Long-Term vs Short-Term Capital Gains: Tax Rate Comparison

⚡ Key Takeaways

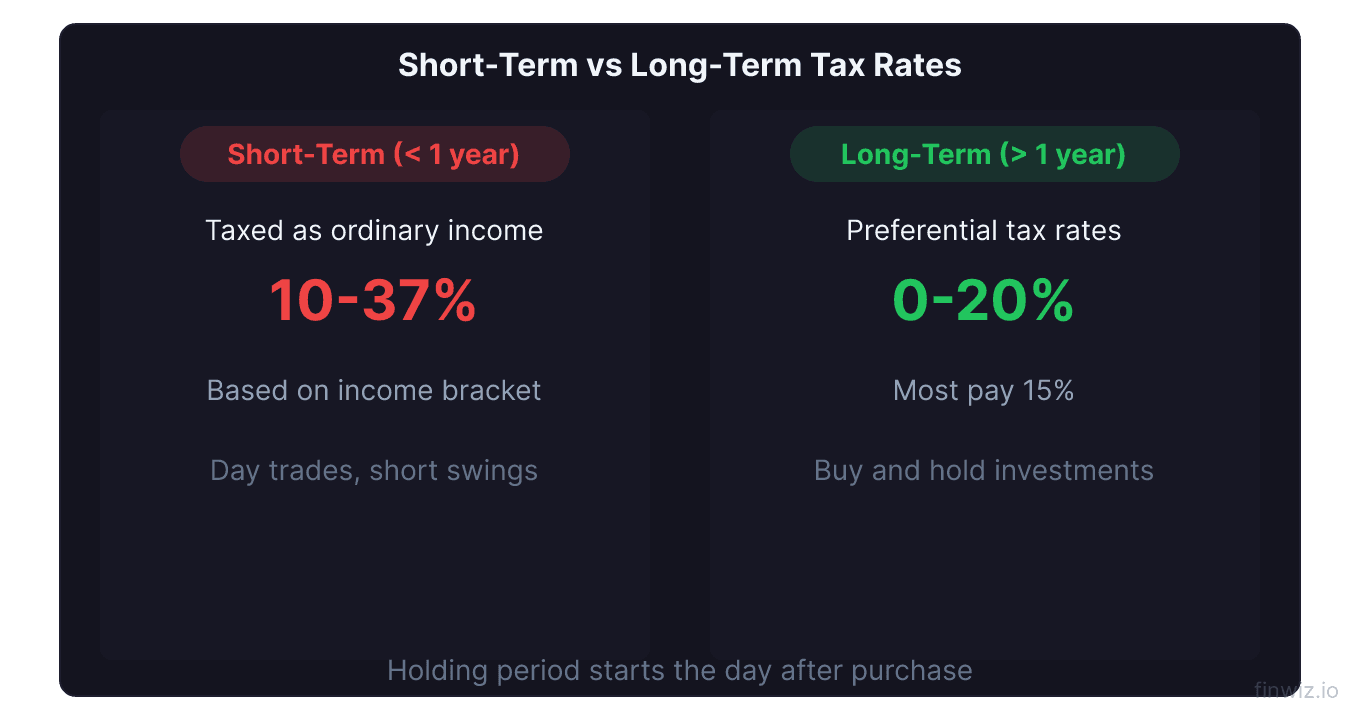

- Short-term gains (held ≤1 year) are taxed at ordinary income rates of 10%–37%

- Long-term gains (held >1 year) are taxed at preferential rates of 0%, 15%, or 20%

- The rate difference means long-term treatment can save 10–22 percentage points on the same gain

- Strategic holding period management and account selection are key to minimizing your tax burden

Long-Term vs. Short-Term Capital Gains: The Core Difference

The distinction between long-term and short-term capital gains is the single most impactful factor in investment taxation. The IRS draws a clear line: assets held for one year or less generate short-term gains taxed as ordinary income, while assets held for more than one year generate long-term gains taxed at significantly lower preferential rates.

This difference can be enormous. A trader in the 35% bracket who sells a stock after 11 months pays $3,500 in tax on a $10,000 gain. Waiting just one more month converts that to a long-term gain taxed at 15% — just $1,500. That one-month delay saves $2,000.

Understanding this distinction and building strategies around it is fundamental to tax-efficient investing.

Side-by-Side Rate Comparison

Here is a direct comparison of tax rates for different income levels:

| Taxable Income (Single) | Short-Term Rate | Long-Term Rate | Rate Savings |

|---|---|---|---|

| $30,000 | 12% | 0% | 12 points |

| $50,000 | 22% | 15% | 7 points |

| $100,000 | 24% | 15% | 9 points |

| $200,000 | 32% | 15% | 17 points |

| $400,000 | 35% | 15% | 20 points |

| $600,000+ | 37% | 20% | 17 points |

For married couples filing jointly, the brackets are roughly doubled, but the rate differentials remain similar. The savings are most dramatic for high earners, but even moderate-income investors benefit significantly.

Tax Savings = Gain × (Short-Term Rate − Long-Term Rate)The Impact Over a Lifetime of Investing

The compounding effect of tax-rate differences is substantial over time. Consider two investors, each generating $30,000 in annual gains over 25 years:

| Factor | Short-Term Trader | Long-Term Investor |

|---|---|---|

| Annual Gross Gain | $30,000 | $30,000 |

| Tax Rate | 32% | 15% |

| Annual Tax | $9,600 | $4,500 |

| Annual Net Gain | $20,400 | $25,500 |

| 25-Year Net Gains | $510,000 | $637,500 |

| 25-Year Tax Paid | $240,000 | $112,500 |

| Tax Savings | — | $127,500 |

The long-term investor keeps $127,500 more over 25 years on the same gross returns. If those savings are reinvested, the compounding advantage grows even further.

