreciation (each day's gains are added to the base for the next day's gains). The S&P 500's historical ~10% average annual return includes this compounding effect.

What is the best way to take advantage of compound interest?

Start investing as early as possible, invest consistently (monthly contributions), reinvest all dividends, minimize fees by using low-cost index funds, use tax-advantaged accounts like Roth IRAs, and do not withdraw money or interrupt the compounding process. The most powerful factor is time — even small amounts invested early dramatically outperform larger amounts invested later.

Can compound interest work against me?

Yes. Compound interest on debt works against you with the same mathematical force. Credit card debt at 20% APR compounds rapidly, causing your balance to grow exponentially if you only make minimum payments. A $5,000 credit card balance at 20% with minimum payments can take over 30 years to pay off and cost over $12,000 in interest. Pay off high-interest debt before investing.

How does inflation affect compound interest?

Inflation reduces the real purchasing power of your compounded returns. If your investments earn 8% but inflation is 3%, your real return is approximately 5%. Over 30 years at 5% real return, $10,000 grows to $43,219 in today's purchasing power. This is still excellent growth, but it is important to use real (inflation-adjusted) returns when planning for future expenses like retirement.

Disclaimer

This is educational content, not financial advice. Trading involves risk, and you should consult a qualified financial advisor before making any investment decisions. Past performance does not guarantee future results.

Related Articles

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.