Discounted Cash Flow (DCF): How to Value a Stock

⚡ Key Takeaways

- Discounted Cash Flow (DCF) analysis estimates a company

- s value beyond the explicit forecast period and typically represents 60-80% of total DCF value

- DCF is highly sensitive to assumptions about growth rates and discount rates, making it both powerful and subjective

- A DCF model provides a range of fair values rather than a single precise number

What Is Discounted Cash Flow Analysis?

Discounted Cash Flow (DCF) analysis is a valuation method that estimates the intrinsic value of a company based on the present value of its expected future cash flows. The core principle is that a dollar today is worth more than a dollar in the future because of the time value of money.

DCF analysis answers the fundamental question: what is this company worth based on the cash it will generate?

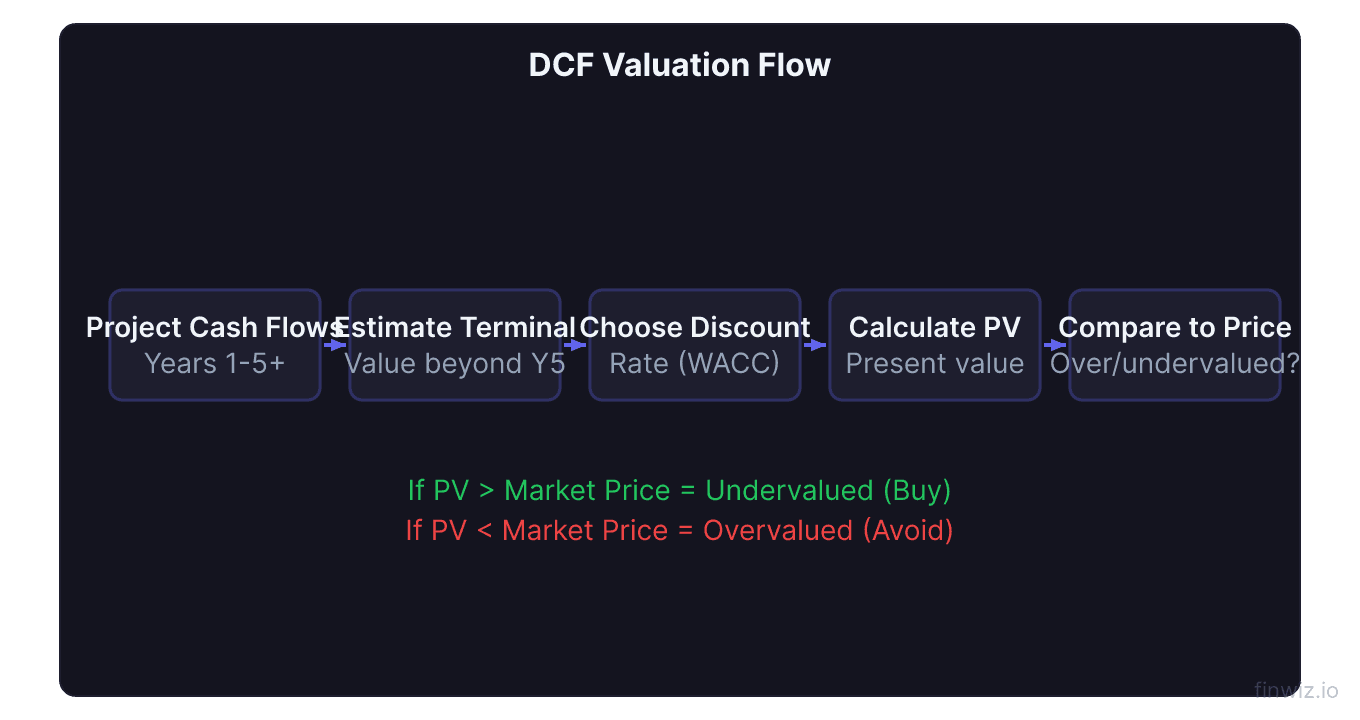

DCF Value = Σ (Cash Flow in Year N / (1 + Discount Rate)^N) + Terminal Value / (1 + Discount Rate)^NIf the DCF value per share is higher than the current stock price, the stock may be undervalued. If it is lower, the stock may be overvalued.

The DCF Process: Step by Step

Step 1: Project Free Cash Flows

Estimate the company's free cash flow (FCF) for the next 5 to 10 years. Free cash flow is the cash remaining after the company pays all operating expenses and capital expenditures.

Free Cash Flow = Operating Cash Flow - Capital ExpendituresUse the company's historical growth rate, industry trends, and management guidance to project future FCF. Be realistic: very high growth rates are difficult to sustain.

Step 2: Determine the Discount Rate

The discount rate reflects the risk of the investment and the cost of capital. The most common discount rate is the Weighted Average Cost of Capital (WACC).

WACC = (E/V x Cost of Equity) + (D/V x Cost of Debt x (1 - Tax Rate))For most companies, WACC typically ranges from 8% to 12%. Higher-risk companies deserve higher discount rates. Lower-risk companies with stable cash flows use lower rates.

Step 3: Calculate Present Value of Cash Flows

Discount each year's projected cash flow back to the present:

Present Value of Year N = FCF in Year N / (1 + WACC)^NStep 4: Calculate Terminal Value

The terminal value captures the company's value beyond your explicit forecast period. Since you cannot project cash flows forever, you assume the company either:

Perpetuity Growth Method: Grows at a constant rate forever (typically 2-3%, close to GDP growth).

Terminal Value = Final Year FCF x (1 + Growth Rate) / (WACC - Growth Rate)Exit Multiple Method: Apply an industry-standard multiple (such as EV/EBITDA) to the final year's metrics.