Pro Tip

When Short-Term Trading Makes Sense Despite Higher Taxes

While long-term holding is generally more tax-efficient, there are legitimate reasons to accept short-term tax treatment:

Momentum and trend strategies. Some strategies require shorter holding periods to capture price movements. If the gross return significantly exceeds the tax cost, short-term trading can still be profitable.

Risk management. Holding a losing position just to reach the one-year mark exposes you to additional downside risk. Selling at a short-term loss is often the better financial decision.

Market conditions. In highly volatile or declining markets, taking profits early may be wise even at higher tax rates. A 24% tax on a 20% gain beats a 15% tax on a 5% gain.

Tax-advantaged accounts. If you trade within an IRA or 401(k), holding period is irrelevant for tax purposes. All gains are tax-deferred (or tax-free in a Roth).

Holding Period Rules and Edge Cases

The holding period starts the day after purchase and includes the day of sale. Some nuances:

Same-day trades: Always short-term. No holding period exists.

Securities received as gifts: You inherit the donor's holding period. If the donor held the stock for 9 months and you hold for 4 more, the total is 13 months — long-term.

Inherited securities: Always treated as long-term, regardless of how long the decedent or you held them.

Stock splits and spinoffs: The original holding period carries over to the new shares.

Options exercised into stock: The holding period of the stock starts the day after exercise for calls. The original stock holding period determines treatment when a put is exercised.

Short sales: Short sales are generally short-term capital gains unless specific holding period requirements are met with other shares of the same security.

Strategies to Minimize Your Blended Tax Rate

The goal for most investors is to maximize the proportion of gains taxed at long-term rates. Here are effective strategies:

Track holding periods actively. Use a spreadsheet or portfolio tracking tool that shows the holding period for each position. Flag positions approaching the one-year mark.

Use specific identification. When selling partial positions, instruct your broker to sell the tax lots with the longest holding period first (and the highest cost basis for additional tax savings).

Harvest short-term losses first. Short-term losses are most valuable when they offset short-term gains. See our tax-loss harvesting guide for implementation details.

Separate accounts by strategy. Keep long-term positions in a taxable account (where they benefit from preferential rates) and short-term strategies in tax-advantaged accounts (where holding period does not matter).

Consider hedging near the one-year mark. If a position is approaching long-term status but you are worried about a decline, use protective puts or collars to lock in gains while the clock runs out.

The Net Investment Income Tax Effect

High earners pay the 3.8% NIIT on both short-term and long-term gains. This narrows the gap slightly at the top:

| Income Level | Short-Term + NIIT | Long-Term + NIIT | Effective Savings |

|---|---|---|---|

| Above NIIT threshold | 40.8% | 23.8% | 17 points |

| Below NIIT threshold | 37% | 20% | 17 points |

The rate difference remains significant even with the NIIT. The additional 3.8% applies equally to both types of gains, so it does not change the relative benefit of long-term holding.

State Tax Considerations

Most states do not differentiate between short-term and long-term capital gains. Both are taxed as ordinary income at the state level. This means:

- The federal preferential rate is the primary benefit of long-term holding

- State taxes add the same flat percentage to both short-term and long-term gains

- States without income tax (FL, TX, NV, WY, SD, AK, WA) eliminate this additional layer entirely

A few states do offer preferential treatment for long-term gains or provide exclusions, but these are the exception rather than the rule.

How Losses Interact With the Long-Term/Short-Term Distinction

The IRS applies losses in a specific order that preserves the maximum tax benefit:

- Short-term losses offset short-term gains first

- Long-term losses offset long-term gains first

- Excess losses of either type offset gains of the other type

- Net losses up to $3,000 offset ordinary income

- Remaining losses carry forward, maintaining their character (short-term or long-term)

This ordering matters strategically. A $10,000 short-term loss that offsets a $10,000 short-term gain saves $3,200 in taxes (at 32%). The same loss offsetting a long-term gain saves only $1,500 (at 15%). When you have a choice, use short-term losses against short-term gains for maximum benefit.

FAQ

Is it always better to hold for long-term treatment?

Not always. If a stock is declining, selling at a short-term loss is better than waiting. Short-term losses are actually more valuable than long-term losses because they offset higher-taxed short-term gains first. Risk management should generally take priority over tax optimization.

How does the holding period work for options?

For standard equity options, the holding period of the option itself determines short-term or long-term treatment. If you exercise an option, the stock's holding period starts fresh from the exercise date. Index options receive automatic 60/40 treatment under Section 1256.

Can I convert a short-term gain into a long-term gain?

Only by continuing to hold the asset past the one-year mark. You cannot retroactively change a gain's character. However, you can use tax-loss harvesting to offset short-term gains with short-term losses, and you can delay selling profitable positions until they qualify for long-term treatment.

Do the same rates apply to all investment types?

Mostly yes, but there are exceptions. Collectibles are taxed at a maximum long-term rate of 28%. Section 1202 qualified small business stock can be 100% excluded. Section 1256 contracts automatically receive 60/40 long-term/short-term treatment.

How do mutual fund distributions affect my short-term vs. long-term mix?

Mutual funds pass through capital gains distributions to shareholders. These distributions are classified as short-term or long-term based on the fund's holding period, not yours. You cannot control this, which is one reason ETFs and index funds (which generate fewer distributions) are more tax-efficient.

Disclaimer

This is educational content, not financial advice. Trading involves risk, and you should consult a qualified financial advisor before making any investment decisions. Past performance does not guarantee future results.

Related Articles

12 chapters covering charts, indicators, risk management & more. Plus weekly trading insights.