Terminal value often represents 60-80% of the total DCF value, which is why this assumption matters enormously.

Step 5: Sum Everything Up

Add the present value of all projected cash flows plus the present value of the terminal value. Divide by the total number of shares outstanding to get the intrinsic value per share.

Pro Tip

Sensitivity Analysis

Because DCF is highly sensitive to assumptions, a sensitivity analysis tests how the valuation changes as key inputs vary.

| Discount Rate \ Growth | 2% Growth | 3% Growth | 4% Growth |

|---|---|---|---|

| 8% WACC | $72 | $85 | $105 |

| 10% WACC | $58 | $67 | $80 |

| 12% WACC | $48 | $55 | $64 |

This table shows that reasonable variations in just two inputs can produce a wide range of valuations. This is why DCF provides a range of fair values, not a pinpoint number.

Advantages of DCF Analysis

- Intrinsic value focus: DCF values the company based on its own cash-generating ability, not on relative comparisons or market sentiment

- Forward-looking: Captures future potential rather than relying solely on historical data

- Flexible: Can be adapted to any company, industry, or scenario

- Comprehensive: Forces you to think deeply about growth, risk, and capital allocation

Limitations of DCF Analysis

- Highly sensitive to assumptions: Small changes in inputs produce large changes in output

- Difficult for unprofitable companies: Companies with no positive cash flow are difficult to value with DCF

- Terminal value dominance: The largest portion of value comes from the most uncertain part of the model

- Complexity: Requires financial modeling skills and a deep understanding of the business

- Not useful for trading: DCF is a long-term valuation tool, not a trading signal

DCF and Other Valuation Methods

DCF works best when combined with other approaches:

- P/E ratio: Quick relative valuation

- Price-to-Sales: Useful for unprofitable companies

- EV/EBITDA: Enterprise value relative to operating earnings

- Comparable company analysis: Valuation based on how peers are priced

If multiple valuation methods converge on a similar value, your confidence in that valuation increases.

Frequently Asked Questions

How accurate is DCF analysis?

DCF is directionally useful rather than precisely accurate. The value of DCF is in the process of thinking through the company's cash flow drivers, growth potential, and risks. The specific number should be treated as an estimate within a range, not as an exact fair value.

Can I use DCF for technology companies?

Yes, but it is more challenging because many tech companies have volatile or negative cash flows. For high-growth tech companies, the terminal value dominates the DCF, making assumptions about long-term growth rates particularly impactful. Revenue-based models may be more appropriate for unprofitable tech companies.

What discount rate should I use?

For most companies, a WACC of 8-12% is appropriate. Use higher discount rates for riskier companies (small-cap, volatile earnings) and lower rates for stable, blue-chip companies. If you are unsure, 10% is a reasonable default that forces you to justify growth with actual cash flow generation.

Is DCF relevant for short-term traders?

Generally, no. DCF is a long-term valuation tool best suited for investors with holding periods of months to years. Swing traders and day traders rely on technical analysis for timing and do not typically perform DCF analysis.

How often should I update a DCF model?

Update your DCF model quarterly when new earnings reports are released and whenever a significant event (acquisition, product launch, regulatory change) affects the company's cash flow outlook.

Disclaimer

This is educational content, not financial advice. Trading involves risk, and you should consult a qualified financial advisor before making any investment decisions. Past performance does not guarantee future results.

Common DCF Pitfalls

The Hockey Stick Projection

One of the most common mistakes in DCF modeling is projecting modest growth in the near term followed by explosive growth in later years, creating a "hockey stick" shape on the chart. This pattern is often wishful thinking rather than analysis.

To guard against this, anchor your projections in the company's historical growth rate and the industry's growth trajectory. Growth acceleration should be supported by specific catalysts (new product launches, market expansion, regulatory changes) rather than optimism.

Circular References

In more complex DCF models, the discount rate (WACC) depends on the market value of equity, which is what you are trying to calculate. This creates a circular reference that requires iterative calculation. Simplified DCF models avoid this by using an assumed discount rate rather than calculating WACC dynamically.

Ignoring Capital Intensity

Some companies require heavy ongoing capital expenditures just to maintain their current operations. A DCF model that projects growing revenue without accounting for the capital needed to support that growth will overestimate free cash flow. Always model capital expenditures as a percentage of revenue and consider whether that percentage will increase as the company grows.

When DCF Does Not Apply

DCF analysis is most appropriate for companies with positive, predictable cash flows. It is less useful or outright inappropriate for:

- Pre-revenue startups: No cash flows to discount

- Highly cyclical businesses: Cash flow projections are unreliable

- Banks and financial institutions: Cash flow measurement is different; book value and dividend discount models are more appropriate

- Mining and natural resource companies: Value depends heavily on commodity prices, which are notoriously difficult to forecast

For these companies, alternative valuation methods such as price-to-book, price-to-sales, sum-of-the-parts analysis, or comparable company analysis may be more appropriate.

Building Your First DCF Model

If you want to practice building a DCF model, start with a company you know well, preferably a stable, mature company with consistent cash flow growth. Use a simple spreadsheet with these steps:

- Pull the last five years of free cash flow from financial statements

- Calculate the average annual growth rate

- Project FCF for the next five years using a conservative growth rate

- Calculate terminal value using the perpetuity growth method at 2.5% long-term growth

- Discount all cash flows and terminal value at 10% WACC

- Sum to get total enterprise value, subtract debt, add cash, divide by shares outstanding

- Compare your per-share value to the current stock price

This exercise, even if imperfect, forces you to think critically about what drives a company's value.

Related Articles

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.